- Private Capital Insider

- Posts

- 📈 The rent is too damn high

📈 The rent is too damn high

An Insider's Guide to Investing in Affordable Housing

Jake @ Equifund

February 29, 2024

If you’re tired of the “commercial real estate apocalypse” narrative building momentum in the financial media these days…

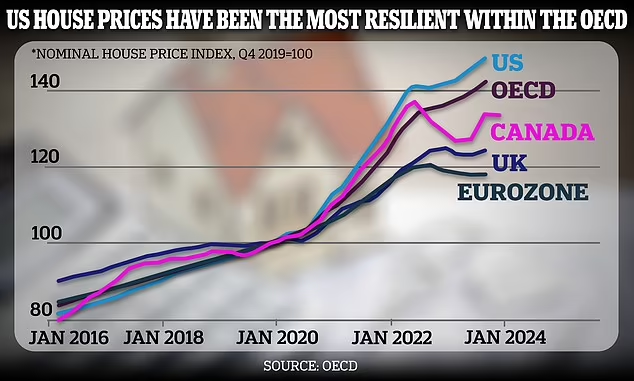

Home prices continue to climb – faster than any other industrialized nation – as rates stay higher for longer and inflation continues.

Source: Daily Mail

The persistence of housing inflation poses a problem for Fed officials as they consider when to roll back interest rates.

Housing prices and mortgage rates don’t directly show up in inflation data, however. That’s because buying a home is an investment, not just a consumer purchase like groceries.

Instead, inflation data is based on rents.

And with private data showing rents moderating, economists have been looking for the slowdown to appear in the government’s data, as well.

Federal Reserve officials largely dismissed housing inflation for much of last year, believing that the official data had simply been slow to pick up on the cooling trend apparent in the private data.

Instead, they focused on measures that exclude shelter, an approach they saw as better reflecting the underlying trends.

But as the divergence has persisted, some economists inside and outside the Fed have begun to question those assumptions.

Economists at Goldman Sachs recently raised their forecast for housing inflation this year, citing rising rents for single-family homes.

As the American political activist, Vietnam War veteran, and NYC political candidate, James McMillian III, once said – ”The rent is too damn high.”

That’s why today, we’re going to dig into one of the most important issues facing our economy today – affordable housing.

Let’s dive in,

-Jake Hoffberg

P.S. Considering an investment in affordable housing?

Be sure to check out FG Communities offering on the Equifund Crowdfunding Portal to learn more.

FG Communities recently announced the company plans to end its Reg-CF offering early.

The last day to invest will be Monday, March 4, 2024.

P.P.S Looking for back issues of Private Capital Insider?

The “Highest and Best Use” Paradox:

Why Upcycling, Zoning Laws, and Construction Costs Ruin Affordable Housing Efforts

On the surface, the solution to the U.S. housing crisis may seem obvious – just build more affordable housing. However, this solution isn’t as practical as it may seem.

Here’s why…

The United States is not experiencing a shortage of available housing stock; there’s plenty of inventory around the country.

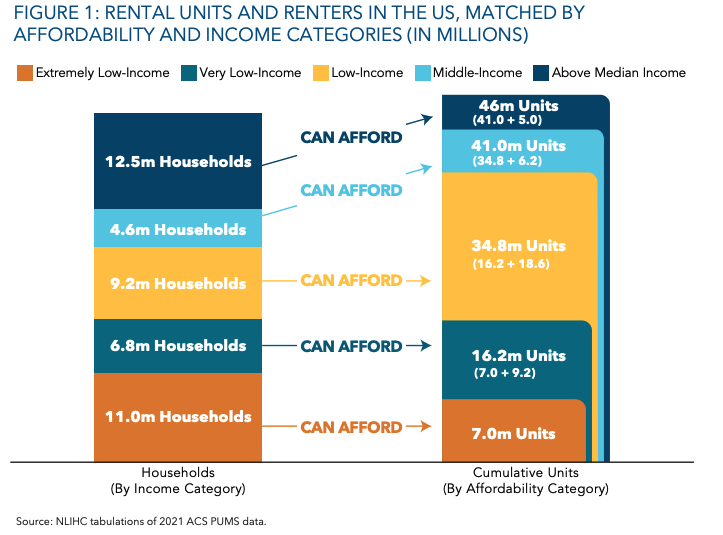

There are 44.1 million renter households and 46.0 million rental units with complete kitchen and plumbing. For every 100 extremely low-income renter households, there are only 33 affordable and available rental homes; Source: NLIHC

The real problem is the economics of affordable housing in desirable places to live. There’s simply no economic way to “build” affordable housing when the cost to build and operate new homes exceeds what low-income renters can afford.

Nationally, the average monthly operating cost for a rental unit in 2018 was $439, excluding mortgage and other debt-related expenses.

In other words, even if landlords set rents at the bare minimum needed to cover costs – earning no profits – housing would remain unaffordable to most very-low-income households, if without government subsidies.

The problem has only gotten worse thanks to burdensome regulations and approval processes in some communities and, in recent years, growing material, labor, and land costs.

And without substantial government subsidies, like the Section 8 Housing Choice Vouchers – which simply shift the cost burden to the taxpayer instead of solving the affordability problem – homebuilders and landlords face a dilemma…

Do you build low-income housing – at either breakeven or at a loss – and hope for government subsidies to make up the difference?

Or do you focus on building housing for the more affluent households?

Not surprisingly, the new rental housing is largely targeted at the higher-priced part of the market.

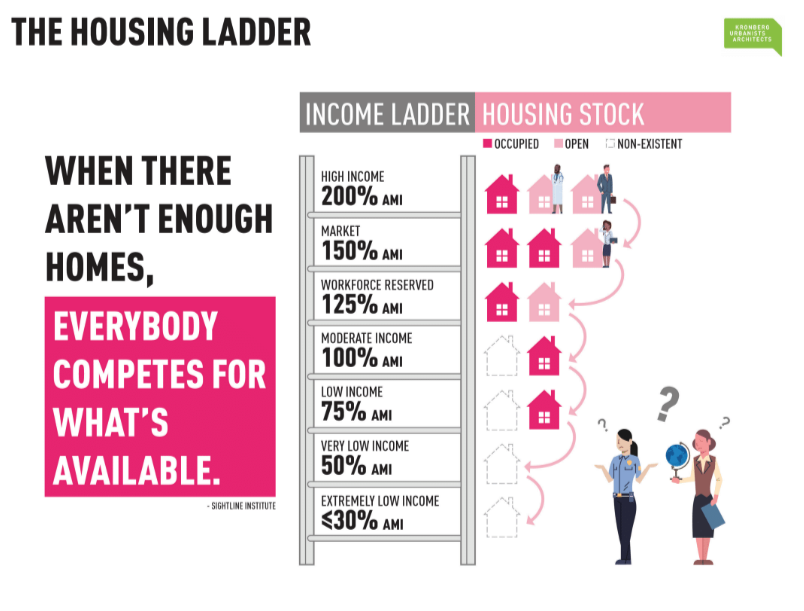

As more housing is built towards the higher end, it creates an unwinnable game of “musical chairs,” as everyone is forced to compete for what's available, even if they can’t afford it.

The Area Median Income (AMI) is the midpoint of a region’s income distribution, by household size, as determined by the Department of Housing and Urban Development (HUD) – Source: KRONBERG URBANISTS + ARCHITECTS

This forces low-income renters to hope that older housing stock “trickles down” as it ages, and higher-income renters move into newer properties.

However, in reality, what happens is something called “Upcycling” (or “gentrification”).

In stronger markets, owners have the incentive to redevelop their properties to justify asking for higher rents from higher-income households.

In weaker markets, owners have the incentive to abandon their rental properties – or convert them to other uses when rental income is too low – to cover basic operating costs and maintenance.

In aggregate, this means that properties that were once affordable become unaffordable for one simple reason: properties tend to get upcycled in the pursuit of the “highest and best use” (HBU).

How is HBU determined? Through four criteria:

What is physically possible? This is a matter of the available space and limits of architectural design

What is legally permissible? This is a matter of zoning issues or other restrictions

What is financially feasible? This is a matter of available financing to improve or rebuild the physical structure

What is maximally productive? This is a matter of how the property is structured to produce the best net operating income

Overwhelmingly, the HBU defaults to single-family homes. Today, restrictive single-family zoning practices make it illegal to build anything other than a detached single-family home on nearly 75% of all residential land in America.

As this “Upcycle” process continues – and new inventory is built for wealthier tenants willing to pay higher rents – what we inevitably see is the hollowing out of the more affordable housing stock, referred to today as the “Missing Middle Housing.”

“Missing Middle” building types, such as duplexes, fourplexes, cottage courts, and courtyard buildings, provide diverse housing options and support locally-serving retail and public transportation options. Source: Missing Middle Housing, KRONBERG URBANISTS + ARCHITECTS

The term, coined by Dan Parolek of Opticos Design, refers to certain building types – such as small apartment buildings, multi-unit houses, and simple mixed-use structures with a storefront and a residence – that were the building blocks of those blossoming 19th-century metropolises, but which are scarcely produced anymore.

They are called “Missing” because they typically have been illegal to build since the mid-1940s, and “Middle” because they sit in the middle of a spectrum between detached single-family homes and mid-rise to high-rise apartment buildings in terms of form and scale, the number of units, and oftentimes, affordability.

However, they are not friendly to the business model of production builders and big finance, which has been characterized as “predicated on vast amounts of institutional complexity and debt.”

In many cases, developing this “Missing Middle” is blocked by the status quo of special interest groups seeking to protect property values and tax revenues, by keeping the “unwanted” out.

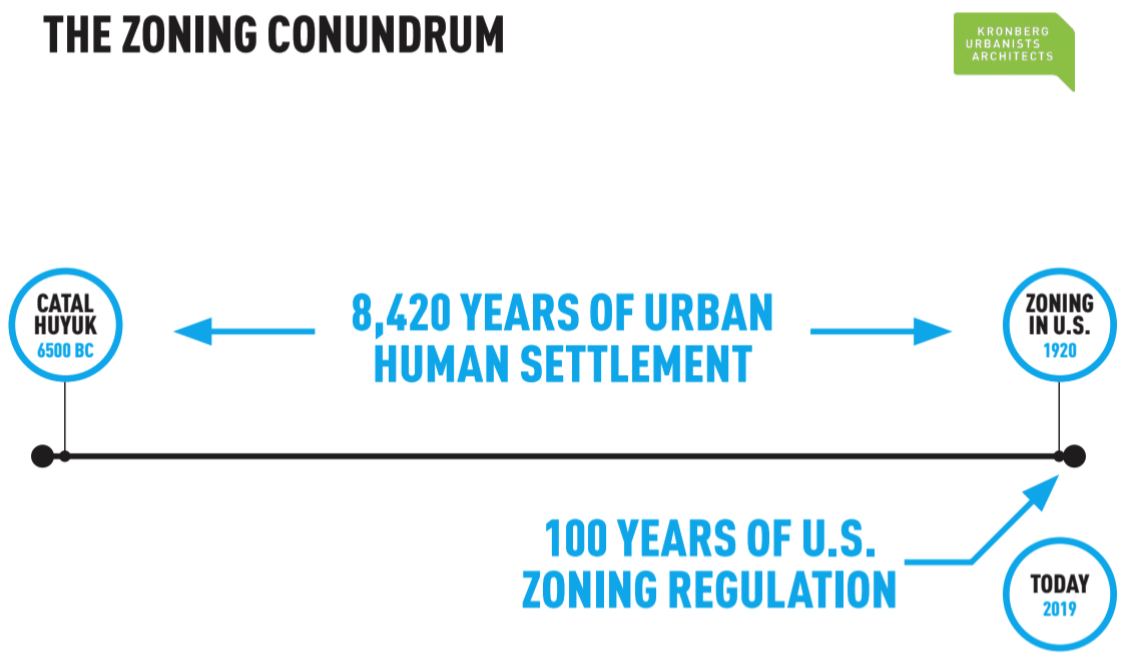

While zoning remains invisible to many people, the problems it's connected to increasingly are not. Cities have typically prioritized single-family homeowners above other groups, with the old belief that dense housing hurts their property values.

That conviction is at least as old as the 1926 Supreme Court decision that upheld zoning in America (Village of Euclid v. Ambler Realty Co., 272 U.S. 365).

According to the opinion delivered by Supreme Court Justice George Sutherland:

These reports, which bear every evidence of painstaking consideration, concur in the view that the segregation of residential, business, and industrial buildings will make it easier to provide fire apparatus suitable for the character and intensity of the development in each section…

With particular reference to apartment houses, it is pointed out that the development of detached house sections is greatly retarded by the coming of apartment houses, which has sometimes resulted in destroying the entire section for private house purposes; that, in such sections, very often the apartment house is a mere parasite, constructed in order to take advantage of the open spaces and attractive surroundings created by the residential character of the district.

… until, finally, the residential character of the neighborhood and its desirability as a place of detached residences are utterly destroyed.

Since then, no one has challenged the policing powers held by municipalities to enforce zoning laws… and the economic consequences for those deemed “undesirable” have been enormous.

We need states to step in and preempt municipalities from enacting and enforcing land use restrictions that raise housing costs.

Land use control is a police power that is constitutionally guaranteed to states, not cities. While states often delegate the power to municipalities, they can take it back when cities don’t use it for the public benefit

As you may already know, household wealth in the U.S. is mostly a function of real estate ownership.

It’s also the primary source of the racial wealth gap, largely due to a history of legalized discrimination called “redlining.”

In 1933, faced with a housing shortage, the federal government began a program explicitly designed to increase — and segregate — America's housing stock.

Author Richard Rothstein says the housing programs begun under the New Deal were tantamount to a "state-sponsored system of segregation."

The government's efforts were "primarily designed to provide housing to white, middle-class, lower-middle-class families," he says.

African-Americans and other people of color were left out of the new suburban communities — and pushed instead into urban housing projects.

Rothstein's new book, The Color of Law, examines the local, state and federal housing policies that mandated segregation.

The Federal Housing Administration's justification was that if African-Americans bought homes in these suburbs, or even if they bought homes near these suburbs, the property values of the homes they were insuring, the white homes they were insuring, would decline. And therefore their loans would be at risk.

It was in something called the Underwriting Manual of the Federal Housing Administration, which said that "incompatible racial groups should not be permitted to live in the same communities." Meaning that loans to African-Americans could not be insured.

However, like many narratives – especially ones related to racial discrimination – the truth is often messier and more complicated than meets the eye.

Source: Kronberg Urbanists + Architects

As we altered our systems to legally and administratively favor single-family homes, we changed how people build wealth – from an income-based paradigm to an asset-based paradigm.

Prior to the 1920s, the way in which real estate was used to build wealth was fundamentally different than it is today. Because there weren’t any zoning laws to “protect” the value of the property, the only real value in real estate was the income the property generated.

This meant that anyone who owned land could earn extra income by building additional rooms.

When wealth is created primarily by income, it encourages a fairly entrepreneurial approach to the asset class, which tends to drive positive outcomes – for both personal wealth creation and the health of the surrounding community.

Under an income-based paradigm, more people are better (more customers), more variety is welcome (diversity of products), and more wealth is created at the local level through increased local participation.

All of that changed thanks to zoning’s ability to artificially restrict supply, and therefore artificially boost asset prices: If the value of your asset is directly tied to supply and demand, fewer houses are better (less competition), less variety is welcome (standardization of products), and less wealth is created at the local level, as more of it is absorbed by the landlords and financiers.

Rapid industrialization and the American ascendance on the world stage created greater societal wealth. With our increasing wealth, we began to codify the single-family detached house as the societal ideal, and we set up all sorts of mechanisms to protect that type of building.

We created special financing programs for houses, especially for newly-built ones in the New Deal and after WWII.

We created zoning laws starting in the 1920's that kept out other types of housing, and we created building codes that made multifamily housing more expensive to build.

Under the asset-based paradigm of the last 100 years, wealth has been "created" by the price of the asset – in this case, a house – going up and then capturing financial gains through buying and selling the asset (or by using creative financing arrangements).

Property owners now have real economic incentives to force exclusion through regulations.

More specifically, these exclusions provided an opportunity for more standardized “monoculture” developments that are easier to underwrite, and therefore, easier to expand financing options.

This meant Wall Street could more easily package mortgages into mortgage-backed securities to sell to large institutional investors.

The Critical Question:

Why is Affordable Housing So Expensive to Build?

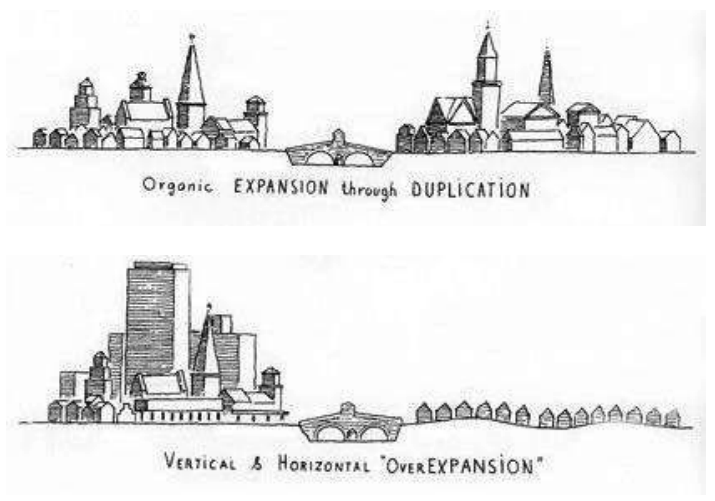

For the last century, almost all the rules around development have been written in ways that entrench the dominance of a few styles of development.

Most notably, the regulatory and financial system we have today is optimized to build the “cookie cutter” monoculture developments of the Suburban Experiment.

The Suburban Experiment can be described, using this illustration by Léon Krier, as a sudden shift from the model of growth depicted on the top—organic expansion through duplication of an existing development pattern based on multi-purpose complete neighborhoods—to the model depicted on the bottom— horizontal hyper-growth, with the rise of a skyscraper district in the core dependent on suburban commuting

Source

However, it also punishes the type of incremental infill – the Missing Middle – that was once underwritten by community lenders and residents, for an unexpected reason…

There’s not enough liquidity in a secondary market to effectively securitize and syndicate these types of loans.

Today, there is a massive secondary market for home mortgages, dominated by Fannie Mae and Freddie Mac, which buy home mortgages and bundle them into mortgage-backed securities (MBS).

These loans are a pretty typical financial product that offer low-interest rates, preferential terms, and a straightforward, streamlined process to qualify.

Today, the American MBS market is one of the largest and most liquid global fixed-income markets, with more than $12 trillion of securities outstanding (as of 4Q21) and ~$250 billion in average daily trading volume (as of February ‘23).

The catch is that all of these programs are designed to support primarily single-use, residential properties. There is no equivalent for mixed-use loans.

Because land-use regulation restricts the vast majority of urban land in the U.S. to single-use structures – and in the case of residential areas, typically 80% or more to single-family homes – banks don’t find it worthwhile to create loan products for building types that are uncommon.

This effectively shuts out the kinds of projects that many incremental developers want to do—urban infill buildings that are often mixed use, usually rental properties, and often denser and with less parking than has been the norm for the last 70 years.

Many of these issues date to the Federal Housing Administration’s original sin, in the 1930s, of defining mixed-use buildings and apartments as “hazardous” for the purpose of insuring loans, a key component of mortgage redlining.

These rules were intended to protect taxpayers from what were considered riskier commercial loans, even though much of Main Street America was built on the notion of mixed use.

Recent research indicates that single-use projects may actually be riskier than ones with higher shares of non-residential uses.

In recent decades and especially since 2008, mixed-use areas have gained or sustained value far better than single-use areas, contradicting the view that mixed-use neighborhoods are riskier.

This creates a strange paradox of market inefficiencies.

While there is clear demand for this type of mixed-use product, developers have a difficult time explaining why their non-conforming project is a good investment.

Final Thoughts: Could manufactured housing solve the affordable housing problem?

Because of these multiple and entwining issues, simple-sounding policy reforms aren’t going to fix the affordability problem.

To make a meaningful impact in the lives of the 38 million people who are cost-burdened today, outside of massive government subsidies, the only reasonable option is to implement rent controls and reduce property values.

For any elected official – especially of a financially distressed state or local government – this move would be political suicide.

This means long-term affordability has little to do with what we build this year or next, but rather, the decisions we make with our existing supply of homes, in which the vast majority of people live.

The most important thing we can do is protect the existing supply of affordable housing through professional management…

And we need a way to significantly reduce the cost of building new homes to meet the growing demand WITHOUT the need for expansive government subsidies.

The answer could be hidden inside a century-old solution, manufactured homes – formerly called “mobile homes.” They’re gaining ground as a viable homeownership option, and manufactured housing communities are a sought-after place to live.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |