- Private Capital Insider

- Posts

- 📈 Searching for “Truth” in Early Stage Investing

📈 Searching for “Truth” in Early Stage Investing

An Insider’s Guide to Fact, Fiction, and Financials

Jake @ Equifund

January 17, 2024

As early stage investors, we are constantly faced with a paradox – we understand we have to take risks to generate above market returns, but we also want certainty and safety.

And if the first two weeks of 2024 are any indication of what’s to come this year, here is my one and only prediction I am going to make…

We may be diving headfirst “Through the Looking Glass” where it will be increasingly difficult to separate Fact from Fiction.

And more specifically, separating Truth from Narratives.

For those who remember reading George Orwell’s 1984 in school, this quote, in particular, stands out…

The Party told you to reject the evidence of your eyes and ears. It was their final, and most essential command.

Don’t worry, I promise this fun newsletter I write about investing isn’t about to devolve into a partisan propaganda rag.

But as early-stage investors, we are constantly being asked to believe in magical versions of the future – as well as the shameless self promotion of management teams and their technology – when investing.

So how do we deal with investing in this period of high risk and uncertainty, where we have to both determine what is “True” today, but could also come “True” tomorrow?

That’s the topic of today’s issue of Private Capital Insider.

-Jake Hoffberg

P.S Looking for back issues of Private Capital Insider?

The Search For “Truth” in Early Stage Investing

When I started my career as a financial ghostwriter in 2016, my very first client was a well-known author who – for all intents and purposes – was always predicting that a massive crash was just around the corner.

This meant the majority of my day was spent scaring the crap out of myself, as I had to produce content that supported that author's viewpoints.

“The greatest crash in history is right around the corner! Huge fortunes are always made after the crash! Move to cash and get ready for the sale of a lifetime!”

But then, Trump got elected and the mood of our audience switched from extreme fear to extreme greed.

And instead of crashing the economy and starting World War III… we wound up with what I can only describe as pure insanity in the stock market (remember the cannabis/crypto bubble in 2017?).

Again, I don’t say any of this to be political. I simply want to point out that – even armed with what appeared to be irrefutable “proof” that the author was correct – the author was completely wrong in terms of what actually happened.

Sure, the author sold lots of books and newsletters off the back of what I can only describe as fear porn…

But in an effort to try to “wake people up” to the “truth” that the “mainstream media doesn’t want you to see,” none of it really translated into making money in the markets.

To be fair, hindsight is always 20/20. It’s always easy to look back and say “man, that dude was totally wrong! I lost a lot of money following that guy's stock picks.”

But the problem with business and investing is this: even if your predictions are correct, and you manage to make all the right moves to be prepared, you can still lose money.

And on the flip side, your predictions can be completely wrong, but the steps you took to protect yourself from a crisis that never happened wind up protecting you from the crisis that did.

So I say this with all sincerity…

After writing for many different authors, with many different worldviews – all of whom made lots of predictions that rarely came true – I write this newsletter as an opportunity to practice skeptical inquiry in search of “Truth,” so that I can operate from “First Principles,” instead of my emotions.

In layman’s terms, first principles thinking is basically the practice of actively questioning every assumption you think you ‘know’ about a given problem or scenario — and then creating new knowledge and solutions from scratch.

On the flip side, reasoning by analogy is building knowledge and solving problems based on prior assumptions, beliefs and widely held ‘best practices’ approved by the majority of people.

People who reason by analogy tend to make bad decisions, even if they’re smart.

If that sounds like a deeply philosophical pursuit, that’s because it is.

And in case you’re wondering how any of this is going to help you make money as an investor…

If the secret to investing is to be contrarian and right… This means you must first be willing to change your mind.

Both in life, and as an investor, one of the hardest things to do is to admit when we are wrong.

But the single worst thing we can do is insist we are right, and close ourselves off to Truth!

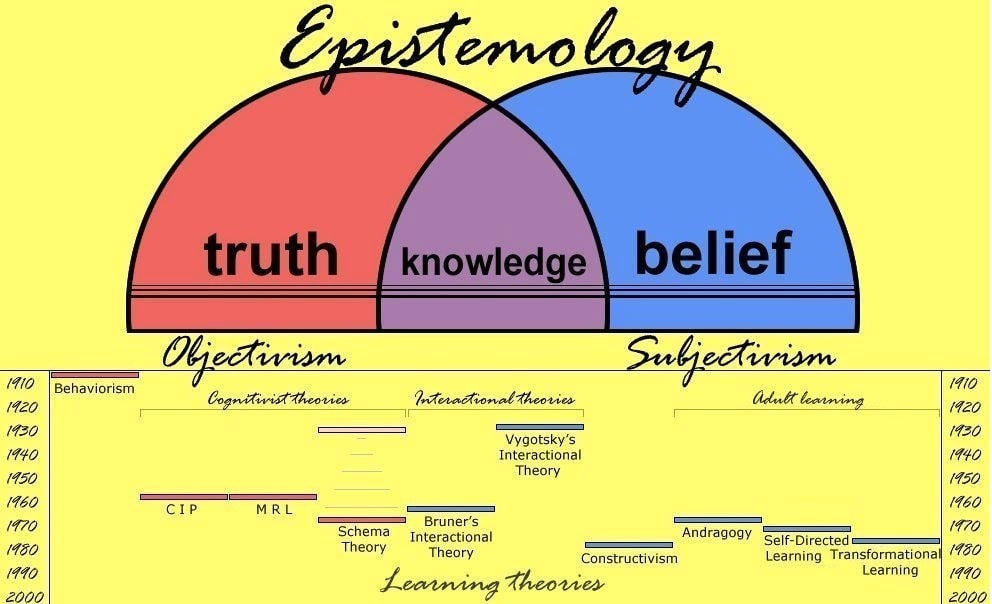

For this reason, I’ve been diving deep into Epistemology – the study of what knowledge is and how to acquire it – is going to become increasingly important in the “Post Truth” Era that has become increasingly partisan.

Because as Alexander Hamilton once said, "Those who stand for nothing, fall for anything."

And I have found great comfort in this simple diagram – that knowledge lies at the intersection of what is objectively true and subjectively believed, and that common knowledge is a result of shared truths and shared beliefs.

But in a world where people seem to live in entirely parallel universes with completely separate “truths”… how do we know which version of reality to believe?

Especially now that we live in a world where everyone can simply choose to reject the objectively true by calling into question the authenticity of the “evidence,” and the credibility of the source?

More often than not, we tend to default to whatever Narrative sounds most believable to us, based on our current worldview and emotional state, regardless of the supporting evidence.

It is true because we feel it is true (called “Truthiness”).

And it is for this reason that I have spent my entire career learning how to build – and dissect – Narratives and “Investment Fables” surrounding early-stage companies (and other assorted investing strategies).

According to Aswath Damodaran – Professor of Finance at the Stern School of Business at New York University, where he teaches corporate finance and equity valuation:

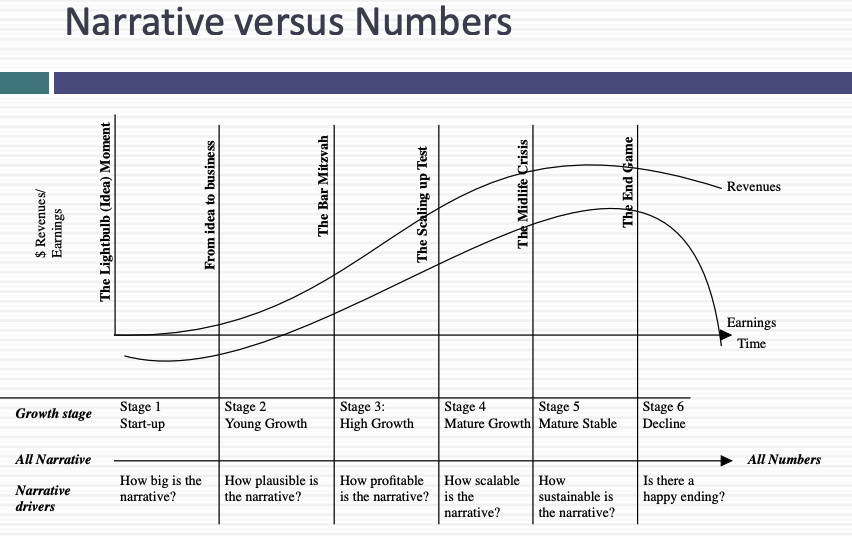

With a young company, narrative is central, divergent and volatile.

It is central because it is the only thing that you are offering investors, since you have no history.

It is divergent because you can still offer widely different narratives, since it is early in the game.

It is volatile, because the real world will deliver surprises that will require you to adjust your narrative.

As companies age, their narratives get narrower as their histories, size and culture start to become binding. The numbers often drive the narrative, rather than the other way around.

Every valuation starts with a narrative, a story that you see unfolding for your company in the future.

In developing this narrative, you will be making assessments of your company (its products, its management), the market or markets that you see it growing in, the competition it faces and will face and the macro environment in which it operates.

Rule 1: Keep it simple.

Rule 2: Keep it focused.

Source: Aswath Damodaran

Even though we may have some historical financials (although often we don’t)…

As early-stage investors, we are forced to create an assumption driven financial model that projects a possible future of the company.

Then, there is a story about those numbers (the Narrative), which helps the investor believe they can come true.

But to make a call back to Epistemology… How do we practice skeptical inquiry of the narrative we’re being presented?

How do we determine what the “truth” is, and how it is being used for the assumptions in the financial model?

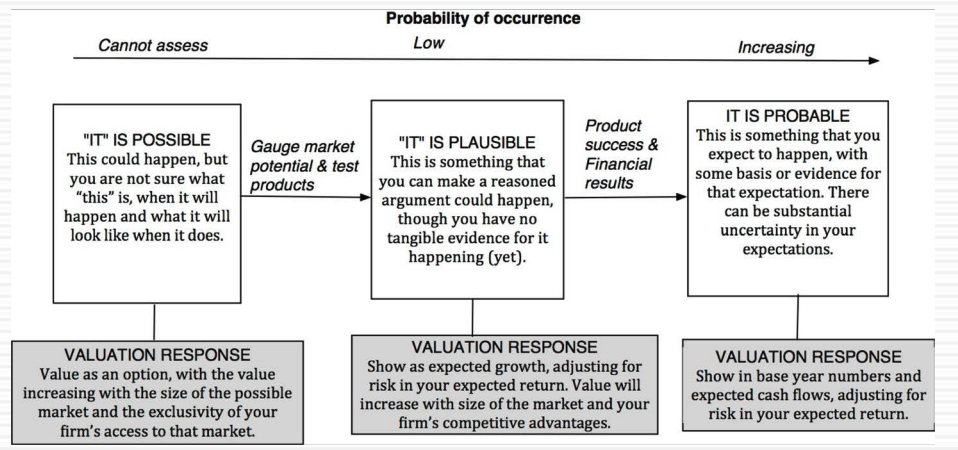

First, we must have a firm grasp of economic first principles and common sense; asking if the financial model being proposed is possible, plausible, or probable?

Source: Aswath Damodaran

Here’s what I mean…

Whenever we are looking at deals here at Equifund, the overwhelming reason we say no to a deal is this: the financial model doesn’t “pencil out.”

More often than not, the management team’s financial model asks you to believe a miracle is going to occur.

Alternatively, there is a financial model that looks reasonable, but once we ask them for the source of these assumptions, we find out “yeah we just made them up.”

Why does this happen? Usually it’s because the management team is trying to justify a valuation that is WAY above market, and they need an equally absurd financial model to justify the price.

This is why underwriting and due diligence are such critical elements when investing!

In order to set the price – and therefore, manage valuation risk – we have to be able to connect the Narrative to the key elements in the financial model that drive Valuation.

Unfortunately, the vast majority of non-professional investors simply don’t have the time, skills, or resources to do any sort of meaningful due diligence.

And even if you did, it is a fact of early-stage investing that everything is uncertain.

It doesn’t matter how many experts you consult, how much data you collect, or how complex the models you make…

You simply cannot remove the uncertainty from the process.

According to Damodaran, as the company matures, you have to be willing to move from:

Rule-based valuation to principle-based valuation

Being reliant on historical data to market-based best judgments

Wanting the right answer to being okay with being wrong (sometimes horribly so).

Point estimate valuations to valuation distributions

And as companies age, the metrics used to value the business may change – from revenue proxies (like Letters of Intent) to actual revenue to earnings to book value.

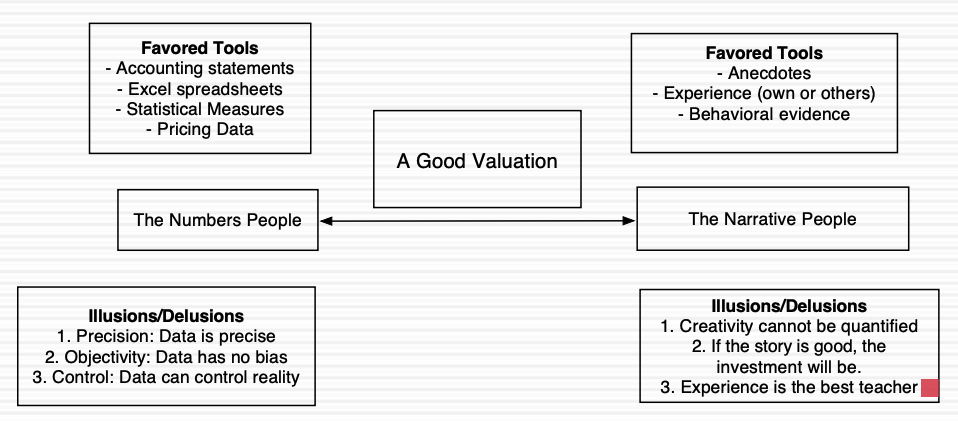

Final Thoughts: From Data to Wisdom

One of the maxims we believe here at Equifund is this – you may forgive us for being wrong, but you will never forgive us for being sloppy.

To say it clearly, as smart as we think we are here at Equifund, we are fully aware that some deals – no matter how “good” we think they are – go bad for reasons outside of our control.

But regardless of the outcome, we believe the best way to build trust with our members is to demonstrate quality thinking.

Instead of relying on fear and greed to put you into an emotionally vulnerable position which can be exploited in the short term…

We want to help you build the intellectual infrastructure you need to operate from First Principles and learn how to think for yourself.

And with this in mind, Private Capital Insider is designed to explain how we think about the markets so you can see the world the way we do (and hopefully, by understanding our thinking, you will put more faith in our decision making).

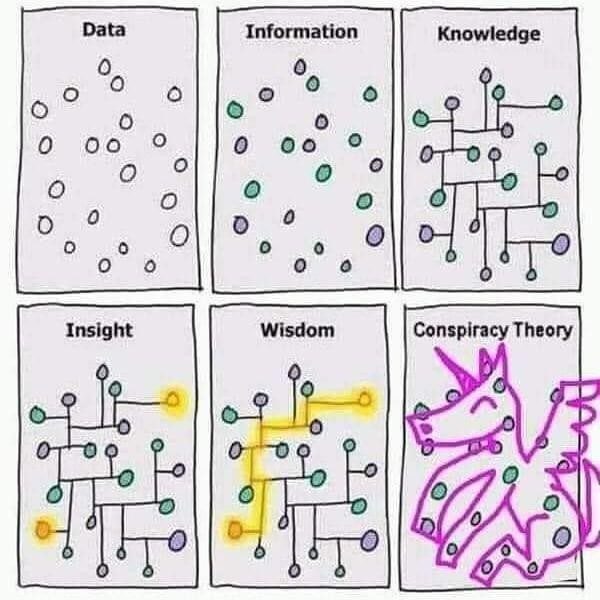

According to Russell Ackoff, a systems theorist and professor of organizational change, the content of the human mind can be classified into five categories:

Data: symbols

Information: data that are processed to be useful; provides answers to "who," "what," "where," and "when" questions

Knowledge: application of data and information; answers "how" questions

Insights: the appreciation of "why"

Wisdom: evaluated insights

The first four categories deal with the past – what has been or what is known.

And even though Epistemology is the philosophical analysis of what is True…

It is only the fifth category, wisdom, that deals with the future.

Wisdom is what allows you to follow a sound course of action, based on the systems of knowledge you possess.

And it is wisdom that we will all need to rely on as we invest – and live – in the face of fear, uncertainty, and doubt.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |