- Private Capital Insider

- Posts

- 📈 Taking “Smart Investment Risks” with Asymmetric Bets

📈 Taking “Smart Investment Risks” with Asymmetric Bets

The Insider’s Guide to Managing Risk with Price, Position Size, and Follow On Rounds

Jake @ Equifund

May 10, 2024

For investors looking to take limited downside risk with potentially unlimited upside return…

Chances are, you’ve heard about the holy grail of investing – asymmetric bets.

Philosophically speaking, it’s pretty obvious why you’d want to invest ONLY in opportunities where the potential reward is greater than the potential risk…

But what’s not obvious is how to determine what the actual risk and reward potential is, or the statistical probability of either outcome happening.

And even less obvious… how do you think about pricing in the risk and uncertainty of any trade you’re about to make – especially as a small balance check writer who has to be mindful about position sizing?

Here’s a potential counter intuitive answer: It’s managing your risk through concentrating your positions over time (i.e. cutting your losers early and doubling down on winners) instead of diversifying (i.e. selling your winners to rebalance into losers).

And when it comes to investing in early stage companies, this means keeping capital in reserves to invest in follow on rounds.

That’s the topic of today’s issue of Private Capital Insider.

-Jake Hoffberg

P.S. Interested in investing in an early stage, AI-powered oil and gas play? If so, Pytheas Energy is raising capital on the Equifund Crowd Funding Portal.

Risk Stacks: A brief primer on understanding risk (and how that impacts price)

Last week, we talked about the types of private market deals I like to invest in as a small checkwriter.

And just in case you don’t have time to read the entire article, here’s the gist of it…

If your entry price determines 80% of your long term stock returns, proper underwriting (i.e. pricing in risk) and position sizing are the key risk management tools.

But as we’ve discussed in previous issues, most people don’t really understand what risk actually is…

Or for that matter, how to think about managing that risk through a function of both price and check size.

That’s why the concepts of Alpha, Beta, and Theta are crucial in this context, each serving a distinct role in the assessment and pricing of risk.

Alpha (𝛼) represents the excess return on an investment relative to the return of a benchmark index (for example, the S&P 500)... when adjusted for risk.

Alpha is often seen as a reflection of the unique value added or subtracted by the management of a portfolio.Beta (𝛽) measures the volatility of an investment compared the benchmark index.

A Beta greater than 1 indicates that the investment is more volatile than the benchmark, while a beta less than 1 indicates that the investment is less volatile.Theta (Θ) represents the rate of decline in the value of an option due to the passage of time, assuming all other variables remain constant. This is often referred to as the "time decay" of options.

Theta is particularly important in the pricing of options because it affects the premium of the options as they approach their expiration date (we are going to come back to this concept in just a moment)

While we are often inundated with the promise of alluring potential rewards that come with the high risk involved in early stage investing…

Very rarely do I hear management teams candidly address the multiple risks involved with any investment in the category they are in…

Nor do I hear an explanation about how those risks are being priced into the current financing.

For these reasons, when we are going through underwriting, one of my big questions is some version of…

How does management generate Alpha through managing the known risks and dealing with unknown uncertainty?

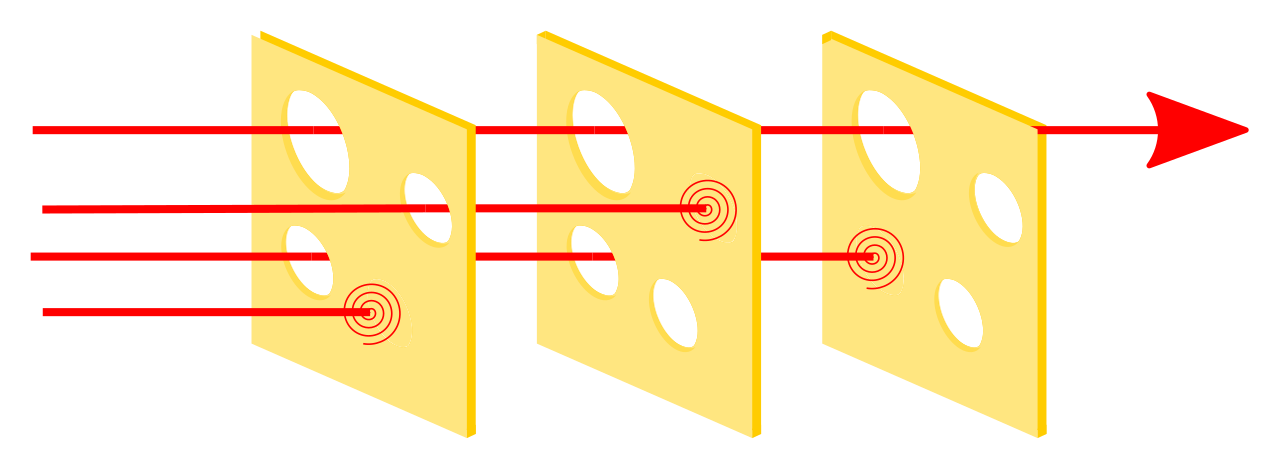

For this, we have to take a look at what we call the “Risk Stack” – the accumulation or layering of multiple risks that, when combined, significantly increase the likelihood of a negative outcome or failure.

In risk management disciplines, this is sometimes referred to as the Swiss Cheese Model of Accident Causation – although many layers of defense lie between hazards and accidents, there are flaws in each layer that, if aligned, can allow the accident to occur.

In this diagram, three hazard vectors are stopped by the defenses, but one passes through where the "holes" are lined up. Source: Wikipedia

And to use our Game of Business vs Game of Money framework, we have to assess both the business risk and financial risk within the investment opportunity.

Generally speaking, here are the main Game of Business risk flashpoints with respect to the typical early stage company:

Technology Risk: Does the technology work as claimed?

Patent Risk: Does the team have the ability to acquire and defend patents in an effort to drive enterprise value?

Regulatory Risk: Does the company need to achieve some sort of regulatory approval (or permitting) to execute the business plan?

Commercial Risk: Is there sufficient demand in the marketplace to successfully commercialize the technology?

Supply Chain Risk: Will management be able to maintain profit margins and product quality as it scales supply to meet demand?

In my experience, the vast majority of investors are very focused on the Game of Business risk factors; whenever I’m in a room where investors are asking management teams questions, it’s almost always product (or operations) focused.

This makes sense when you think about it…

Most individual investors are far more likely to have some sort of operational (or product) experience than they are a corporate finance or capital markets background.

But remember: Good products don’t necessarily make good companies, and good companies don't necessarily make good investments.

However, there are plenty of situations where investors can make above market returns betting on “okay” companies with “okay” products.

For these reasons, instead of getting overly caught up in the details of “is this product better than what’s already out there” or “is the market as big as they’ve forecasted?”...

I find it’s far more useful to ask the question “so how do I make money in this deal?”

Why? Because in the majority of early stage investments, there are only two things that determine your financial returns: Your entry price and your exit price.

Simply put, you are looking to make short- to medium-term trade… not a medium- to long-term investment.

And even though the Game of Business Risk Stack is something we need to pay attention to when it comes to execution risk…

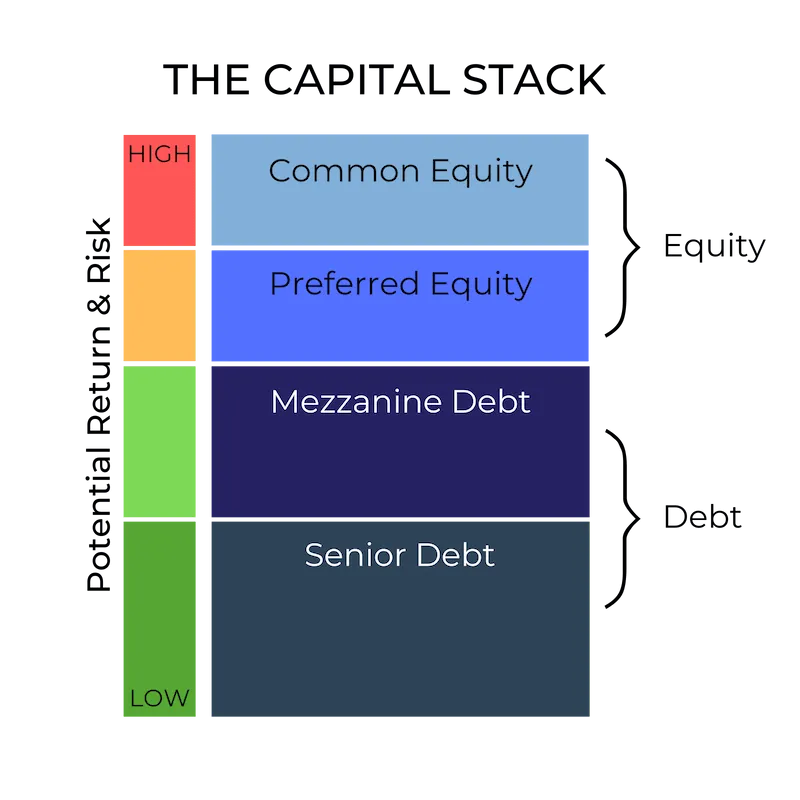

The Game of Money has its own risk stack called the Capital Stack – which organizes the different types of financing into a hierarchy based on the order of repayment priority and financial risk.

Senior Debt: This is the most secure form of investment in the capital stack. It has the highest priority in terms of repayment and generally carries the lowest risk.

Senior debt holders are usually the first to be repaid in the event of a sale, refinancing, or liquidation of the property.

Mezzanine Debt: Positioned between senior debt and equity, mezzanine debt is subordinated to senior debt. It is riskier than senior debt and therefore typically offers higher returns.

Mezzanine lenders may also receive warrants or options to convert debt into equity, increasing potential returns if the project performs well.Preferred Equity: This component of the capital stack offers features of both debt and equity.

Preferred equity holders have a priority over common equity holders in terms of profit distribution and capital return, but they are subordinate to all debt holders.Common Equity: At the top of the capital stack, common equity holders assume the highest level of risk. They are the last to be paid in any capital distribution scenario, such as from operational cash flows or upon liquidation of assets.

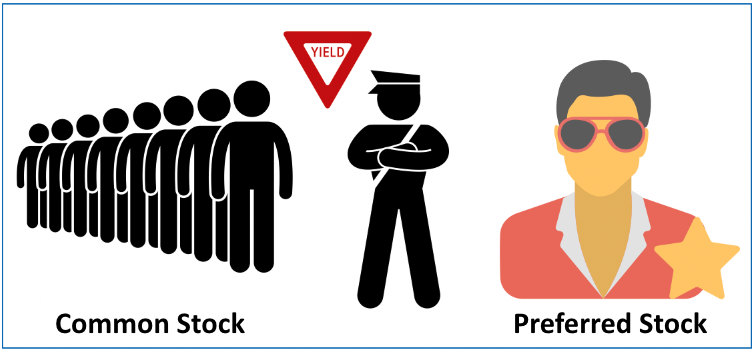

Said another way, your biggest risk as an early stage investor – especially if you own common stock – is every other round of capital that comes in.

More specifically, how the rights and privileges those shareholders receive – relative to yours – impact your ability to sell your shares at a future date.

Because they take on significant risks, investors expect to get “VIP” head-of-line privileges to be paid upon a liquidation event such as an acquisition. Common stockholders wait in line and collect proceeds only after all of the preferred investors take their share. Source: Fundable Startups

And once we have a composite understanding of the Risk Stack and Capital Stack – as well as how management can “de-risk” the investment opportunity over time by achieving certain milestones…

Then, and only then, can we have a real discussion around how to properly price the risk vs reward potential…

And how much we’re willing to wager on this current investment opportunity.

With a mature company with an observable track record of results, it’s relatively easy to produce a reasonable forecast of future returns – the next 12 months probably looks pretty similar to the previous 12 months (with some growth factored in).

But what about young companies with a limited track record and incredible – albeit speculative – future potential value?

Valuing early stage companies with milestone driven valuations and multi-stage call option pricing

Before we begin, we have to remember that valuation is not the same thing as price.

Valuation is an attempt to quantify the true intrinsic value of an asset using objective measures and predictions of future performance.

Price is what the market will bear, influenced by psychological factors (i.e., risk and reward), market dynamics (i.e, supply and demand), and external economic conditions (i.e., liquidity)

In “normal” finance, the method for valuing a company (or asset) is most commonly determined by a discounted cash flow model.

Basically, you have a spreadsheet that provides both a backwards looking track record of actual financial results, and a forward looking pro forma that projects expected future results.

Then, you discount the value of all future cash flows to today in order to account for the risk and uncertainty of that forecast being proven.

If you’ve ever heard of a company being valued as a multiple of any metrics – whether it’s revenue, EBITDA, or net operating income – you’ll notice the larger the number being multiplied is, the larger the multiple is.

This makes sense when you think about it: the more mature the company is – or the faster it’s growing – the more likely it is that the forecasted results are going to come true.

So what factors – aside from pure supply and demand for the company’s equity – would potentially justify a higher multiple (i.e. higher price) for the same present value?

Why is one business that is in roughly the same starting position as another business sometimes worth 2x, 5x, even 10x more?

Short answer: the expected risk vs reward of the investment

Said another way, risk taking investors who understand they are looking for asymmetric bets are willing to pay a higher price for better odds.

So what types of factors might influence the price investors are willing to pay for any asset?

Product: Highly engineered product(s), especially critical infrastructure or lifesaving devices

Market: A large total addressable market, or the ability to expand into adjacent ones

Revenue: Recurring customer base without significant customer concentration

Margins: High margin and differentiation from competitors

Team: Strong leadership team with a track record of success in the asset class

Growth: The ability to rapidly scale and achieve aggressive growth targets

But how do you value a company that has limited (or no) revenue? Especially companies where there is a significant “risk flashpoint” they have to overcome before they can generate revenue?

To answer this question, we have to think about an investment opportunity as a transfer of risk from the seller to the buyer.

Here’s why…

In the Game of Business, figuring out the price of something is relatively straight forward.

You have a price for how much something costs to make, how much competing products are selling for, and some amount of profit margin you’re solving for.

For the customer, the risk reversal mechanism often comes in the form of a “make good” or a “refund” from the selling party if the product or service doesn’t perform as advertised.

But in the Game of Money, we’re not buying and selling tangible goods and services. We are buying and selling financial products called securities.

And with the exception of annuities and US treasuries, no security can be considered a “risk free” asset.

This means by definition, in the Game of Money, the buyer is actually purchasing risk from the sell side…

And the buy side expects to be appropriately compensated for the risk they are being asked to take.

So how does the price of the risk get determined?

Generally speaking, this is the value the Banker (aka “Sponsor” or “Lead Investor”) brings to the deal – they are responsible for underwriting the risk, setting the price, and making a market to transfer the risk (and potential future value) from the sell side (the Issuer) to the buy side (the Investor).

For example, when an Issuer raises debt capital by selling bonds, in exchange for money, the company promises to repay the principal at a later date (plus interest).

The risk transferred here includes the credit risk that the issuer might default on its payments.

However, if the Issuer doesn’t have any cash flow – and therefore have no way of repaying debt – this means their only real option is to raise equity capital by selling stock.

When Investors purchase stock, they essentially accept the risk associated with the company's future performance (i.e. execution risk).

In return, they gain potential for high returns through appreciation of their equity value if the company succeeds.

But again, when investing in an early stage company – which should be considered high risk and speculative in nature – how do we think about pricing the risk we’re being asked to take?

For this reason, many professional early stage investors view the price they are willing to pay today based on a “multi stage call option pricing” rationale.

This perspective is based on the idea that investing in a startup involves committing capital in stages, contingent upon the venture meeting certain developmental milestones.

And if we are looking to take smarter investment risks through asymmetric bets…

One of the simplest ways we can manage risk is through proper position sizing and follow on rounds.

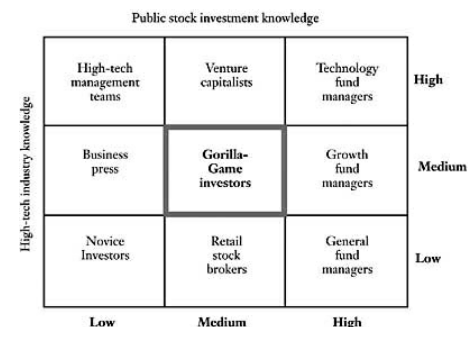

To understand why, here’s a quote from one of my all time favorite books on investing in high tech startups as a small balance investor, The Gorilla Game: Picking Winners in High Technology, by Geoffrey Moore (published in 1998)…

As a gorilla-game investor, we think you have or can readily acquire “medium” knowledge both of the high-tech industry and of investment principles.

That is, on the industry knowledge side, we think you have or can gain a knowledge of the industry that is better than your retail stock broker’s but not as good as, say, a venture capitalist’s.

Finally, and perhaps most importantly, the you, that we have uppermost in our minds, is a private investor who is turning to the stock market to provide for your family’s future.

Far from being independently wealthy, we assume you to have modest capital at the outset and to be deeply concerned about not losing it.

As a result, we are going to define an investment strategy that has significant upside potential but that is, at its heart, inherently conservative.

That is to our mind the real purpose of the gorilla game—to help private investors participate in the rewards of high-tech stock gains while standing clear of the market’s unnerving volatility.

So what is the gorilla game? It is a form of growth investing.

Like growth investors, gorilla gamers value the forward-looking dynamics of a company’s market as a better indicator of its future stock performance than its current price/earnings ratio.

Two key points distinguish the gorilla game from growth investing in general:

1: It focuses exclusively on high tech, and specifically on product-oriented companies that sell into mass markets undergoing hypergrowth.

2: It uses consolidation, not diversification, as its primary risk-reduction strategy for long-term holds.

Simply put, if we assume that any early stage company is going to raise multiple rounds of private capital before a liquidity event…

We will have multiple chances to invest – usually at higher prices – as the company matures and “de risks.”

If we assume this to be true, we should consider placing more – but smaller – bets across multiple companies (i.e. buying a basket of stocks)…

Then, as it becomes more clear which ones will be winners and losers, we cut the losers short and add more to the potential winners.

Final Thoughts: The Easiest Alpha is Price

For many reasons, the simplest way to achieve a consensus around price is to identify the significant “risk flashpoints” in the corporate lifecycle…

And then assigning a “value” to the company for successfully moving through these milestones – ideally on (or ahead) of forecast, and on (or under) budget.

In essence, we are looking for signals that indicate the believability of Management’s forecast – and ideally, some sort of track record where Management has demonstrated their ability to make and meet forecasts in the past.

In other words, we’re looking for Alpha.

With this idea in mind, Equifund strives to be a source of Alpha for our members by underwriting (and pricing) risk.

According to Eric Falkstein’s book “Finding Alpha: The Search for Alpha When Risk and Return Break Down”:

While some alpha seeking is based on understanding portfolio theory, most of it is not.

Alpha is basically self-derived private information about straightforward but detailed situations, which implies that people have a good reason to present it strategically.

The theory that risk underlies any returns not due to chance is fundamental to modern finance, and because it is also wrong presents both current confusion and considerable opportunities to those seeking alpha.

A good risky investment is tied to one's human capital, meaning it is highly idiosyncratic, not so much dependent on covariances with the business cycle as with one's talents.

No matter what your position, it helps to understand how the archetypal alpha is created, because a manager who knows the source of his organization's alpha is much more effective than one who merely knows everyone's name.

Entrepreneurs, inventors, alpha seekers and others like them are trying to create value by doing something differently from how others would do it.

The goal in the search for alpha is to find what you are good at, become better at it, and do it a lot.

Thus, it is more of a self-discovery process in a quest to find an edge that can become a vocation or firm value, rather than a specific trading strategy.

This idea of figuring out what we’re good at, in order to find our source of Alpha, has been a key tenet at Equifund.

And as much as we’d like to say we are genius stock pickers who can predict what companies will be massive winners…

We know that, statistically speaking, the easiest way to deliver better investment returns is to simply reduce fee drag and negotiate an appropriate risk-adjusted price.

And when you’re a small balance check writer with non-controlling shares in a privately held company…

In many ways, this is the single easiest way to target better investment returns as a completely passive investor.

Looking for an AI-powered oil and gas play?

If so, you might be interested in checking out Pytheas Energy – an upstream oil and gas producer that is currently raising capital on the Equifund Crowdfunding Platform.

[Disclaimer: By law, Equifund cannot make any buy/sell recommendations, provide individualized investment advice, or otherwise “endorse” any specific investment opportunity – especially ones listed on the Equifund Crowdfunding Platform due to the obvious conflicts of interest. Please do not make any investment decisions based solely on the information published in this article.]

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |