- Private Capital Insider

- Posts

- 📈 Oil, Gas, and the Texas Paradox

📈 Oil, Gas, and the Texas Paradox

Private Capital Insider: Weekend Edition

Equifund: Weekend Edition

April 14, 2024

While everyone else is talking about Morgan Stanley’s anti-money-laundering problems, Rivian and Lucid closing at all-time lows after Ford slashed prices on its electric pickup truck, and O.J. Simpson passing away…

Here are the stories you haven’t been hearing much about:

Oil Rally Is Driving Texas Gas Prices Below Zero: There’s so much natural gas flowing from Texas wells that producers are paying customers to take it off their hands.

More oil at current prices means more cash. But one hitch is that those wells also produce gas, and right now, the U.S. gas market is glutted — thanks to an unseasonably warm winter that crippled demand.

Stockpiles are nearly 40% above the five-year average. Pipelines are jammed.

What does this all mean for Oil, Gas, and the Texas Paradox?

That’s the topic of today’s Weekend Edition.

-Equifund Publishing

P.S. Interested in investing in oil and gas? Pytheas Energy – an AI-powered, early-stage oil and gas producer operating in Texas – is raising capital on the Equifund Crowd Funding Portal.

The Texas Oil & Gas Paradox: Why too much natural gas could stall oil production in the Permian Basin

While we are obviously in favor of developing renewable energy sources that work as advertised…

As investors, it’s important we take notice when the narrative pendulum begins to swing in the other direction.

The Anti-ESG campaign that’s been running since 2022 appears to have taken hold, and the “rubber” of policy is beginning to meet the “road” of reality.

Not to mention, the return on regional bank lending to oil and gas.

A group of US regional banks is ratcheting up lending to oil, gas and coal clients, grabbing market share as bigger European rivals back away. Source: Bloomberg, April 14th, 2024

Like it or not, we need oil and gas – and will for the foreseeable future.

And as the markets start to call for $100 oil – especially now that Iran has attacked Israel – we could be on the edge of a major shift in the narrative around oil.

Here are some of the headlines (and notable quotes) from this week:

Source: Yahoo Finance, April 5, 2024

“There are a lot of geopolitical reasons to be concerned about supply risks," Claudio Galimberti, senior vice president at Rystad Energy, told Yahoo Finance this week of oil's upward price trend.

"Therefore, I would say triple-digit oil prices are not that far at this point. And this is where we could end up in the next couple of months for sure,” he added.

“Russia is a major oil producer. So the moment you have potentially 500,000, [or] a million barrels a day temporarily impacted — this is when you can see oil prices notch up potentially another $5, $10, and then you are in triple digits,” said Galimberti.

Source: MarketWatch, April 8, 2024

“Brent has rallied to $91/bbl because the market is now pricing in a firmer demand outlook and some geopolitical downside risks to oil supply, which together have boosted positioning and valuation,” says Goldman.

Source: Forbes, April 9, 2024

Officially, OPEC+ rarely admits its moves are designed to shore up crude oil prices.

However, it knows that the prevailing market conditions give it a measure of control over the direction of the market both to the downside and upside, despite rising non-OPEC production.

But while it would like a sufficiently high price of at least $80 or more, a level that is very high - say $110 to $125 - might well be self-defeating in 2024.

That's because should Brent hit such a high range, its inflationary impact would stop global central banks from cutting interest rates and maintain them at their current elevated levels for longer.

Demand destruction in its wake is something that OPEC+ will not want. A range between $80-90 might well be what it can work with.

To summarize…

Should there be ~500,000 barrels of net supply shortage for some reason, oil could go above $100, and that would be bad for inflation – but really, it’s bad for central bankers.

In somewhat related news, inflation also seems to be bad news for Wall Street bankers, as JPMorgan is now leading the anti “higher rates fight inflation” narrative (probably nothing, right?).

Source: Bloomberg

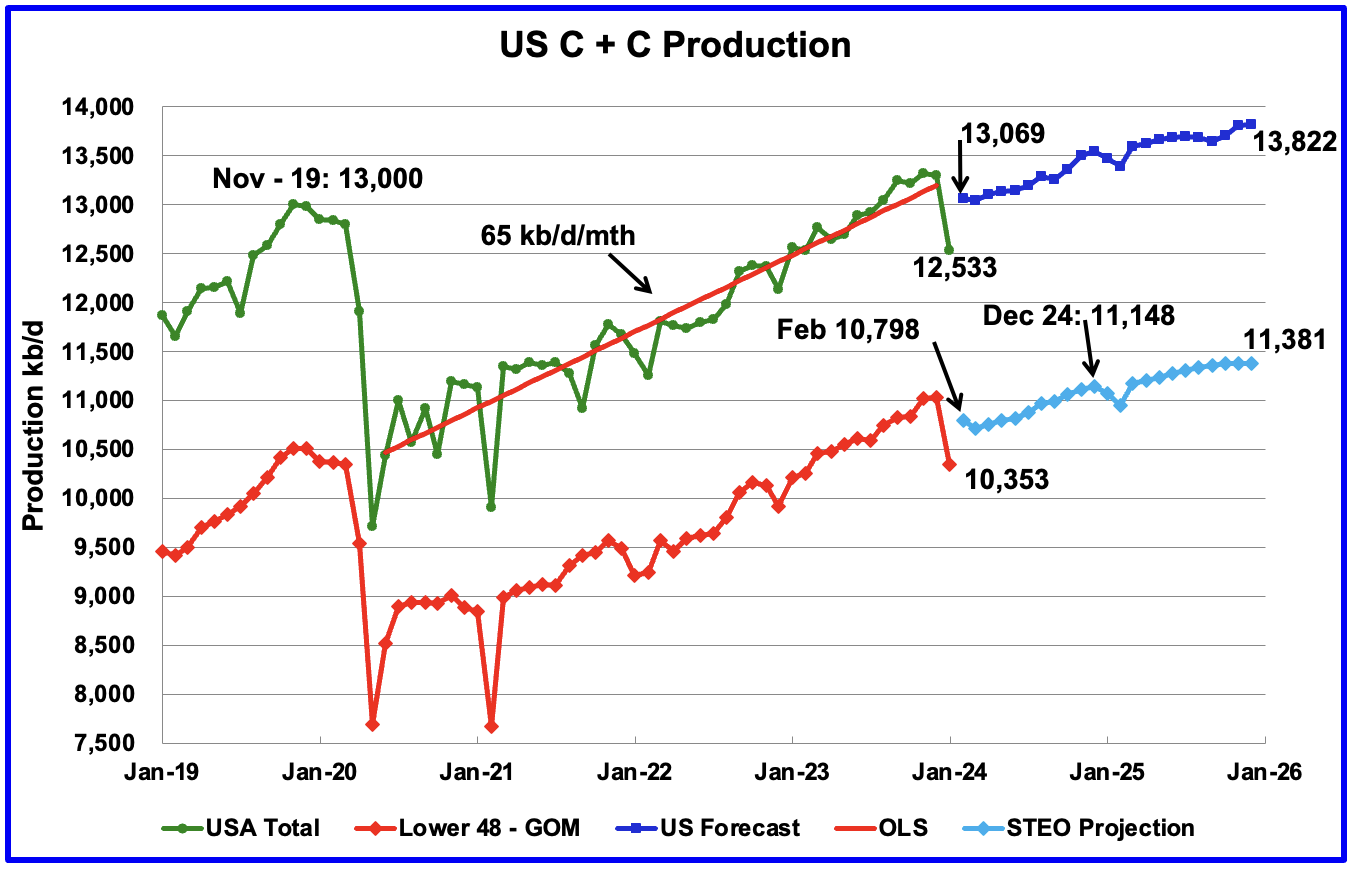

As a reminder, we’ve already had the January EIA forecasts revised down by ~762,000 barrels per day due to “bad weather” (which we don’t buy as the reason why).

U.S. January oil production decreased by 762 kb/d to 12,533 kb/d. The large decrease was due to a severe US winter storm that was spread across most central states. The largest drop came from Texas, 288 kb/d. Source: PeakOilBarrel.com

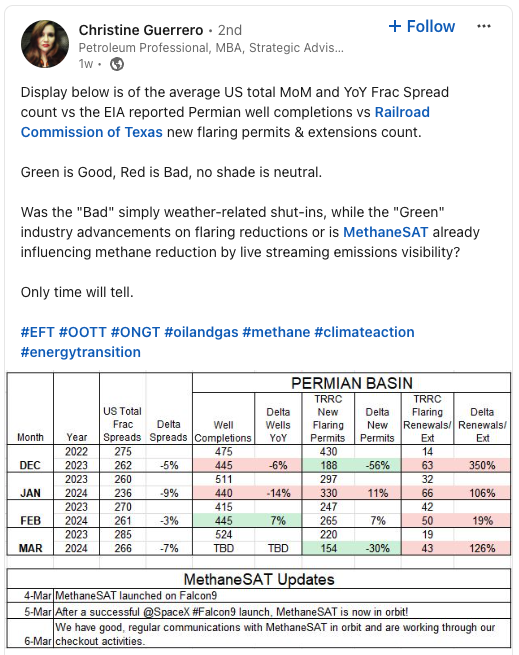

According to Christine Guerrero – former petroleum engineer for companies like Chevron, Hess, and Schlumberger,

I looked back on the history of US oil and gas production, and I had to go back 49 years in order to find an oil drop percentage wise that was as big as what we saw in January from the previous December.

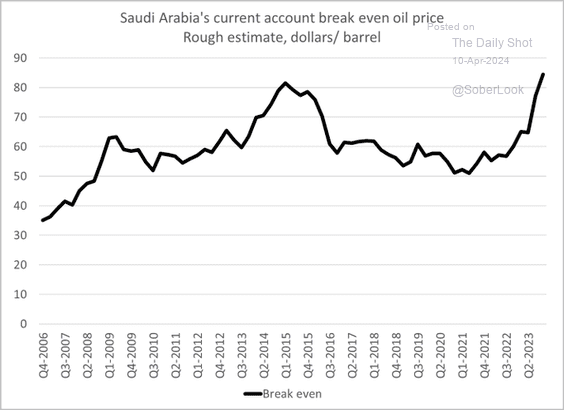

But here’s the part of the story most people miss. Saudi Arabia – who seems to care about having a balanced budget (imagine that) – needs oil prices in the ~$90 range.

Source: @AyeshaTariq

Why does this matter? Because the oil wars have been – in many ways – a war between bankers (and their ability to maintain financing for oil investments during low prices).

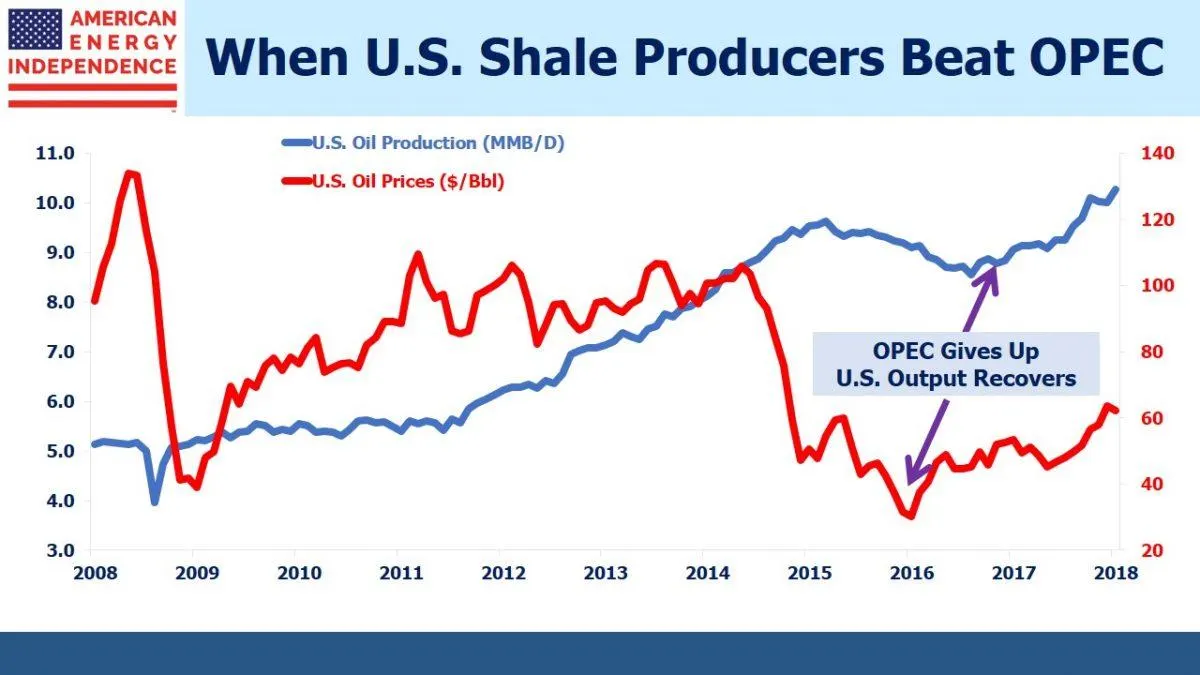

For example, in the Oil War of 2014, here’s the story most people have heard: With American shale hitting the market, Saudi Arabia decides to flood the market in an effort to collapse prices and bankrupt the U.S. Shale industry.

Prices crashed from above $114 per barrel in 2014 to about $27 in 2016.

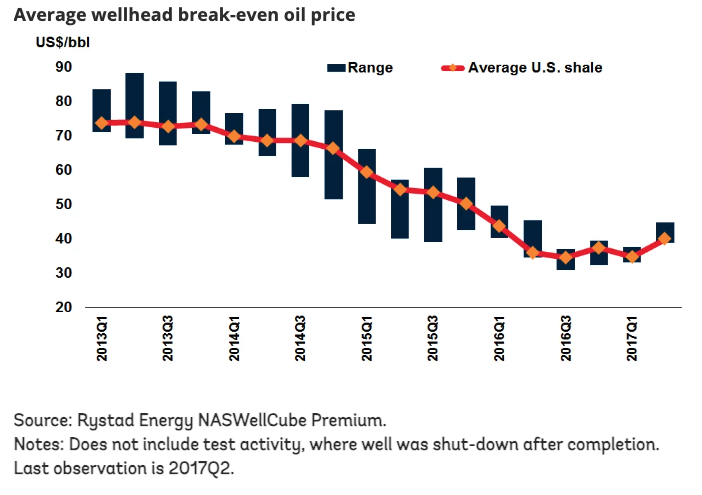

Believing that the new U.S. supply was high cost, they expected a couple of years of ruinously low prices would drive these new producers out of business.

U.S. shale responded with innovation, cost cutting, and major efficiency gains – all of which lowered break-even prices considerably.

After several years of massive government deficits as oil revenues slumped, OPEC capitulates to U.S. Shale, making it the de facto marginal cost producer on the international oil market.

Source: Forbes

In September 2016, Saudi Arabia and Russia agreed to cooperate in managing the price of oil, creating an informal alliance of OPEC and non-OPEC producers that was dubbed "OPEC+."

Here’s the story most people haven’t heard: the U.S. allegedly pressured Saudi Arabia to overproduce crude, and intentionally crash prices on the global market, in order to hurt the export-reliant economies of Russia, Iran, and Venezuela.

The Saudis have shown themselves to use oil politically throughout their recent history. They're quite good at it; they think of oil as a strategic commodity and kind of their key lever of influence globally.

The Saudis are always mindful of oil prices. They always try to keep the oil prices high enough for them to cover [their] budget, but low enough to hurt the Iranians.

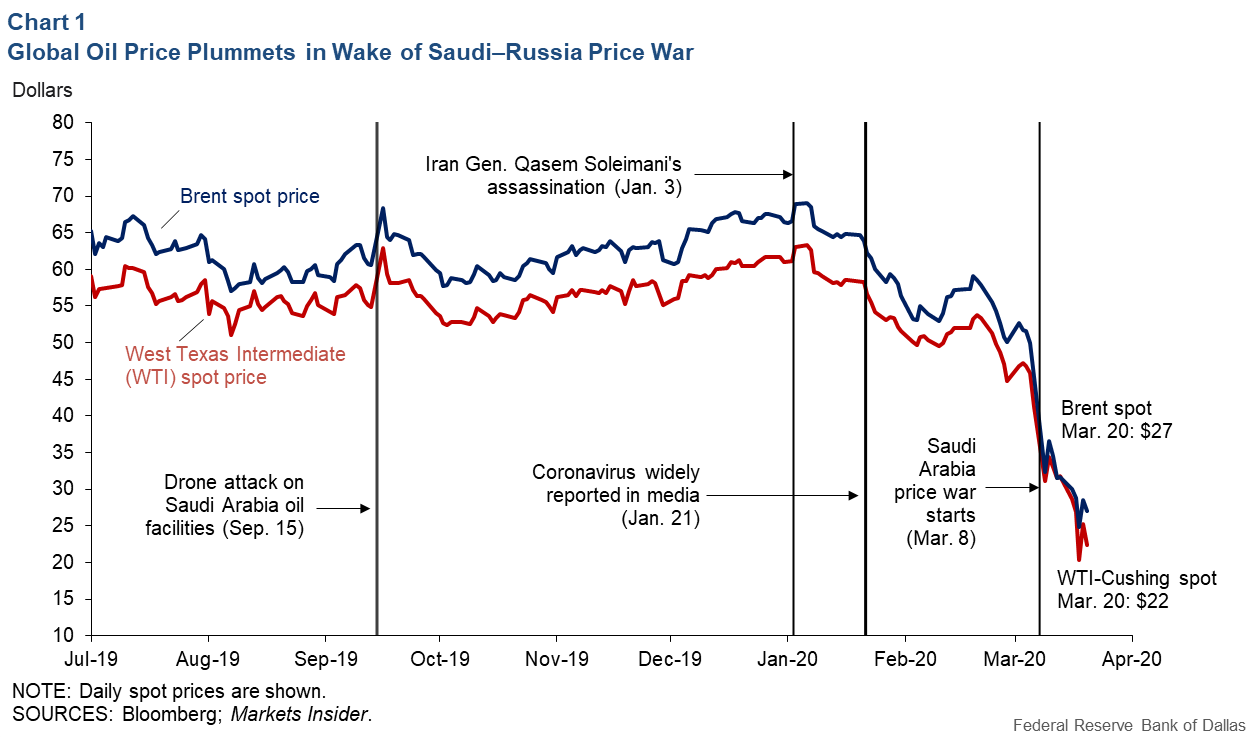

Since then, we’ve also had the alleged Saudi-Russia Price War during COVID that sent prices negative.

It stands to reason that Saudi Arabia and Russia would terminate the price war as soon as U.S. shale oil production has been greatly diminished.

This would provide an opportunity for coordinated supply cuts among the remaining oil producers and for persistently higher oil prices.

As prices rise, however, capital markets would view U.S. oil producers as financially viable once again, making an eventual U.S. shale oil production comeback likely. Thus, it seems unlikely that this price war will permanently vanquish the U.S. shale oil sector.

Moreover, a Saudi victory may prove to be Pyrrhic. Saudi Arabia already experienced a major drawdown in its foreign exchange reserves following the sharp decline in the price of oil after June 2014.

If Saudi Arabia exhausts its hard-currency reserves with an extended price war, it will be unable to similarly threaten U.S. shale oil producers and other oil producers in the future.

Thus, the global oil market will never be the same.

For a while now, the world has assumed that Saudi Arabia can produce oil at a price as low as $10 per barrel from some fields, with Russia arguably requiring an average price of $20 or $30…

But what if those assumptions are wrong?

Or more importantly, what if they simply don’t have the available “swing” capacity to increase production – regardless of oil prices?

Especially if Houthi rebel attacks in the Red Sea intensify, and continue to delay shipments from the Middle East…

Or if, oh I dunno, Iran attacks Israel.

If that’s the case, this means we’d have to expect a significant amount of supply to come online from somewhere outside the three largest players.

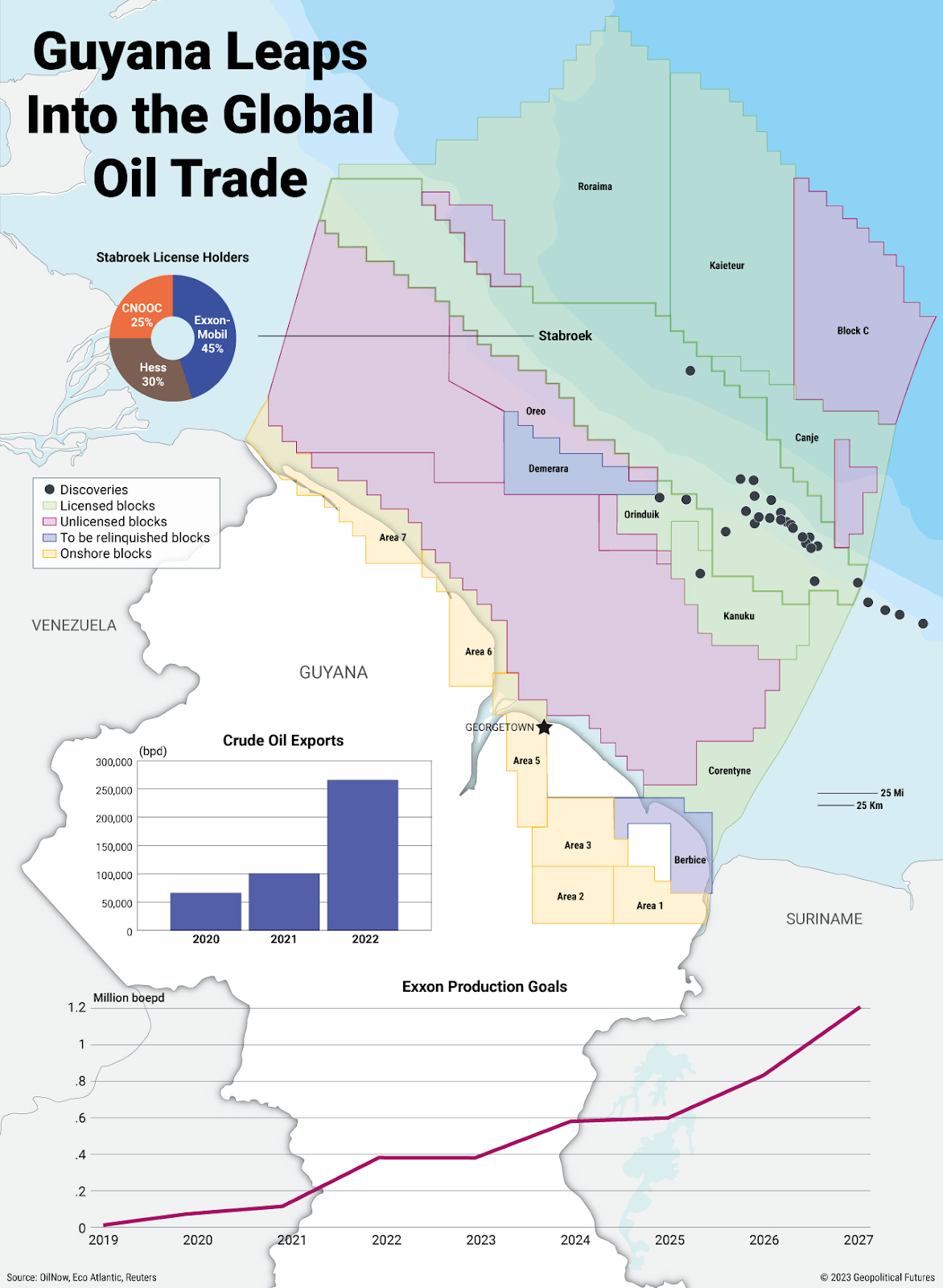

While there’s a lot of excitement around the major oil find in South America’s Guyana – which has been described as a “transformative” discovery…

Source: Geopolitical Futures

We haven’t even hit the seasonal summertime demand, but are already seeing signs of a supply squeeze forming – Mexico, the U.S., Qatar and Iraq cut their combined oil flows by more than one million barrels a day in March.

Source: Bloomberg

The supply squeeze comes as demand is ramping up. US refiners are preparing to boost fuel production for the summer, when millions of Americans take to the roads and gasoline consumption peaks.

Gasoline stockpiles on the populous East Coast are tightening and manufacturing activity in the US and China is also signaling a boost in fuel use.

In Asia, refining margins are around 50% higher than the five-year seasonal average, suggesting healthy demand.

Crude’s rally has snarled the Biden administration’s plans to refill emergency US oil reserves, which reached a 40-year low following an unprecedented drawdown after Russia’s invasion of Ukraine.

It’s also a political risk for Biden as prices for food and energy remain stubbornly high.

Oil’s advance threatens to push retail gasoline, now near a daily national average of $3.60 a gallon, toward $4, a key psychological level.

That’s contributing to concern that commodities will reverse the recent slowdown in consumer price gains.

But again, we come back to the critical question here about supply…

What if U.S. producers don’t have the amount of supply they think they do? Or even if they did, what happens if they – for whatever reason – can’t increase production?

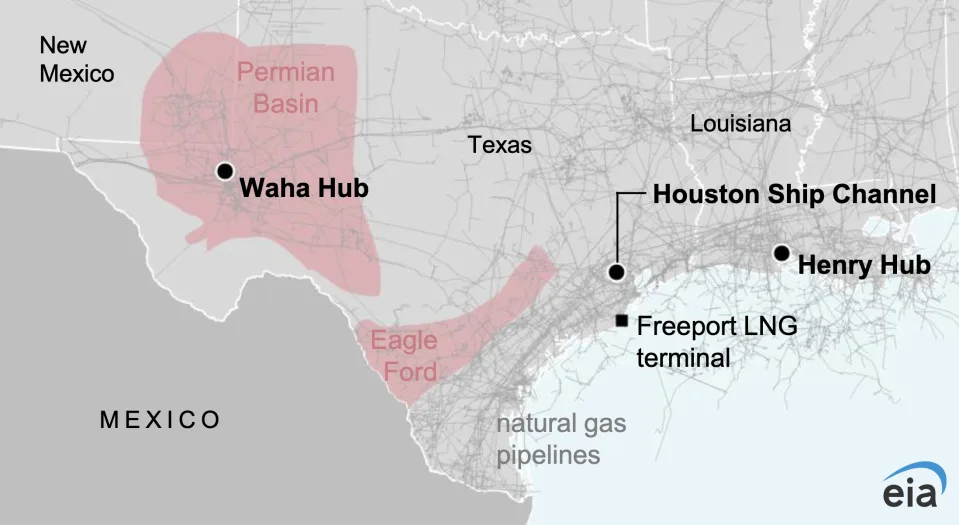

Strangely enough, the limiting factor in Permian oil production is pipeline capacity for natural gas.

The lack of this pipeline takeaway capacity may limit Permian Basin oil production in 2024 since companies cannot simply burn off the associated gas into the atmosphere,

At West Texas's key trading spot, the Waha Hub, prices have been negative for the majority of March and into April, according to government data released this week. That means producers have essentially paid someone to take it off their hands.

Why? Because in the Permian, the main business model is producing crude oil – any natural gas produced is, in many ways, considered a “free” byproduct.

In fact, once upon a time, oil companies would simply burn it (called “flaring”) to get rid of it.

The natural gas production stays oversupplied to the point that you can't add any more to the existing lines.

Between now and August / September we're probably in a situation where you cannot grow oil production out of the Permian – which is the biggest component of US oil production.

That might actually mean that between now and September / October you don't get any incremental oil from the US no matter what the price is.

When you don't have a pipeline to put your gas in, if you want to increase your oil production there's only one thing that you could do … flare your natural gas into the atmosphere.

Today, flaring is largely considered a “no-no” and generally frowned upon.

Not to mention, a new satellite – called MethaneSAT – backed by Alphabet Inc's Google and the Environmental Defense Fund, launched with a mission to pinpoint the oil and gas industry’s methane emissions from space.

The Environmental Defense Fund said the data will bring accountability to the more than 50 oil and gas companies which, at the Dubai COP28 climate summit in December, pledged to zero out methane and eliminate routine gas flaring.

This, in an effort to “help those preparing to comply” with forthcoming methane regulations in the EU and the U.S., including a methane pollution fee.

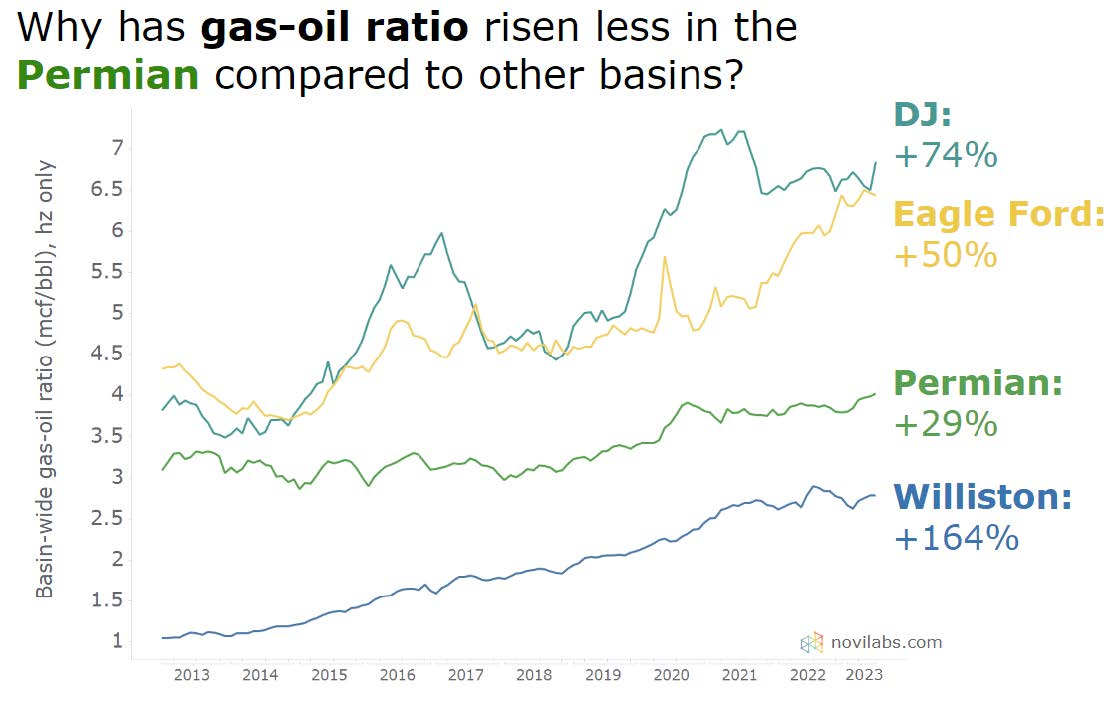

However, as oil fields age, they tend to get gassier – about one-third of all the flow from the Permian Basin is now associated gas, with wells becoming gassier and wetter farther west in the Delaware Basin of West Texas and southeastern New Mexico.

With that said, the Gas to Oil ratio for the Permian has been far more stable compared to other unconventional plays.

Source: NoviLabs

On one hand, there’s a lot to like about natural gas, if you’re into low-cost and relatively “clean” fuel sources.

But unless you’ve got enough infrastructure to actually MOVE that gas somewhere, oil production is artificially capped.

Also according to Guerrero,

If I look back a year ago at what production was doing in the Permian Basin, whatever it was growing a year ago, we're most likely not physically able to grow that much today because we don't have that many wells being completed.

I even went so far as to jump into the Texas Railroad Commission and started looking through their various permits.

A lot of times when a well is being drilled, they'll have a permit for flaring. For the month of March last year there were 220 new flaring permits issued. For this March, there was a only 154 permits issued

That's a 30% reduction potentially in the wells that are being drilled today than were being drilled a year ago

I promise you we have not had any technology breakthrough that has allowed us to produce much more oil and gas with 30% less wells.

So again, there's all these little key points of data that when you put them altogether you start to see “wow. we truly are bottlenecked right now, because we didn't build ahead soon enough to meet our growth expectations”

And as we’ve already covered, because of the dramatic decline rate of “short cycle” shale wells, it requires constant drilling to simply maintain production (let alone increase it).

Not to mention the fact that bringing these short cycle wells online requires a tremendous amount of materials and labor…

A key reason why deep-water exploration and production dominates in terms of investment interest.

Does all this point to a coming oil supply squeeze?

As usual, we don’t like to make predictions about the future… but we do like to track “Narratives and Numbers,” and how they change over time.

While we came into 2024 with record forecasts for oil production…

Based on revised numbers coming in lower than expected, if February and March numbers also miss forecasts, we could see a major shift in the “$100 Oil” narrative, which could cause everything to reprice higher.

Interested in learning more about investing in oil? Go here now to check out Pytheas Energy – an AI-powered oil and gas producer currently raising capital on the Equifund Crowd Funding Portal.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |