- Private Capital Insider

- Posts

- 📈 Basel III, Access to Capital, and Kevin O’Leary

📈 Basel III, Access to Capital, and Kevin O’Leary

Private Capital Insider: Weekend Edition

Equifund: Weekend Edition

January 28, 2024

While the mainstream media is focused on plane problems, election coverage, and more stuff about AI…

The story that is strangely absent is the conversations around the conspiracy theory sounding international banking reform called Basel III Endgame.

More specifically, the two major standards that have already started to roll out in January here in the United States – the Fundamental Review of the Trading Book and the Basel III: Finalizing post-crisis reforms.

What are these standards, why should you care, and how might it potentially impact you?

That’s what we’re covering in today’s Weekend Edition of Private Capital Insider.

-Equifund Publishing

P.S. Today’s weekend edition builds off the foundational “investment philosophy” we discussed in the Jan 17th (Searching for “Truth” in Early Stage Investing) and the Jan 25th(Turning ideas into investments (that hopefully make money) Editions of Private Capital Insider.

Fair warning, this will be one of our longer posts we’ve ever published. I’m sure some of you will tell me it’s too long… but we believe it warrants the space and coverage.

House Committee on Small Business Hearing – “Basel III will harm small businesses by making American banks less competitive”

On Jan 18th, Congressman Roger Williams (TX-25), Chairman of the House Committee on Small Business, gaveled in a full committee hearing titled “Unleashing Main Street’s Potential: Examining Avenues to Capital Access.”

However, based on the testimonies of the witnesses – one of whom was Kevin O’Leary – and the general Q&A, this meeting could have easily been called “two hours of complaining about Basel III, its impact on small business, and what we can do to improve access to capital.”

While Basel III’s primary goal is to prevent additional financial crises, it would directly harm small businesses.

Basel III works by requiring a material increase of capital requirements applicable to banking organizations with total assets of $100 billion or more.

As a result, large banks and most regional banks will be required to increase the amount of capital they hold by an estimated 20 percent on average.

When banks are forced to keep more money on the sidelines to fulfill their capital requirements, there is less money that can be loaned out to the communities they serve.

Should the Basel III proposal be implemented, it would further prevent banks from making loans at a time when small businesses are struggling to access capital.

As a result, more business owners have started to think twice about taking on new loans or drawing upon lines of credit to start their businesses.

We don’t need to dive any deeper into what was said in the hearing, as it didn’t reveal much in the way of details (or backstory) on what Basel III is.

Instead, we’re going to take a deep dive into all of the missing history – and context – you’d want to understand, if you wanted to understand the potential impact of Basel III on the economy.

And perhaps most importantly, small business, and the millions of American employees who depend on them.

The Basel Accord: A Brief Intro to International Banking Standards

Like many stories about finance, this one begins in the 1970s after the Nixon Shock that ended the gold convertibility of the U.S. Dollar.

On June 26th, 1974, a small privately owned bank called Herstatt Bank was put into liquidation by German regulators.

Now called the Herstatt Crisis, the bank collapsed due to something called settlement risk in the foreign exchange (FX) market.

Settlement risk is the possibility that one or more parties will fail to deliver on the terms of a contract at the agreed-upon time.

Settlement risk is a type of counterparty risk associated with default risk, as well as with timing differences between parties.

Here’s how it all went down…

Herstatt had speculative FX positions, and had sold a sizable amount of U.S. dollars against the Deutsche mark, but the market moved against them.

As the firm tried to close out its positions – because of the time zone difference, with one bank being open while the other was closed – the trade didn’t exactly go as planned.

Because there was no mechanism for instantly settling the international trade – and because the exchange rate moved – Herstatt had received the German Marks it purchased, but not yet delivered the dollars it sold to cover.

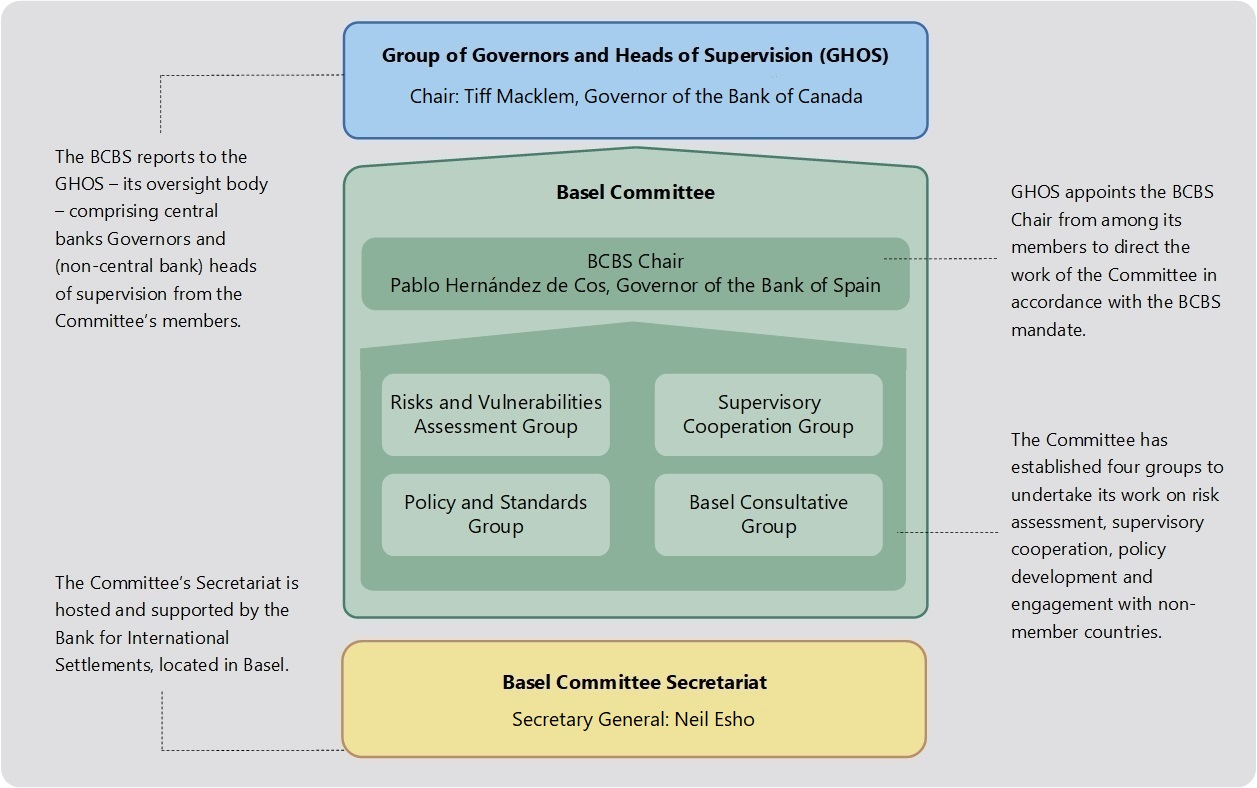

Long story short, this led to the formation of the Committee on Banking Regulations and Supervisory Practices in 1974 – later renamed the Basel Committee on Banking Supervision – headquartered at the Bank for International Settlements (BIS) in Basel, Switzerland

In case you’ve never heard of the BIS, think of it as the “final boss” of the international central banking cartel; the central bank of all central banks, which even Swiss authorities may not enter without permission.

Source: BIS

According to the BIS, the Committee “was established to enhance financial stability by improving the quality of banking supervision worldwide, and to serve as a forum for regular cooperation between its member countries on banking supervisory matters.”

In 1975, the Committee published a paper that came to be known as the “Concordat” – a founding document of what would later become the basis of the Basel Accord.

Specifically, the paper set out principles for sharing supervisory responsibility for bank’s foreign branches, subsidiaries, and joint ventures.

Banking supervision is considered in this report from three different aspects: liquidity, solvency and foreign exchange operations and positions.

The Committee recognizes that these three different aspects are to some extent overlapping.

For instance, liquidity and solvency problems can shade into one another; and both liquidity and solvency considerations are among the reasons why countries supervise their bank’s foreign exchange operations.

The Committee agrees that the basic aim of international cooperation in this field should be to ensure that no foreign banking escapes supervision.

This paper was later revised and reissued in 1983 as the Principles for the supervision of banks' foreign establishments.

I’ll spare you the boring, technical, and vastly deep rabbit hole inside the various updates and revisions…

But the main things we want to stay focused on are the topics of liquidity and solvency.

Illiquidity means the borrower (or the borrowing country) is unable to pay back now, but it can pay back later.

Insolvency means the borrower (or the borrowing country) is unable to pay back, both today and in the future.

You might recall there was a rather nasty debt crisis in the 1980s in Latin America.

The problem exploded in August 1982 as Mexico declared inability to service its international debt, and the similar problem quickly spread to the rest of the world.

Enter: Basel I

Following comments on a consultative paper published in December 1987, a capital measurement system commonly referred to as the Basel Capital Accord was approved by the G10 Governors and released to banks in July 1988.

The 1988 Accord called for a minimum ratio of capital to risk-weighted assets of eight percent, to be implemented by the end of 1992.

Risk-weighted assets are used to determine the minimum amount of capital a bank must hold in relation to the risk profile of its lending activities and other assets.

This is done in order to reduce the risk of insolvency and protect depositors. The more risk a bank has, the more capital it needs on hand.

The capital requirement is based on a risk assessment for each type of bank asset.

The Basel I classification system groups a bank's assets into five risk categories, labeled with the percentages 0%, 10%, 20%, 50%, and 100%. A bank's assets are assigned to these categories based on the nature of the debtor.

The first Basel accord only focused on credit risk.

The other types of risks such as market risk and operational risk were simply excluded from the analysis (which would eventually be accounted for under Basel II).

Basel II

Published in 2004, Basel II was a new capital framework to supersede the Basel I framework. It introduced the "Three Pillars":

Minimum capital requirements, which sought to develop and expand the standardized rules set out in the 1988 Accord;

Supervisory review is the process whereby national regulators ensure their home country banks are following the rules;

Market discipline refers to the disclosure requirements for individual banks, allowing other market players to assess each bank’s capital and risk exposures. Under this framework, banks are required to disclose all material information relating to their risk management policies, but enforcement is left to the individual regulators.

Immediately after the Great Financial Crisis of 2007-2009, the so-called “Basel II.5” package of reforms included a major increase to the market risk capital standards for banks.

This, among other things, introduced something called the Incremental Risk Charge and the Stressed Value-at-Risk.

These were considered a stopgap measure regarding the underlying structural problems, which would eventually be addressed in the form of the more comprehensive Fundamental Review of the Trading Book (FRTB).

In case you have no idea what a Trading Book is, it functions as an accounting ledger that tracks all securities held by the bank, which are considered available-for-sale and used for active trading.

The fluctuations in the portfolio value must also be recorded on a daily basis and recognized in the profit and loss statement.

This is in contrast to assets in the Banking Book, which are presumed to be held until maturity, the value of assets in the trading book must be marked-to-market.

Mark to market is a method of measuring the fair value of accounts that can fluctuate over time, such as assets and liabilities.

Mark to market aims to provide a realistic appraisal of an institution's or company's current financial situation based on current market conditions.

Banks are strictly prohibited from moving assets from one book to the other, as a mechanism for capturing regulatory arbitrage benefits – a practice whereby firms capitalize on regulatory systems’ loopholes, in order to circumvent unfavorable regulation.

For example, a bank might try to move an illiquid asset out of the Trading Book (hard to mark to market because it's difficult to do a valuation), and move it to Banking Book (using historic costs).

The finalized BCBS framework outlines two approaches that firms can adopt to calculate their market risk capital requirements – the Standardized Approach and Internal Models Approach.

Source: SIFMA

I’ll spare you all the details of exactly how these frameworks work…

But the important thing to know is the rather predictable conclusion – banks will need to increase their capital ratios related to risk weighted assets.

And as we’ve learned time and time again, when banks are forced to increase their capital reserves, it causes a credit crunch that inevitably hits the “little guy” hardest.

Originally, the FRTB changes – along with the rest of the Basel III Endgame reforms – were widely assumed to be issued at the end of 2020, at the latest.

Thanks to COVID, the rollout was delayed to January 1, 2023.

Introducing: Basel III Endgame (B3E)

The B3E proposal was jointly published on July 27, 2023 by the Federal Reserve, the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation.

With a proposed compliance date of July 1, 2025, U.S. banks will have approximately two years to interpret the new rule, address new data and technology needs, and adjust their business models.

Under Basel III, the minimum Tier 1 capital ratio is 10.5%, which is calculated by dividing the bank's Tier 1 capital by its total risk-weighted assets.

However, Basel III also eliminates Tier 3 capital, and instead places new liquidity ratios on banks, specifically the Net Stable Funding Ratio.

This introduced an Required Stable Funding factor of 85% for gold held on a bank’s balance sheet (we’ll come back to this in just a bit).

While the proposal only applies to banks with $100bn or more in assets… The “everyone knows that everyone knows” part, is that increased capital requirements for large banks will almost certainly have trickle down impacts on smaller banks.

The Weird Part About “Gold” Under Basel III

Amongst all the controversy surrounding Basel III, it is the potential impact on allocated/unallocated gold that I find most interesting.

Allocated gold is all gold held in custody – off balance sheet – that belongs to the depositors.

Unallocated gold – often referred to as paper gold – is attractive to banks because they can leverage on the gold actually held in the vaults, and some estimates put the ratio of unallocated gold to physical gold at up to 400 times, making it potentially very profitable to bullion banks.

Under the new regulation, allocated gold will be considered a Tier 1 asset and will continue to have zero risk weighting.

Conversely, banks’ unallocated gold and exposures due to other financial transactions will be considered a Tier 3 asset subject to a Required Stable Funding ratio of 85%, like other risky assets such as equities.

Under the new rules, banks are required to hold physical gold or other liquid assets for an amount equal to at least 85% of the value of unallocated gold on their books.

A likely, and probably intended, consequence of the Basel III rules will be a drop in the volume of financial transactions linked to gold.

The increased cost of these activities will encourage bullion banks to reduce their exposure or to increase the price they charge clients, who may reduce demand for those products.

The new rules give physically held gold a preferential treatment over paper gold, and that should increase demand for bullion and support the price of gold.

Many commentators see as no coincidence that since 2017 central banks have purchased large volumes of physical gold and that gold prices have generally risen.

Because of the new rules, banks are expected to advise clients to turn unallocated into allocated gold positions, increasing, at least temporarily, the demand for physical gold.

We’ve dedicated several issues of Private Capital Insider to the gold markets, as well as the de-dollarization narrative surrounding the emergence of a gold-backed BRICS currency.

While I’m not entirely sure if the increased capital requirements – and changes in how gold is treated – will either help or hinder such a thing from happening…

It’s definitely something worth paying attention to.

Criticism of Basel III Endgame

What was the [expletive] point of Basel in the first place?

In 2023, we saw the collapse of three banks – Signature Bank, Silicon Valley Bank, and First Republic (see our May 6th, 2023 issue for our coverage on this).

Without going way too deep into the weeds about why this crisis was, in some respect, a massive government sponsored bonanza for JP Morgan…

Suggesting that these bank failures would have somehow been stopped, if not for greater capital requirements, just doesn’t line up with the reality of the Fed Rate Hike Agenda and the objectively poor management of duration risk by the banks.

During a Senate Banking Committee hearing in November 2023, Sen. Steve Daines (R-Mont.), admonished Federal Reserve Vice Chair for Supervision Michael Barr, FDIC Chair Martin Gruenberg and Acting Comptroller of the Currency Michael Hsu, saying:

We saw the bank failures earlier this year, I believe, as a result of regulators being asleep at the switch, as we probed in great depths in many of these failures.

It's clear these failures were not due to insufficient capital. Nevertheless, you're moving forward with a flawed Basel III endgame proposal.

One area of the reforms where the application of national discretion is most apparent is on capital requirements applied to operational risks.

A focal point of the latest Basel standards was to standardize the treatment of operational risks, rather than the current approach which allows banks to rely on internal models.

The committee established risk weights for certain exposures and a method for calculating the capital needed to offset them.

Unlike other jurisdictions, U.S. regulators incorporated this new operational risk framework in full.

Chen Xu, a bank regulatory lawyer with Debevoise & Plimpton, said even by regulators' official estimates — which he believes understates the actual impact — the operational components of the proposal are driving "the vast majority" of capital requirement increases.

But aside from the usual teeth gnashing from banks who think more regulation is bad because it hurts their profit margins…

According to the Organisation for Economic Co-operation and Development (OECD),

“The estimated medium-term impact of Basel III implementation on GDP growth is in the range of -0.05 to -0.15 percentage point per annum”

Because that’s exactly what we need…

More banking regulation that, under the guise of preventing market crises, in reality, is what actually causes them in the first place.

So what are we to do about it?

Final Thoughts: The solution is decentralized

As a former financial ghostwriter, I’ve written my fair share of “doom and gloom” articles.

While there are no shortages of extremely scary-sounding conspiracy theories involving the BIS’s “one world bank, one world currency” agenda…

The worst thing you can do for your mental health is continually scare yourself with all the possible “Endgames” the global elites are cooking up.

While I most certainly could be wrong, it seems very clear to me that Basel III will only serve as a mechanism to continue the consolidation of the banking sector here in America (and around the world)...

As well as the implementation of the dystopian sounding Central Bank Digital Currency.

So what are we – the “little guys” – supposed to do about it?

Simply put, we must stand up and become “Creditors in Commerce” and make use of our Private Capital.

According to Professor Richard Werner, Chair in International Banking at the University of Southampton, U.K., and Director of its Centre for Banking, Finance and Sustainable Development:

Most central banks were created as cartels by big banking groups. Today, many central banks remain in private hands – such as the Federal Reserve Bank of New York, the Italian, Greek or South African central banks.

The solution to this concerted threat to our civil liberties and our freedom can only be to try to advance the opposite agenda: the decentralization of power.

We can decentralize power in our monetary system by abandoning the big banks and instead creating and supporting local not-for-profit community banks and ultimately a system of local public money issued by local authorities as receipts for services rendered to the local community.

The truth of the matter is: We don’t need central banks.

Since 97% of the money supply is created by banks, the importance of central banks is far smaller than generally envisaged. Moreover, the kind of money that commercial banks create is not privileged at law.

Legally, our money supply is simply private company credit, which can be created by any company, with or without a banking license.

This reality of private money creation also means that we can, without legal obstacles, create a decentralized system of local currencies, without central bank involvement.

You can make the decision to support local farmers and small businesses.

You can make the decision to support community banks and credit unions.

You can make the decision to deploy capital in your local community.

You can make the decision to stand up for what is right, true, and good.

You can make the decision that you will take responsibility for solving problems that you didn’t create.

And together, we can make a difference by simply deciding we can.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |