- Private Capital Insider

- Posts

- 📈 The return of regional bank failures?

📈 The return of regional bank failures?

Private Capital Insider: Weekend Edition

Equifund: Weekend Edition

February 04, 2024

While the mainstream financial news is busy cheering on the so-called “Biden Boom” in the stock market and labor market, the debut of Apple’s Vision Pro, and the never-ending saga of Elon Musk drama…

Here’s the major stories you’re not hearing much about.

Evergrande, one of China’s largest property developers, has been ordered to liquidate by a Hong Kong court. However, there is some speculation as to whether or not mainland China can tell Hong Kong to pound sand and otherwise ignore the court order.

While everyone is hoping the damage will stay contained, as we all know, the global financial system is too interconnected for that to be likely. In 2021, it was reported by Reuters that BlackRock, HSBC, and UBS were among the largest buyers of Evergrande debt.In a probably not-unrelated story, China – which, ironically, was once a champion of decentralized banking – is now forcing a massive consolidation of rural banks as financial risks are mounting.

Regional and mid-sized banks had an ugly Q4, posting huge year-over-year losses to Net Income; Q1 isn’t looking much better now that NY Community Bancorp – one of the banks that bought assets from failed Signature Bank – plunged 44% in a single day, causing the stock to be “halted” for volatility.

Fed chair Jerome Powell indicated he will not be cutting rates.

Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates have confirmed they are joining the BRICS bloc (34 countries have indicated interest) – which is the emerging gold-backed currency positioned to challenge the dollar dominance, and…

Central banks continue to buy gold at a record pace, and analysts are starting to hop on the “gold will hit record highs in 2024” train (probably nothing, right?).

In the previous Weekend Edition, we did a deep dive on Basel III, and why increasing capital requirements often results in a predictable outcome – bank failures that lead to more consolidation.

And, while we can in no way prove that Basel III is the culprit behind why all of this is happening now…

It is rather convenient timing that we’re starting to see the Ghost of 2023 Bank Failures emerging today.

While we have no interest in making any predictions about what will or won't happen…

In today’s issue, we are going to stay focused on what appears to be happening right now, and some historical context that may provide some clues as to why it’s happening.

-Equifund Publishing

P.S. For all the people who will undoubtedly write in asking what they should do with their money, we cannot provide any individualized advice or recommendations.

If you need help, please consult with a qualified financial professional who is licensed to provide investment advice.

P.P.S. Scary sounding headlines are one of the main reasons we’ve been devoting so much editorial space to more philosophical concepts – specifically around epistemology and worldviews.

In a world where it is very difficult to know what is REALLY going on, we have to remind ourselves that the only thing we can control is how we respond.

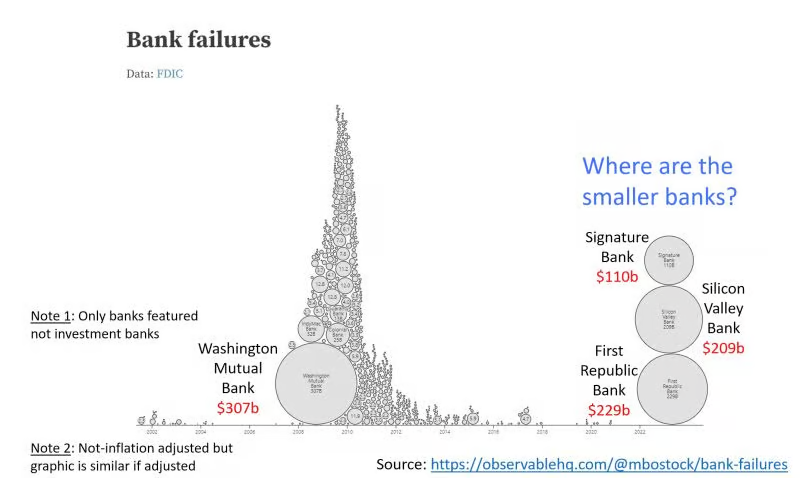

The Return of Regional Bank Failures?

If you haven’t read our May 6, 2023 issue, “Bank Failures, Short Sellers, and Commercial Real Estate,” here’s a quick recap of the most relevant talking point.

In the last two banking crises, we had a lot of small banks fail, with a few larger ones.

However, in the current crisis, the only failures so far have been three $100b+ institutions.

Where are all the small bank failures?

Answer: Thanks to short sellers and the pending commercial real estate crisis, bank stocks are getting crushed, and it appears the worst is still to come.

At the time of publishing, we were also in the very strange and paradoxical market sentiment of “the most predicted recession of all time” and “Holy Crap, AI!”

Generally speaking, consensus opinions are usually wrong.

But in this case, it appears the AI narrative was, in fact, the winner of 2023; the so-called Magnificent Seven stocks — Amazon.com (AMZN), Apple (AAPL), Google parent Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA) and Tesla (TSLA) – logged an impressive average return of 111%, compared to a 24% return for the broader S&P 500.

But one of the things I learned as a financial ghostwriter… When predicting a market crash, you’re never wrong, just early.

Can AI-powered tech stocks continue to bolster the entire stock market in 2024?

Who knows, but we’re starting to see headlines that suggest investor fatigue.

Source: Reuters

Source: Barrons

Source: Reuters

While we find KKR’s thesis surrounding AI-adjacent plays in 2024 interesting – energy infrastructure related to AI, like critical energy transmission assets, data centers, and cooling technologies – let’s get back to the “most predicted recession” narrative, and what’s going on with regional banks.

I don’t think it’s a stretch to suggest that everyone’s default thinking is that 2024 – arguably the most significant election year of all time – is a bad time to have a market crash.

Not to mention, the Fed has proven time and time again that they are going to step in and bail out (certain) banks, or take emergency measures to prevent a major crisis.

Speaking of the Fed…

The Federal Open Market Committee (FOMC) holds eight regularly scheduled meetings per year to:

Review economic and financial conditions,

Determine the appropriate stance of monetary policy, and

Assess the risks to its long-run goals of price stability and sustainable economic growth

I think most people have assumed that – due to the election year – we were going to see rates start to drop, and that would keep the stock market humming.

However, the Fed is stuck in a quandary right now. They either stick to their two percent inflation target, and keep rates higher for longer… or they risk losing all credibility by lowering rates for what could easily be assumed were “political reasons.”

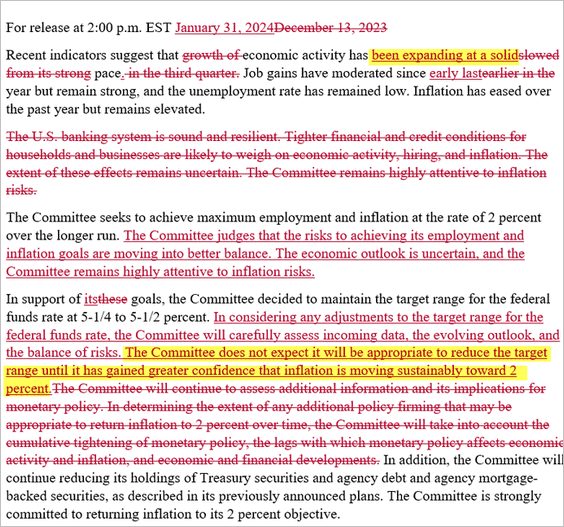

But let’s not guess – we can compare the most recent FOMC statement against the one from December.

Usually these announcements are almost identical from meeting to meeting.

But in December, Powell said “The U.S. banking system is sound and resilient,” and that line has now been removed.

Is there anything significant to that removal? We won’t speculate.

Instead, let’s move on to the other component investors are paying attention to – reducing the balance sheet through “Quantitative Tightening” (QT), which is removing money from the economy by allowing some of its holdings of debt securities to mature without reinvesting the principal – currently ~$95b per month in reductions – and therefore intended to reduce inflation.

Source: Bloomberg

Since QT began, the Fed’s balance sheet has shrunk from $9 trillion down to $7.68 trillion, according to the most recent central bank data.

In the December meeting, several officials saw it “appropriate” to begin discussing slowing this rundown.

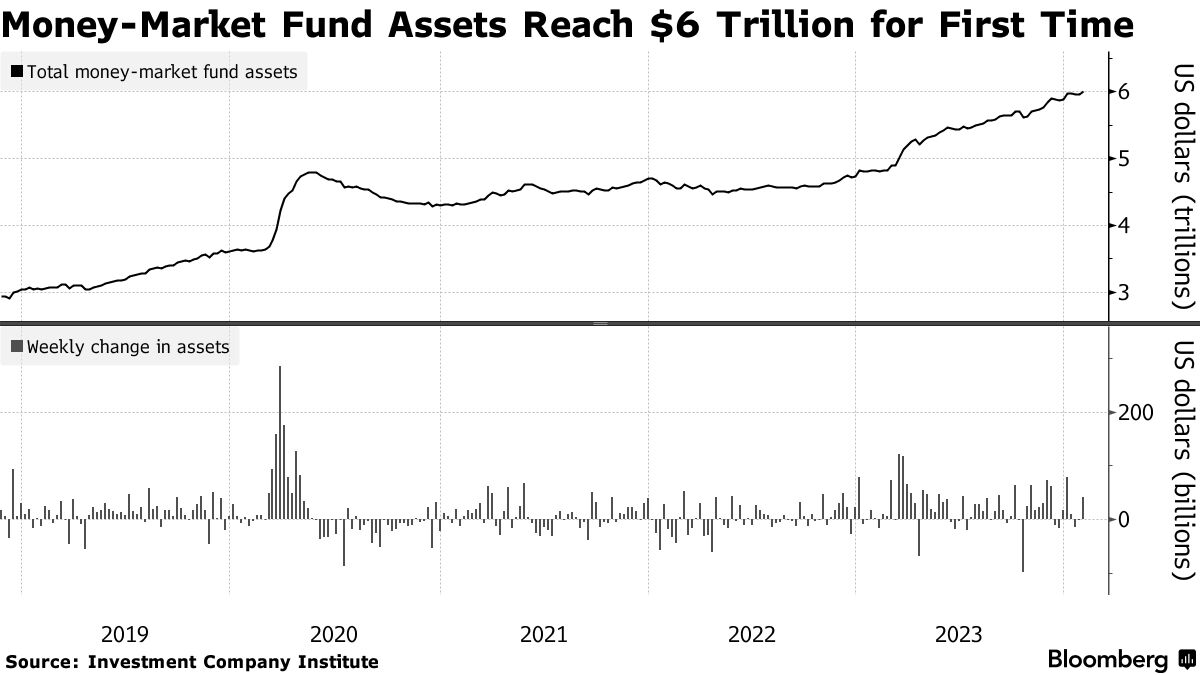

The Fed’s QT has also led to more government debt going to private investors such as banks, hedge funds, broker-dealers and money-market funds as the central bank has backed away from holding public debt.

The process threatens to deplete the amount of cash reserves banks hold at the Fed. If those reserves fall low enough, it could disrupt funding markets.

So far, though, that hasn’t been a problem. Bank reserves sit at $3.49 trillion, up 16% from last year.

But what could possibly deplete those bank reserves you ask?

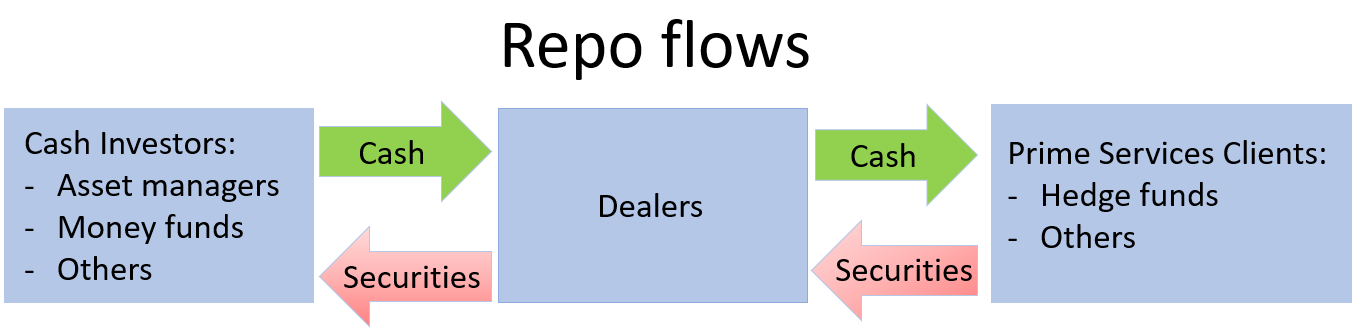

Enter: The Reverse Repurchase Facility Market

In case you have no clue what the overnight repurchase and reverse repurchase facilities are…

It’s an obscure part of the financial system that most people haven’t heard of.

A repurchase agreement (called “repo”) is a short-term secured loan, where one party sells a security to another party, while agreeing to repurchase it later at a higher price.

The “spread” paid between the sell price and the repurchase price is the “repo rate.”

A reverse repo is the opposite – one party purchases and agrees to sell them back at a positive return, often as soon as the next day (most repos are overnight transactions).

The economic effect of this transaction is pretty similar to a collateralized loan. The market value of collateral typically exceeds the amount of cash invested in a repo by an agreed-upon margin.

Why do they do this? According to Brookings:

1. The repo market allows financial institutions that own lots of securities (e.g., banks, broker-dealers, hedge funds) to borrow cheaply and allows parties with lots of spare cash (e.g., money market mutual funds) to earn a small return on that cash without much risk, because securities, often U.S. Treasury securities, serve as collateral.

Financial institutions do not want to hold cash because it is expensive—it doesn’t pay interest.

For example, hedge funds hold a lot of assets but may need money to finance day-to-day trades, so they borrow from money market funds with lots of cash, which can earn a return without taking much risk.

2. The Federal Reserve uses repos and reverse repos to conduct monetary policy.

When the Fed buys securities from a seller who agrees to repurchase them, it is injecting reserves into the financial system.

Conversely, when the Fed sells securities with an agreement to repurchase, it is draining reserves from the system.

Since the crisis, reverse repos have taken on new importance as a monetary policy tool.

Reserves are the amount of cash banks hold – either currency in their vaults or on deposit at the Fed.

The Fed sets a minimum level of reserves; anything over the minimum is called “excess reserves.”

Banks can and often do lend excess reserves in the repo market.

So what happens when “repo goes wrong?”

Well, in 2019, it did. In mid-September 2019, repo rates spiked dramatically, rising to as high as 10% intraday.

Source: Federal Reserve

This eventually led to an emergency intervention by the Fed, which pumped $75bn into the repo markets a day, for the next several days.

The official story is the main cause was a temporary shortage of cash, which was caused by two events on September 16th: the deadline for the payment of quarterly corporate taxes and the issuing of new Treasury securities.

That’s why we’re starting to see some concern about this exact issue as it relates to QT.

Usage of the Fed’s reverse repo facility, or RRP, has been considered the canary in the coal mine when it comes to the end of QT because whatever is still parked there — about $581 billion currently — is considered the remaining excess liquidity in the financial system.

Even though bank reserve balances are still above the level they were when the central bank began its unwind in June 2022.

Generally speaking, repo’s are classified as a money market instrument, as it’s used for short-term capital needs.

Why do we care about any of this? Because of the Basel III reserve requirements.

If we look at the reason why market crashes happen, they more or less all happen due to a liquidity crisis – when there are no more dollars available in the financial system to cover costs, that is when defaults start to occur.

As we covered last week, higher reserve requirements mean a tightening of credit, as banks can’t lend as much.

Additionally, it means in order to attract more deposits into the bank, they have to compete with ~4-5% yields we’re seeing in the money markets.

Banks large and small have had to shell out more interest to yield-hungry depositors.

But it is harder for regional and community banks to absorb those costs than for the megabanks, whose scale and diversity help them navigate good times and bad.

Some customers and investors became wary of all but the largest banks after a crisis of confidence in early 2023 caused depositors to flee, taking down three regional lenders in rapid succession.

PNC Financial Chief Executive Bill Demchak said the bank crisis exacerbated the need for scale, particularly when it comes to corporate customers that “don’t necessarily trust the regulatory environment to ensure that their deposits at a [smaller] bank are safe,” or that need more complex services such as treasury management.

For now, regional banks have sought to shrink themselves back to health, as they face steep deposit and technology costs, as well as potentially tougher regulations.

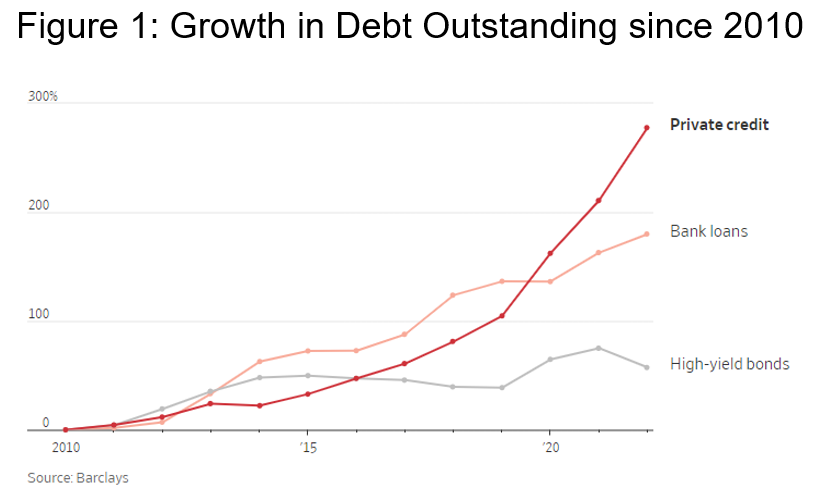

For many reasons, this only serves as a mechanism for pushing more and more lending into the less regulated world, or private credit funds.

Source: ABA Banking Journal

This brings us to the New York Community Bancorp Story…

New York Community Bancorp Inc’s stock lost more than a third of its value Wednesday in its steepest one-day drop ever, after it posted a surprise loss, built up its reserves, and signaled challenges in the office-space sector with one of two troubled loans.

Source: MarketWatch

While there’s plenty of coverage going on right now regarding New York Community Bancorp – and plenty of debate on whether this is an isolated incident or not…

It’s bringing back up what I find to be a concerning narrative – the small, regional bank business model is broken, and therefore, they should consolidate.

Yes, regional banks have a larger exposure to the commercial real estate (CRE) sector.

Yes, the CRE refinancing timebomb thing is pretty scary (please refer to our May 6, 2023 issue for more on this).

And yes, it would be better if regional banks had a more diversified balance sheet and loan portfolio to reduce the systemic risk.

But I do not for one second believe the problem with regional banks is regional banks – the problem is the two-tiered banking system.

As more and more regulatory requirements get pushed in the name of market safety, all this does is put yet another tax on “the little guy.”

You’re either too big to fail or too small to survive.

But if you want to fight centralization, the answer is still decentralization.

A regulatory proposal we’re watching

Speaking of weird banking regulations…

Check out this recently published document in the Federal Reserve titled, “Self-Regulatory Organizations; The Options Clearing Corporation; Notice of Filing of Proposed Rule Change by The Options Clearing Corporation Concerning Its Process for Adjusting Certain Parameters in Its Proprietary System for Calculating Margin Requirements During Periods When the Products It Clears and the Markets It Serves Experience High Volatility”:

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (“Exchange Act” or “Act”), and Rule 19b–4 thereunder, notice is hereby given that on January 10, 2024,

The Options Clearing Corporation (“OCC”) filed with the Securities and Exchange Commission (“SEC” or “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared primarily by OCC.

The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons.

This proposed rule change would codify OCC's process for adjusting certain parameters in its proprietary system for calculating margin requirements during periods when the products OCC clears and the markets it serves experience high volatility.

To be fair, I haven’t read all 131 pages of this document, but I immediately have questions.

For example…

What is the point of having margin requirements if we just pretend they don’t exist during the exact periods of time they are supposed to exist?

Is the OCC expecting some sort of high volatility to happen this year that would, oh I dunno, blow up all their derivative contracts?

According to the document:

To determine when implementation of high volatility control settings may be appropriate, OCC monitors the volatility of the products it clears and the markets it serves.

Based on the results of this monitoring, OCC may determine to implement high volatility control settings for those model parameters.

OCC previously described its use of high volatility control settings within STANS in its filing to establish its STANS Methodology Description.

The STANS Methodology Description, however, does not provide specific details around the process for setting or applying high volatility control settings.

To ensure that OCC's rules include a sufficient level of detail about material aspects of OCC's margin system, OCC proposes to amend its Margin Policy, which is filed as a rule with the Commission, to define material aspects of the high volatility control setting process.

OCC has implemented global settings on only a few occasions. For example, OCC implemented global control settings for equities, indexes, volatility-based products and short ETF products from March 9, 2020 until April 9, 2020 in connection with the market volatility associated with the onset of the COVID–19 pandemic and on January 27, 2021 for volatility-based products in connection with market volatility caused by the so-called “meme stock” episode.

It’s unclear if this is sensible market reform, or something a bit more sinister…

But we’re keeping track of this to see if it winds up getting triggered in the near future.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |