- Private Capital Insider

- Posts

- 📈 Investing in American “Craft Oil” Producers

📈 Investing in American “Craft Oil” Producers

The Insider’s Guide to Investing in Small Oil & Gas Plays

Jake @ Equifund

April 04, 2024

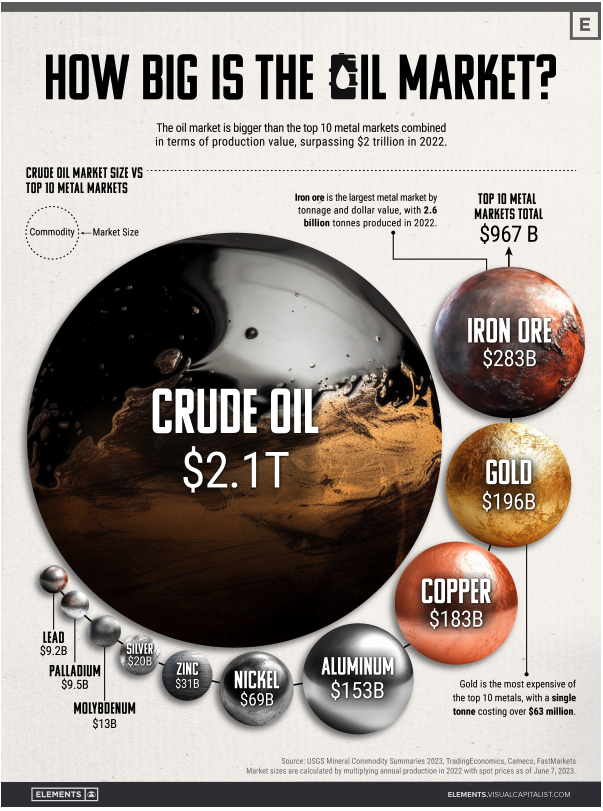

While it’s tempting to think of the $2.1 trillion crude oil market as being completely controlled by a small handful of players…

Source: Visual Capitalist

Just like pretty much every other market, oil and gas investors have the option to invest in larger companies that often offer downside protection, income, and reasonable growth…

They can also opt for smaller – significantly higher risk and more volatile – companies that may offer the chance for huge upside returns.

In the oil industry, these smaller companies – known sometimes as “Craft Oil” – are usually “pure plays,” which are hyper-focused on one part of the value chain; such as exploration and production, refining, or marketing.

They may be more likely to develop new technological innovations that can drive the industry forward, and eventually be acquired by a larger company.

But before considering an investment in the “Craft Oil” space, it’s important to understand the mega trends that have the biggest potential impact on your returns.

That’s the topic of today’s issue of Private Capital Insider.

-Jake Hoffberg

P.S. Interested in investing in a “Craft Oil” play? Pytheas Energy – an AI-powered, early-stage oil and gas producer operating in Texas – is raising capital on the Equifund Crowd Funding Portal.

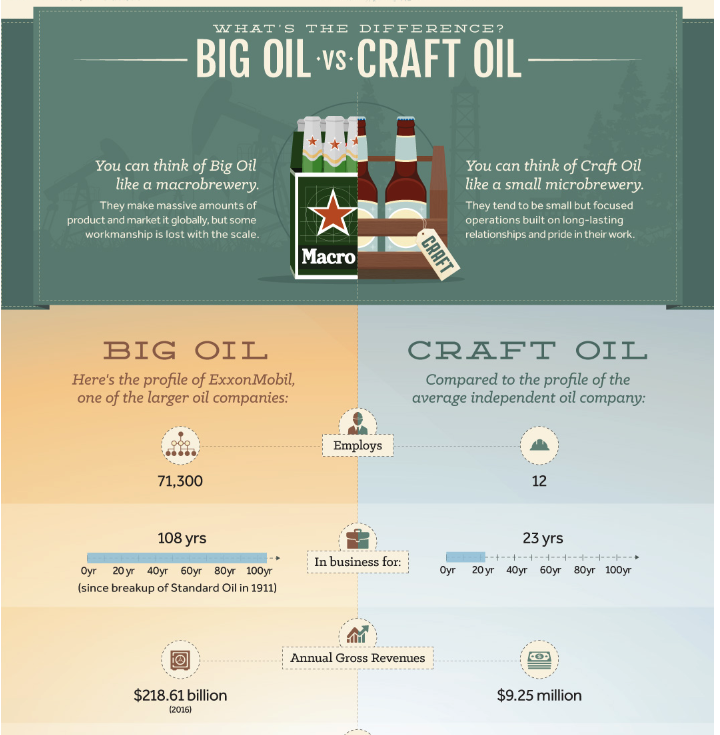

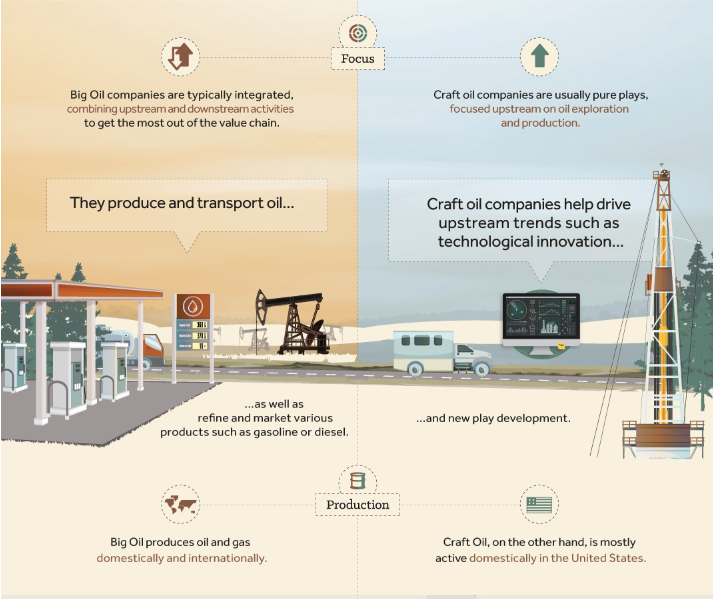

Big Oil vs Craft Oil

Big Oil consists mainly of large, vertically integrated companies that combine upstream exploration activity, midstream transportation activity, and downstream refining activities.

Source: Visual Capitalist

Because of their size, they typically employ tens of thousands of people, generate billions of dollars in revenue, and are responsible for producing, transporting, refining, and marketing much of the world’s oil products (like gasoline and diesel fuel).

Source: Visual Capitalist

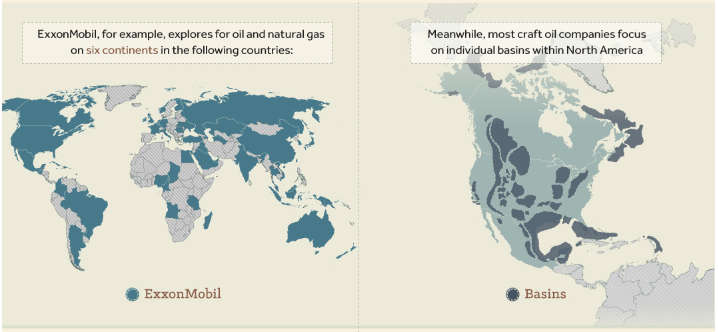

They also have the infrastructure to invest in developing long-term oil reserves – in particular, offshore drilling – and operate at an international scale; for example, ExxonMobil explores for oil and natural gas on six continents.

On the other hand, “Craft Oil” producers primarily focus on individual basins within North America.

Source: Visual Capitalist

Interestingly enough, Big Oil drills only 5% of all American oil wells.

The other 95% of all domestic wells are drilled by the smaller “Craft Oil” companies who focus mainly on the large North American oil basins.

These small companies are usually “pure plays” that are hyper-focused on one part of the value chain – such as exploration and production.

They also may be more likely to develop new technological innovations that can drive the industry forward, and eventually be acquired by larger companies.

Source: RSM

And as the exploration and production industry begins to grapple with the problems of finding new reserves, many companies are exercising increased caution, and shifting their strategies to target more profitable and geologically better-understood regions.

More specifically, we are seeing incredible consolidation in the Permian Basin.

While supermajors operating in the Permian Basin have enough quality inventory to last an estimated 25 years at the current pace of drilling, private exploration and production companies would have around 11 years remaining at the current pace.

If these companies start drilling again at 2022’s pace, you’re going to exhaust that inventory in a shorter period of time.

For some E&Ps that could be five years or less.

The likely outcome of all this activity? Once this current consolidation cycle is completed, the available acreage, in large part, will be spoken for.

The players that remain will have amassed vast swaths of acreage, and there will be two pressing questions:

How can we manage this portfolio of assets as efficiently as possible?

How can we reduce our cost basis, reduce our carbon footprint, and also maximize the profitability of the assets we have?

The companies who can successfully answer these questions – and transition to the new reality – will stand to capture the enormous opportunity ahead.

A New Era Of Oil: The shift from big discoveries to asset management

If the last 100 years have been about long-term bets on land assets, innovation at the wellhead, and maximizing short-term profits to capture windows of favorable pricing…

The next decade will likely shift toward managing assets, maximizing long-term profitability, and handling environmental issues.

Even though Big Oil will almost certainly be the biggest winner of this new paradigm, thanks to their tremendous economies of scale, they have the same weakness all large commodity producers have – they have to focus on large, producing projects.

While mergers and acquisitions provide opportunities to consolidate new assets, and increase focus on what’s called “core assets”...

They also tend to force a divestiture of “non-core assets,” in order to free up resources as wells become “marginal.”

But interestingly enough, research suggests only ~30% of oil and gas is ever extracted from most existing wells using conventional methods.

Crude oil development and production in U.S. oil reservoirs can include up to three distinct phases: primary, secondary, and tertiary (or enhanced) recovery.

During primary recovery, the natural pressure of the reservoir or gravity drives oil into the wellbore, combined with artificial lift techniques (such as pumps) which bring the oil to the surface.

But only about 10 percent of a reservoir's original oil in place is typically produced during primary recovery.

Secondary recovery techniques extend a field's productive life generally by injecting water or gas to displace oil and drive it to a production wellbore, resulting in the recovery of 20 to 40 percent of the original oil in place.

However, with much of the easy-to-produce oil already recovered from U.S. oil fields, producers have attempted several tertiary, or enhanced oil recovery (EOR), techniques that offer prospects for ultimately producing 30 to 60 percent, or more, of the reservoir's original oil in place.

Here’s why…

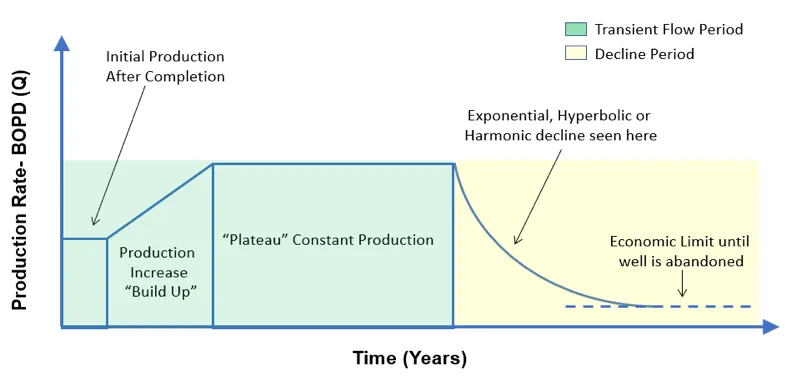

In theory, every oil and gas well goes through something called a decline curve - a method used to determine estimated ultimate recovery for an oil or gas reserve.

The 3 decline curves – exponential, hyperbolic, or harmonic – are important because they are used as one of the factors in determining the value of minerals or land. Source: Rock River Minerals

With conventional wells, the decline curve is often slow and steady.

With unconventional wells, it’s anything but.

For these reasons, it’s critical for anyone interested in investing in oil and gas plays to understand what we call…

The 5 Profit Killers of Shale Wells

At their foundation, oil exploration plays have two major challenges:

Oil reserves eventually run dry, so there is a constant need to drill for more oil

Exploration is an extremely capital-intensive business, which carries high risk due to price volatility.

This creates an interesting problem. In order to fund operations, we need high oil prices and access to credit facilities.

In an era of near zero interest rates, epic monetary expansion, and booming oil prices... it’s relatively easy to get access to investor capital and credit facilities.

However, when the inevitable downturn comes, lenders lose their appetite for these sorts of investments, and these companies often go under.

And this problem is only made worse due to the nature of unconventional wells.

Challenge #1: High Exploration Costs

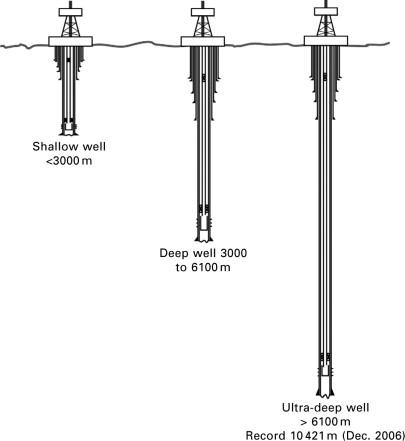

In oil exploration, wells are typically defined by how deep the company needs to drill in order to find oil.

They’re split into three categories. Shallow, deep, and ultra-deep.

Shallow wells – which are anything less than 3,000m (or <10,000 ft) – represent the conventional oil and gas reserves that are now scarce.

That’s why the majority of newer fields in production today are deep wells, which reach depths from 3000m to 6100m (10,000−20,000 ft).

The problem with deep wells should be immediately obvious. The deeper the drilling, the more expensive it gets; both for successful drills and dry wells.

But the initial drilling costs are only the beginning.

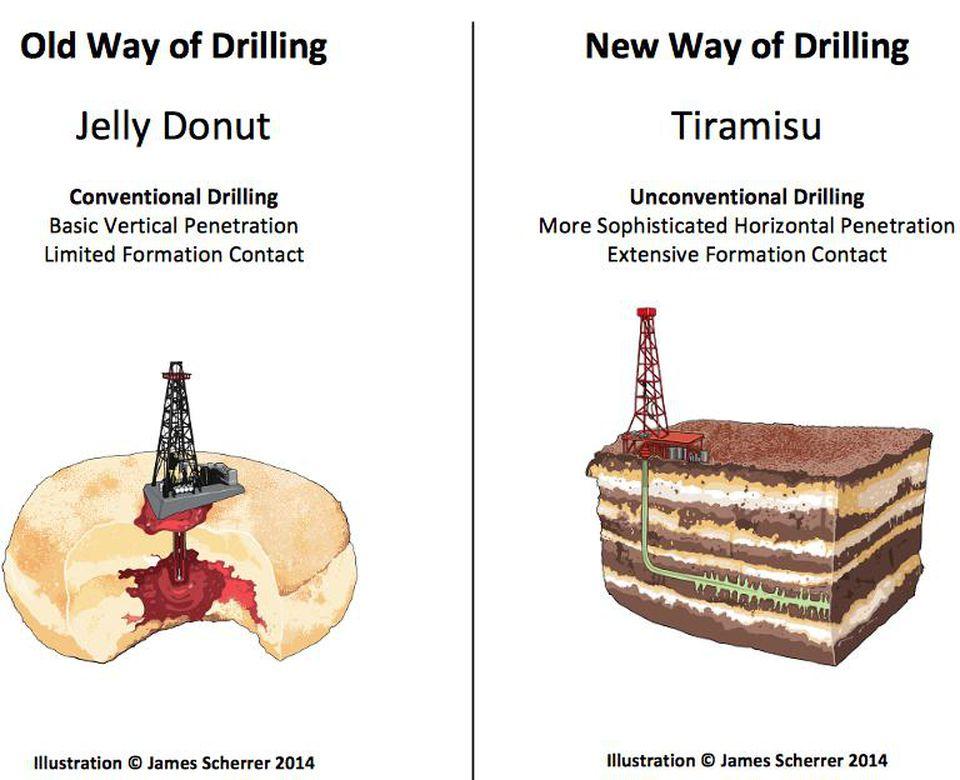

Up until recently, oil was recovered using vertical drilling – or “conventional” – methods. The method is rather simple; drill a hole down into the earth until you hit a patch of oil. Assuming there’s enough pressure in the well, oil will come out the top.

In the early stages of the well, pressure is provided by the gas (or water) already in the reservoir. But as it depletes, oil has to be pumped – or otherwise “lifted” – from the wells.

If you’ve ever seen one of these contraptions, called a “pump jack,” that’s what they’re for.

But only 30-35% of the well is recoverable with these methods. To get the rest, drillers boost pressure by injecting water or gas into the reservoir.

Once that stops working, they move to the final step called “enhanced oil recovery” or EOR. This is where fracking comes into the picture.

In conventional wells, going through this multi-stage process means producers can sustain flow for years, or even decades.

But in the case of unconventional shale oil wells, drillers go right to the EOR stage.

Why? Because shale oil is not produced from a reservoir. It’s trapped inside a nearly impenetrable rock.

And because of this, shale wells ramp up fast, and fall off fast.

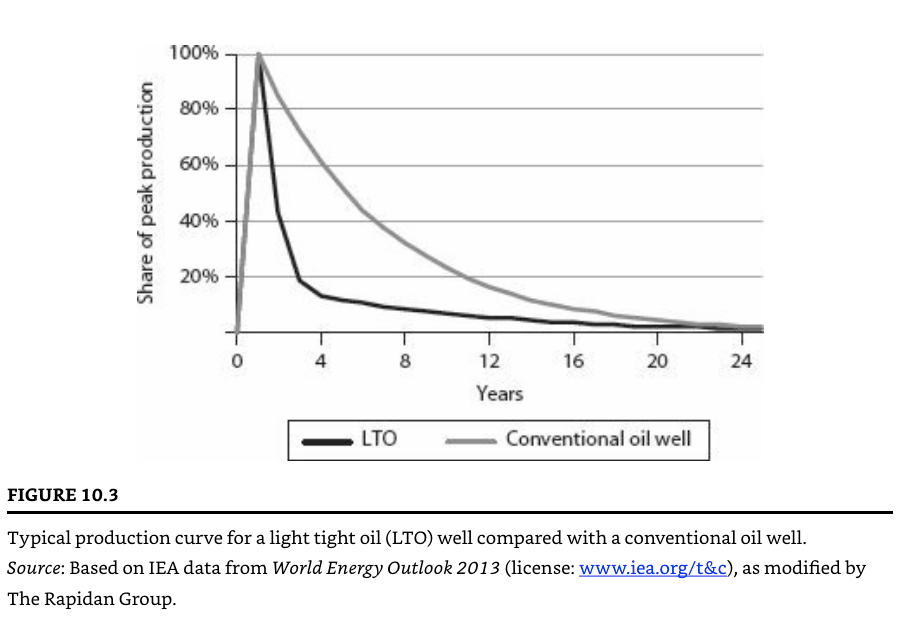

A typical shale well in the Bakken region of North Dakota declines 65% in the first year, 35% in the second year, 15% in the third, and 10% per year afterward.

As indicated in the chart below, within four years, a shale well’s production has fallen to below 20% of the initial level; A conventional oil well is still producing at between 70-80% of its initial rate.

This steep decline rate creates a huge problem. In order to maintain (or grow) shale production, there’s a constant need to drill new wells.

But the bigger problem lies in the cost to not only drill, but maintain operations.

Challenge #2: High Operational Costs

With conventional wells, once they’re drilled, they’re relatively inexpensive to run. But unconventional wells require much higher ongoing operational costs; shale production requires not just drilling but then fracking and often re-fracking the same wells.

Because the majority of shale wells are drilled by the smaller “Craft Oil” companies – and due to the speculative nature of the business – the day-to-day operations are usually handled by third-party contractors.

This adds an additional premium to the already expensive costs to continue drilling for new reserves.

When oil is trading above $80 a barrel, and you need to move fast, the economics make sense. But once prices dip, it usually means an over-leveraged operation that can’t afford to pay people to continue pumping oil.

With conventional wells, turning off production – or “shutting in” wells – is a relatively simple matter.

But with unconventional wells, they can’t be easily “shut in” or “re-opened” on command. There are real costs to doing this.

“Turning off” shale oil is more like shutting down a manufacturing plant than turning a spigot. Bringing wells back online often means additional costs to re-pressurize the well. And if not done properly, it could mean permanent loss of recoverable reserves.

But even more problematic is the deal structure most shale companies have with the landowners: If they stop drilling, they could lose the lease and opportunity to produce in the future.

Combine this with the typically overleveraged producer carrying debt, it means in order to make interest payments and meet stricter credit conditions, they needed to maintain or even increase output.

That’s why shale producers are incentivized to get as much oil out of the ground as fast as possible.

However, the race to get oil out of the ground is met by the problems with storage and transportation costs.

Challenge #3: High Storage and Transportation Costs

Again, because smaller “Craft Oil” players drill the majority of new shale wells, it means they’re at the mercy of market forces when it comes to storage and transportation costs.

During boom times, they’re competing against all the other producers for access to pipelines. And if they can’t, it means they have to ship by land at greater costs.

Additionally, if they don’t have access to storage during downtimes, it means they can’t continue to pump during depressed oil prices and sell later, when prices rebound.

But perhaps the biggest problem with unconventional wells is the environmental costs, which are both expensive and politically unpopular.

Challenge #4: High Environmental Costs

Exploration and production companies face two major environmental issues:

They need a massive amount of water to drill for new wells

They have to do something with the large volume of wastewater that comes up from the wells once oil and gas is extracted

While water usage varies by region and specific wells, overall, water usage is rising. In 2008, an average of just 5,618 barrels of water were used for the injection stage of fracking, according to the USGS. In 2014, that ballooned to 128,102 barrels of water for an oil well, and 162,906 barrels for a gas well.

A lot of this increase is due to the shift from conventional vertical wells, to unconventional horizontal wells.

Source: Visual Capitalist

Simultaneously, the Government Accountability Office estimates that 40 of 50 states have at least one region that will face some kind of water shortage by 2023. This crisis has increased social and regulatory pressures on oil and gas firms, while making the supply of usable water less dependable.

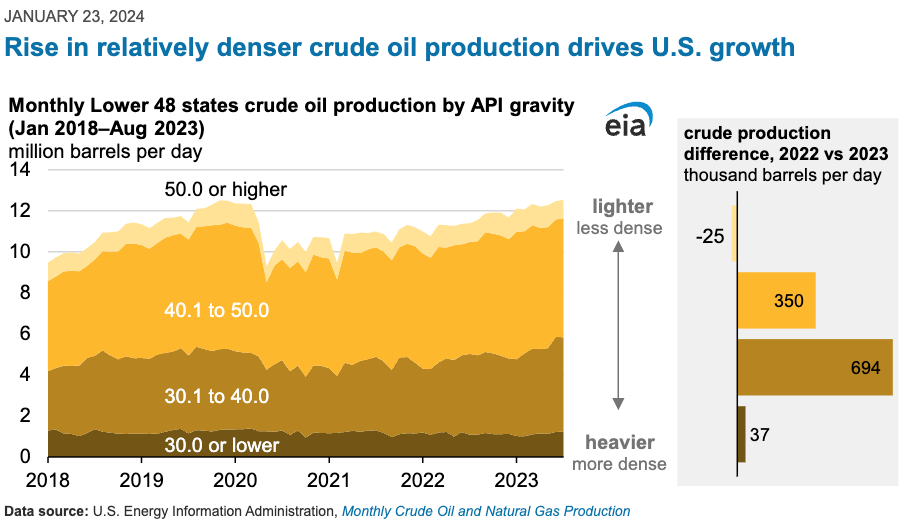

But the final challenge is one that is just beginning to show its effects: the quality of shale oil, and the impact on refinery economics.

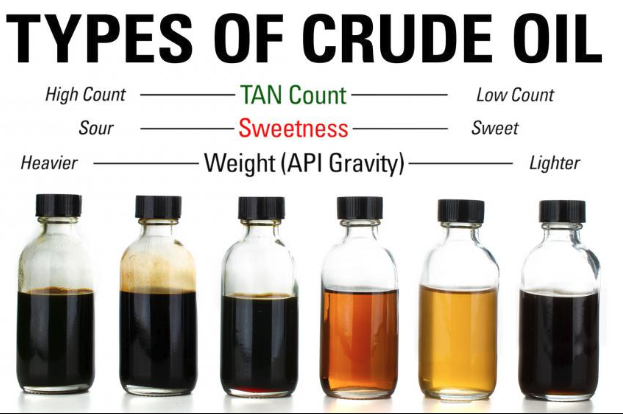

Challenge #5: Oil Quality

Eventually, all oil has to be refined into petroleum products for commercial use. But not all oil is created equal.

Source: Kimray

Like any commodities market, the highest quality - most in demand - stock will always fetch a premium price.

At a high level, oil is measured by two important metrics.

Weight (API): this refers to how “heavy” or how “light” the crude oil is

Sweetness (Sulfur Content): high sulfur oil is called “sour” and low sulfur oil is called “sweet”

Total Acid Number (TAN) Count: This is the measure of how corrosive the oil is. If a crude has a high TAN number, producers must use more robust metallurgy than is standard, so their processes can handle that corrosivity and keep the crude in the pipe.

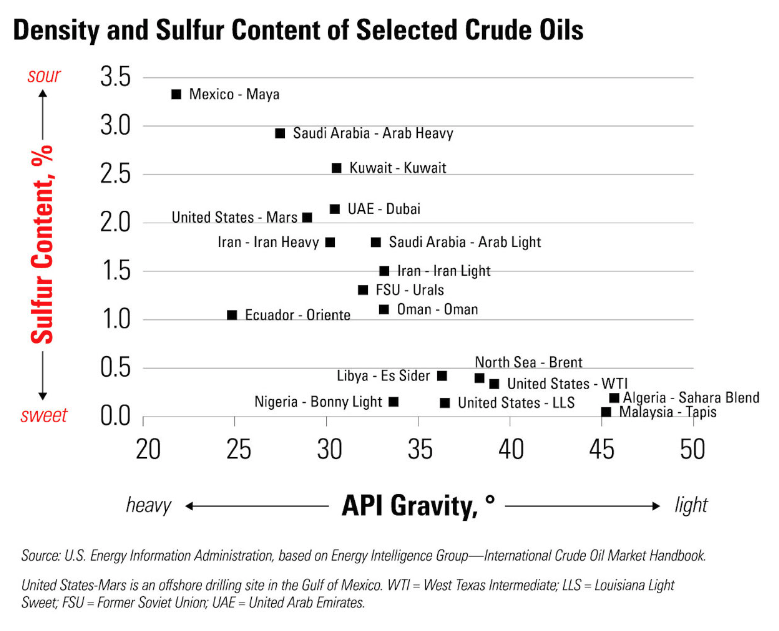

There are over one hundred different crude oils traded on the market today.

These oils are typically labeled by the region they come from, and they have a specific chemical makeup. This graph below shows the sulfur content and weight of some of the most common.

Now, without going into the nitty gritty details of exactly how the refining process works, the important thing to understand is this; there are a lot of steps between getting it out of the ground and turning it into a finished product.

Source: World Oil

Every single step of the process is impacted by the quality of crude oil, all of which impact margins.

Generally speaking, refiners like shale oil because...

It’s relatively cheap to get

A secure domestic supply enables long term, profitable planning

The low-sulfur content means it can be blended with higher-sulfur, low-cost oil

With shale oil, there is a lot of variance from formation to formation, as well as in the same formation.

In practice, this means refiners need to use the right chemical additives to keep equipment clean, costs down, and quality high.

But in the current economic climate, it means there’s more pressure to not only get it out of the ground cheap, but also deliver high quality raw material that refineries can process easily.

Which brings us to perhaps the most important question we have to ask ourselves, if we’re planning to invest in a “Craft Oil” play.

Is there a way to get the upside potential of Craft Oil WITHOUT taking the risks of drilling for shale?

While there is certainly no way to avoid the inherent risk and volatility that comes from investing in any early-stage company – much less an oil and gas play…

There is one notable way to significantly reduce the major risks that come from betting on small explorers/producers.

As it turns out, America has a LOT of what’s known as stripper wells; by IRS definition, an oil or gas well with a maximum daily production below 15 BOED – which is 15 barrels of oil or 90,000 cubic feet of gas per day – over any consecutive 12-month period.

Generally speaking, all these stripper wells come from shallow wells (which are conventional wells by nature).

By current estimates, the United States has 760,000 stripper wells in production – about 400,000 oil and 360,000 natural gas wells.

That means, of the roughly one million active oil and natural gas wells in the United States, 76% are low production stripper wells.

In addition to this, researchers estimate that there are between 2-3 million abandoned (a.k.a. “orphaned”) oil and gas wells in the United States that may have producible reserves, but simply aren’t in operation.

If you’re interested in learning more, go here for the full story on investing in stripper wells.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |