- Private Capital Insider

- Posts

- 📈 Biden's "LNG Ban", Bill Ackman goes retail, and the SEC

📈 Biden's "LNG Ban", Bill Ackman goes retail, and the SEC

Private Capital Insider: Weekend Edition

Equifund: Weekend Edition

February 11, 2024

While everyone else is getting sucked into the “Taylor Swift Super Bowl Psyop,” Tucker Carlson’s interview with Vladamir Putin, and the S&P hitting a new all-time high…

Here’s the short list of stories we’re talking about in today’s issue.

The Biden Liquid Natural Gas (LNG) Ban: Already a hostile party to the American oil and gas industry, the Biden administration – pressured by charities controlled by members of the Rockefeller family, Michael Bloomberg, and other billionaire donors – recently paused new approvals of LNG exports from the U.S.

Bill Ackman launches new retail-focused fund: The hedge fund billionaire is planning to launch a closed-end fund, investing in 12 to 24 large-cap, investment grade, “durable growth” companies in North America, according to a regulatory filing.

The SEC finalizes controversial changes to dealer definition that widely expands their regulatory authority. To no one's surprise, everyone on Wall Street is upset about it.

Let’s dive in,

-Equifund Publishing

P.S. As a reminder, we cannot provide any individualized advice or investment recommendations.

If you need help, please consult with a qualified financial professional who is licensed to provide investment advice.

Biden, LNG, and American Energy

While the editorial team does our best to avoid being political… as investors, politics and policies are unavoidable facts of life.

So before we get into the “he said, she said” of the “Biden LNG Export Ban” drama…

Let’s see if we can establish some objective truth and otherwise create a somewhat stabilized worldview around the American Energy industry.

With an estimated $3 trillion up for grabs each year, the global oil and gas industry has been one of the most important - and potentially lucrative - markets over the past 160 years.

For decades, investments in “Big Oil” have offered investors a much-needed source of income for their portfolios. Companies like Exxon Mobil Corp (NYSE: XOM) and Chevron (NYSE: CVX) have increased their dividend payouts every year, for more than 30 years, at the time of publishing.

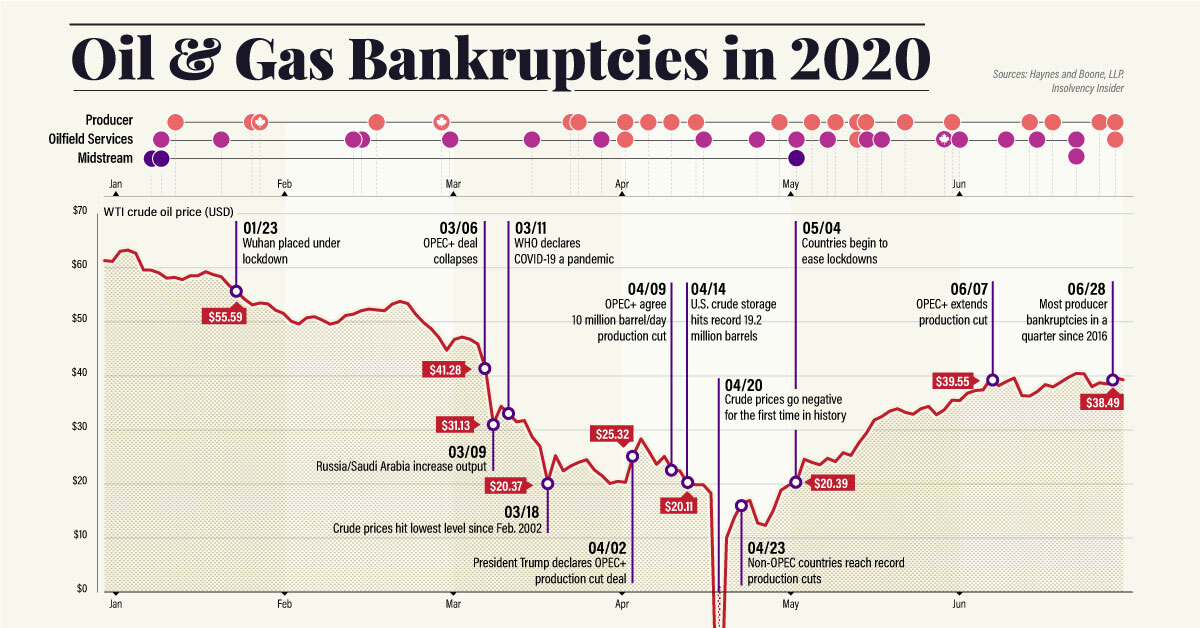

But then, the famous COVID Crash of 2020 happened; over-leveraged oil companies that took on too much debt in 2016 are unable to refinance, causing a wave of bankruptcies that decimated U.S. oil producers.

Source: Visual Capitalist

This inevitably led to a new wave in the ongoing consolidation of oil and gas (O&G) companies – of which the Biden Administration’s hostile posture towards the industry has only accelerated.

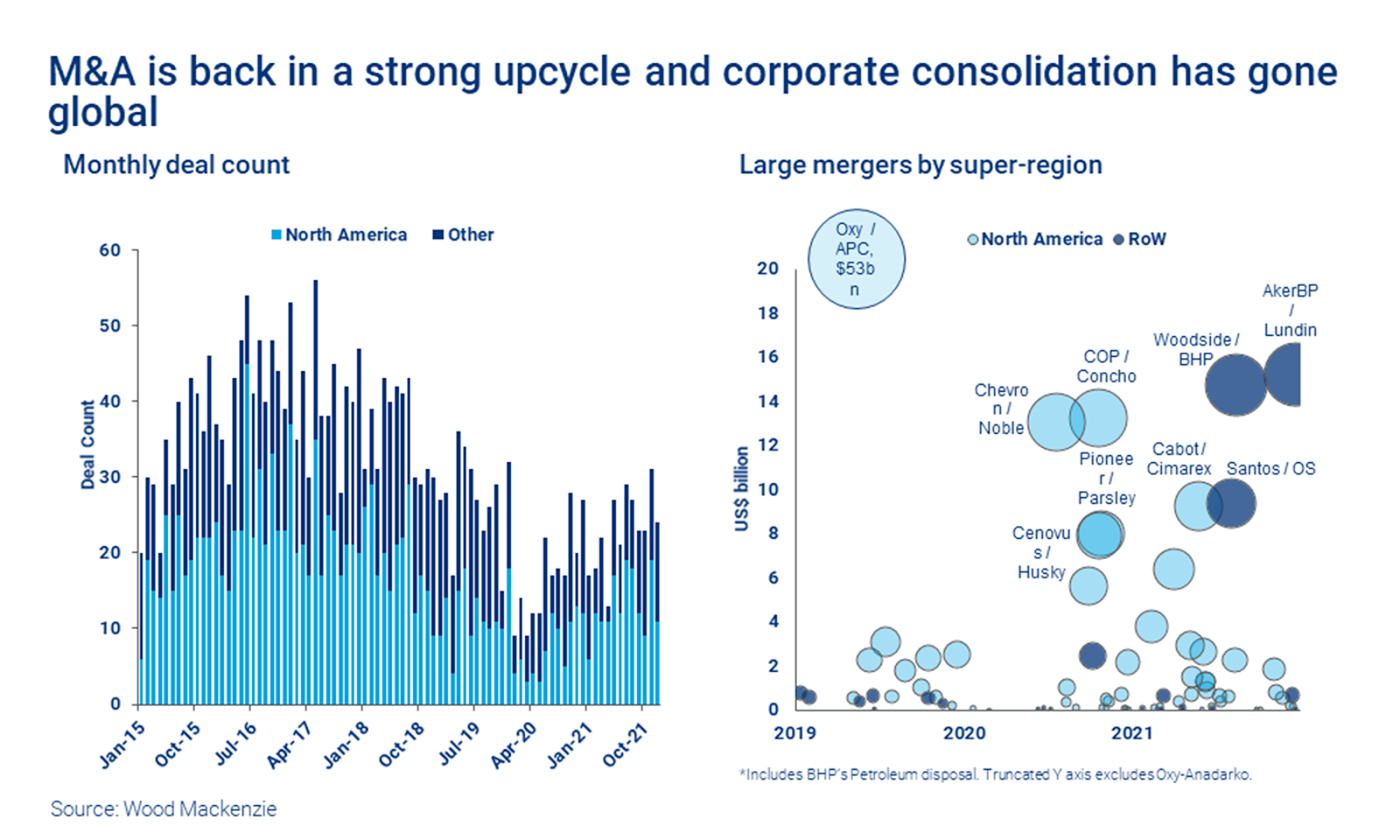

Why? Thanks to growing pressure on O&G companies – both to return capital to shareholders and deal with environmental issues / energy transition – the entire industry has shifted.

Not only were O&G companies forced to make operational and productivity improvements…

Similar to what we’ve seen in the gold mining industry, O&G companies started to grow through mergers and acquisitions to achieve economies of scale, increase reserve depth, and gain/maintain market relevance.

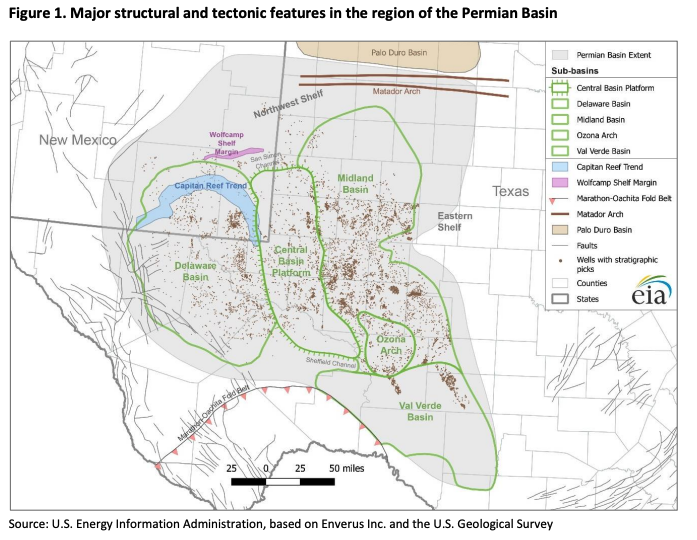

This is especially the case in the Permian Basin (i.e., West Texas and New Mexico).

Map showing the boundaries of the Permian Basin region and principal sub-basins. Source: EIA

Drillers have been warning for a while that untapped acreage is running out, so acquisitions have essentially become the only option for producers that want to grow in the area—and many big players do want to grow in the area.

Earlier this year, the Energy Information Administration predicted that oil output in the Permian was declining for several months in a row.

For each of these months the EIA had to revise its figures after getting actual production data that showed output in the Permian was actually increasing.

There is still plenty of oil in the Permian that can be extracted relatively cheaply. That is why everyone with money to spend is rushing there to buy smaller rivals and expand.

And that is why some believe that by 2030, the U.S. oil industry could be a very different place than it is now.

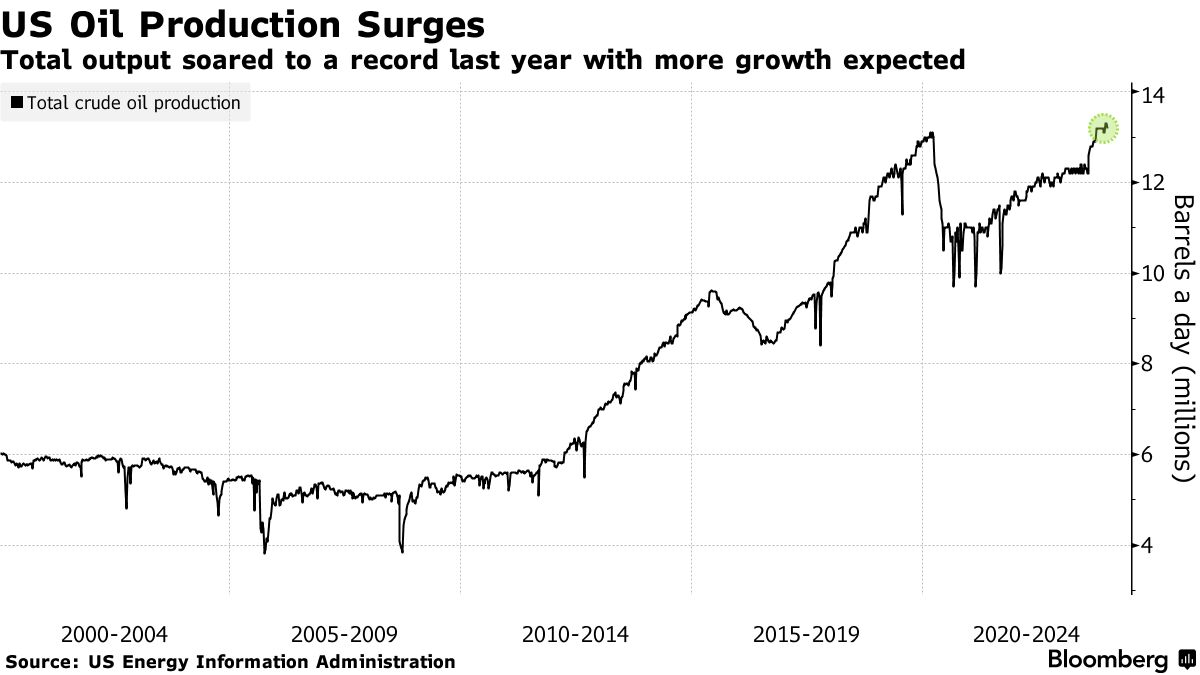

However, despite President Biden’s climate agenda – which includes the bipartisan 2021 Infrastructure Law, and 2022 Inflation Reduction Act – American Oil has been pumping a record ~13 million barrels per day of crude…

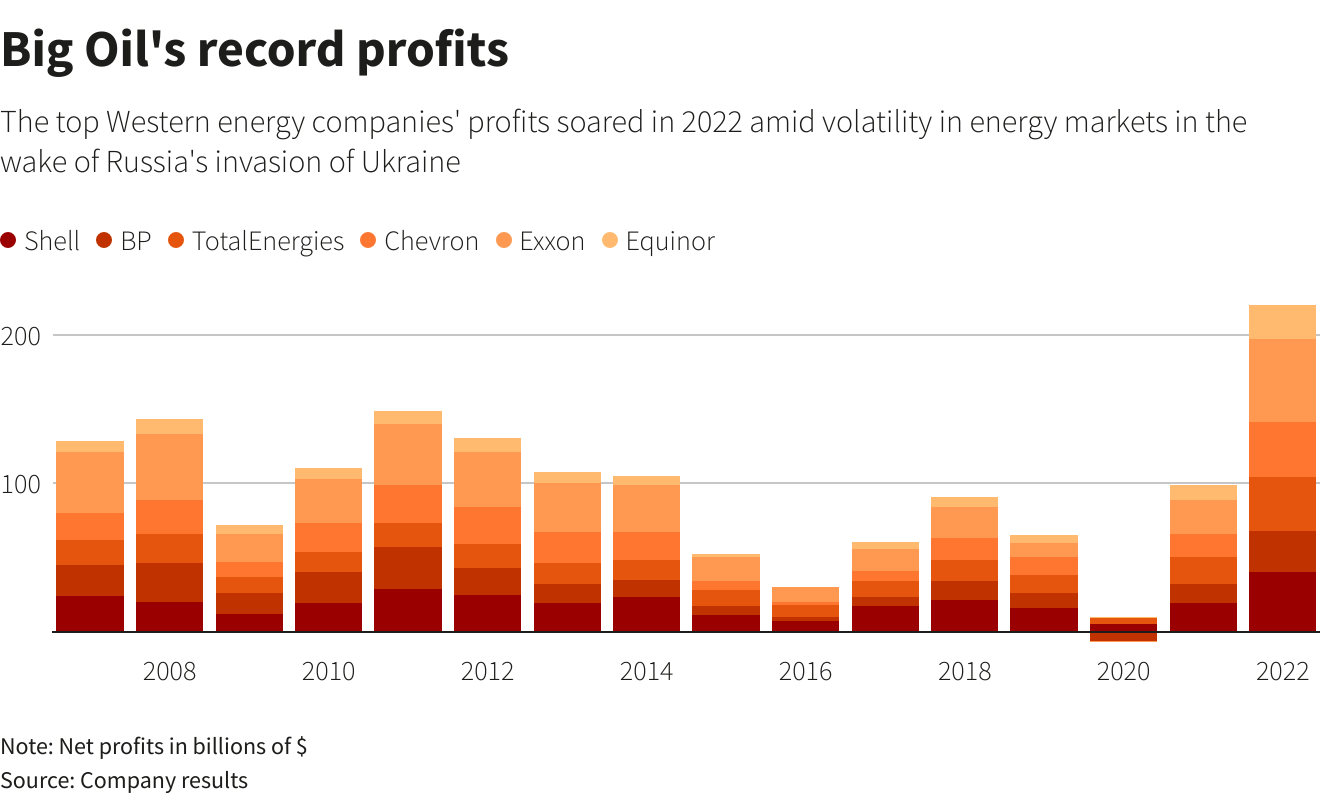

Produced record cash flows in 2021 - 2022…

Source: Reuters

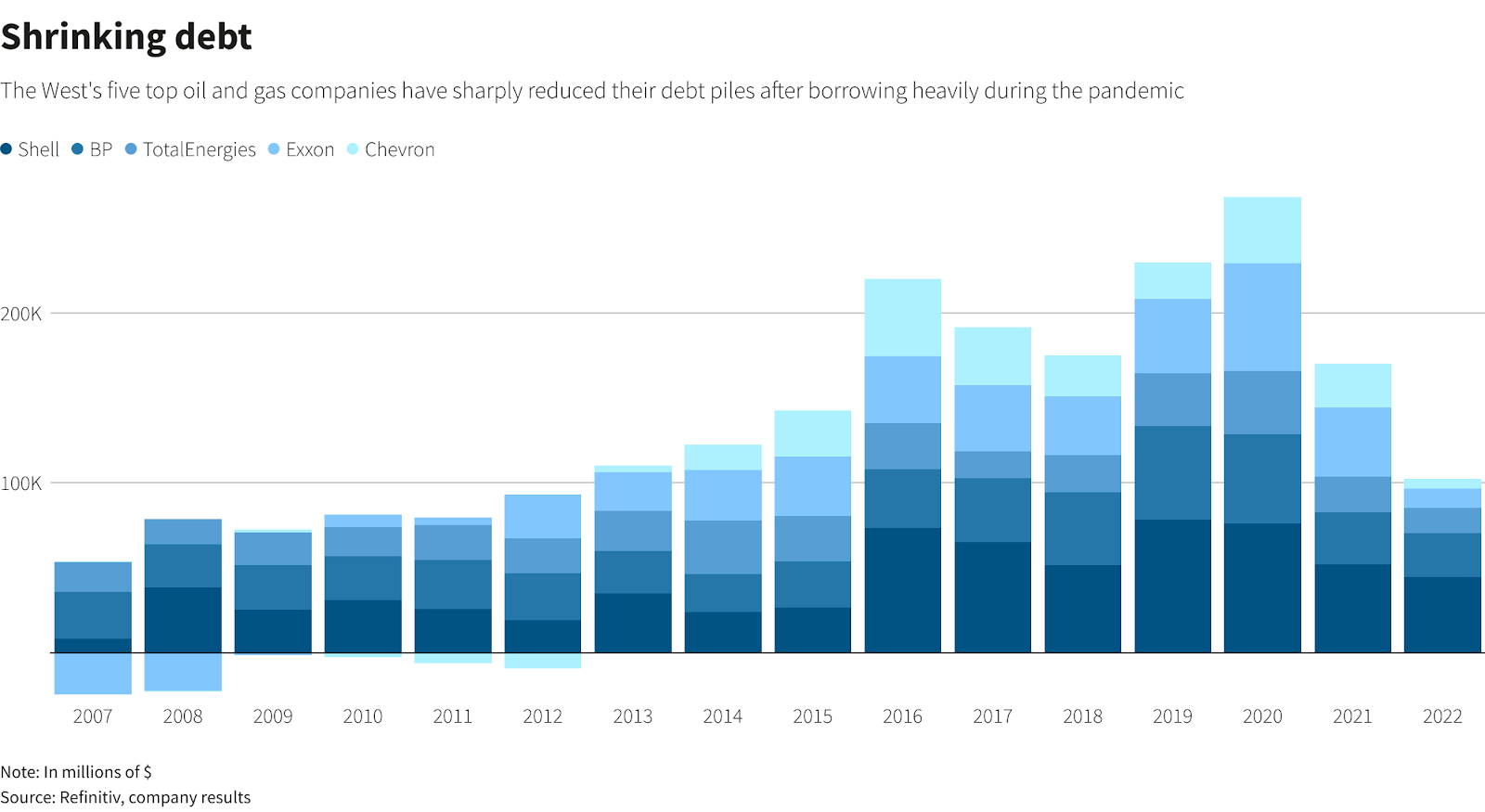

Significantly reduced debt…

Source: Reuters

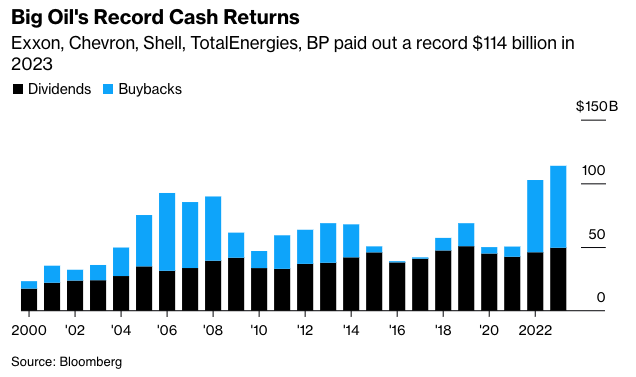

Not to mention, massive dividends and share buybacks for investors.

And if KKR’s forecast of ~$80 - $100 per barrel in 2024 comes true, that will likely only continue to drive profitability for oil majors.

All of which puts Biden (and the Democrats) in a weird position – The United States is producing more oil than any country ever has.

The flow of huge amounts of crude from American producers is playing a big role in keeping prices down at the pump, diminishing the geopolitical power of OPEC and taming inflation.

The average price of a gallon of regular gasoline nationwide has dropped to close to $3, and analysts project it could stay that way leading up to the presidential election, potentially assuaging the economic anxieties of swing-state voters who will be crucial to Biden’s hopes of a second term.

But it is not something the president publicly boasts about. The politics of oil are particularly tricky for Democrats, whose chances for victory in the 2024 elections could hinge on whether young, climate-conscious voters come out in big numbers.

Many of those voters want to hear that Biden is doing everything in his power to keep oil in the ground.

“They invested too little of that profit to increase domestic production and keep gas prices down,” Biden said during his State of the Union address in February. “Instead, they used those record profits to buy back their own stock, rewarding their CEOs and shareholders.”

The soaring domestic oil output has already begun to reshape geopolitical dynamics.

The United States is producing so much oil that it has undermined the influence of OPEC, which failed when it tried to make production cuts recently to drive prices up globally.

Even crazier? Permian oil production is projected to hit new all-time highs in 2024 – 6.4 million barrels per day (MMbpd) at the end of this year, up from 6.1 MMbpd at the end of 2023.

And that brings us to the LNG part of this story…

On Jan. 26, 2024, the Biden Administration announced a “temporary pause on pending decisions on exports of Liquefied Natural Gas (LNG) to non-[Free Trade Agreement] countries until the Department of Energy can update the underlying analyses for authorizations.”

While this technically isn’t a “ban” on exports – but a pause on new applications – this ticked off a lot of people.

Source: WSJ

Source: Fortune

Source: Bloomberg

While I won’t speculate as to why the Biden administration is engaging in this strange course of action…

It seems the most likely outcome of this will be higher gas prices domestically.

Bill Ackman Enters Retail Market

Bill Ackman, CEO of Pershing Square Capital Management, is set to launch a new retail-investor focused hedge fund – Pershing Square USA (Ticker: PSUS) – on the New York Stock Exchange.

Why? According to the regulatory filing,

Investors in many alternative investment funds own non-traded interests with limited redemption and liquidity features, whereas, the Fund intends to be a publicly-traded, NYSE-listed, closed-end fund.

The Fund expects that it will have significant liquidity supported by its scale, name recognition and the Adviser’s broad following.

The Adviser believes that the Fund has the potential to be one of the largest, if not the largest, listed closed-end fund and expects that the Adviser’s brand-name profile and broad retail following will drive substantial investor interest and liquidity in the secondary market.

Or said another way, Ackman’s betting his 1.2m followers on X (formerly Twitter) will drive fundraising efforts.

But more to the point, Ackman’s fund addresses one of the long standing issues we see with these new retail-focused funds – fees.

Also according to the filing,

No performance fees. Unlike conventional alternative investment funds, which typically charge 15%-30% annual performance fees on realized and unrealized profits in addition to management fees, the Fund will not be subject to any performance fees.

The Fund believes that this has the potential to meaningfully improve long-term NAV per Common Share performance.

No management feefor first 12 months. The Adviser has irrevocably waived the Management Fee for the first 12 months of the Fund’s operations.

This means Ackman is offering a hedge-fund structure, for retail investors, with no minimum investment, and a flat two percent management fee per year (after the first 12 months).

While this alone doesn’t make it a “good investment” by any stretch, this could be a watershed moment for the industry, in terms of expanding retail access to alternative investment strategies.

Speaking of structure, the fund mirrors a $14 billion fund already listed on European stock exchanges, called Pershing Square Holdings, which returned 27% in 2023.

However, there is absolutely no guarantee that this fund will see similar returns. Additionally, Equifund has no affiliation with Pershing Square, and the discussion of this fund is solely for educational purposes.

The “Wall Street vs SEC” Saga Continues with Expansion of “Dealer” Definition

In case you didn’t think the Gensler-led SEC could do anything else to make basically everyone mad at them…

At a contentious open meeting on February 6, 2024, the SEC voted three to two to adopt rule amendments under the Securities Exchange Act of 1934 that will significantly expand the scope of the definition of “dealer” and “government securities dealer.”

As a result of the expanded definitions, market participants that regularly engage in certain liquidity-providing activity in securities (or government securities), will have to register with the SEC as a “dealer” or “government securities dealer” under Section 15 or Section 15C, respectively.

Why should you care?

While it might not immediately be obvious how this impacts retail investors…

Eventually, all costs get passed on in one form or another.

But before we pass judgment – is this “good” or “bad” – let’s take a look at the arguments being presented.

The Securities and Exchange Commission will now require dozens of firms, including high-speed traders and hedge funds, to face new Net Capital requirements, register their activities and report more information on their transactions.

The SEC has been trying to bring its regulations up to speed with markets, especially for U.S. Treasurys, which are increasingly dominated by electronic trading and intermediaries that act as crucial providers of liquidity.

Unregistered market participants acting like dealers accounted for about half of daily Treasury trading activity over electronic platforms in recent years, according to research cited by the SEC.

Big trading and hedge-fund firms warned the SEC that imposing higher costs on their operations could lead them to scale back, reducing overall liquidity.

They also argued the SEC’s timing risked upsetting the market just as the Treasury is trying to finance larger budget deficits.

If you missed our deep dive on Basel III, be sure to check that out for why the “capital requirements” is a big deal.

On one hand, it might be a good thing to have greater regulations for high frequency trading firms…

But the broadening of the definition of a dealer – which expands the purview of WHO falls under these regulations – is problematic.

The Commission’s effort to classify nearly any person who buys and sells securities as a “dealer” under the Securities Exchange Act of 1934 (the Exchange Act) extends beyond its statutory authority.

The lack of any limiting principle creates the potential for arbitrary and capricious government action.

Today’s action codifies the Commission’s view that the “dealer” definition is practically limitless. The public should be concerned about the immense scope of this claimed jurisdiction.

The rule of law means that the government should define ex ante which activities are lawful and which are not.

Without such definition, governmental authority can be arbitrary and even tyrannical. Government can favor some entities, while disfavoring others.

This rulemaking targets proprietary trading funds (PTFs), private funds, and others who make money by buying low and selling high in the Treasury market, while creating additional regulatory confusion for other markets, including crypto asset securities.

Indeed, following Form PF, the adoption of private fund adviser rules, securities lending disclosure, and short position and short activity reporting, this action feels like another salvo in the Commission’s war on private funds.

While it might be easy to say Wall Street is crying crocodile tears about enhanced regulation…

This expanded definition may have serious consequences for crypto asset securities.

According to the recent Coindesk article, U.S. SEC Clears 'Dealer' Rule Expansion That Could Rope in DeFi:

The commission did consider a crypto carve-out, according to the document, but decided that would have "negative competitive effects" by giving crypto firms an advantage over those who have to register.

While this effort – which goes into full effect in April of next year – was largely targeted at electronic participants in the U.S. Treasuries market, the requirements will be the same for any business roped into the expanded definition.

A dealer must register with the SEC, comply with securities laws and join an industry-backed self-regulatory organization.

But as we’ve seen time and time again, the final ruling published by the SEC often contains “softer language” than what was originally proposed.

The Commission originally proposed the amendments on March 28, 2022.

The Final Rules did not include two of the most contentious provisions applicable to the “as part of a regular business” test: a qualitative standard designed to capture firms that trade flat each day, and a bright-line quantitative test designed to capture firms that trade large volumes in government securities.

The Final Rules also removed from the “own account” definition the aggregation standard, which expanded the definition of “own account” to include accounts “held in the name of a person over whom that person exercises control or with whom that person is under common control.”

The Final Rules may bring within the definition of dealer a number of proprietary trading firms, private funds, and investment advisers (including registered investment advisers).

Additionally, the Final Rules reflect a change in language from “routinely” to “regularly” as applied to a person’s expression of trading interests.

It’s still anyone's guess exactly who is going to be ensnared by this new regulation – or how this regulation will be used in the future – but it’s something we’ve got our eyes on.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |