- Private Capital Insider

- Posts

- 📈 Oil, Inflation, and the Biden Administration

📈 Oil, Inflation, and the Biden Administration

Private Capital Insider: Weekend Edition

Equifund: Weekend Edition

April 06, 2024

While everyone else is talking about the Truth Social insider trading drama, Tesla's weak performance in 2024, and the “end of days” conspiracy theories surrounding the upcoming total eclipse (featuring: ONE TRILLION cicadas that may have a sexually transmitted bug zombie disease)

Here are the stories you haven’t been hearing much about:

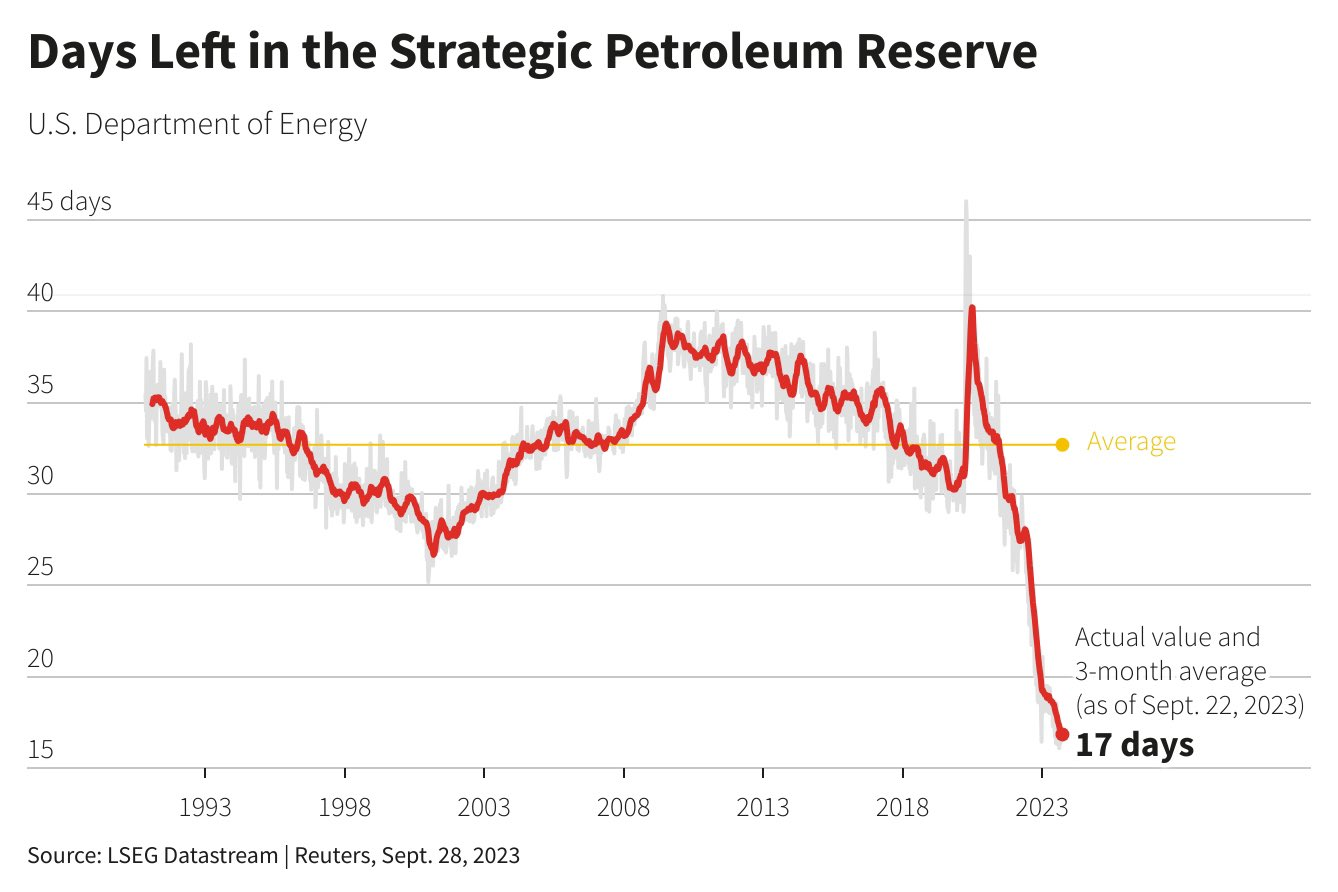

Biden administration cancels buyback of three million barrels to replenish oil stockpile. The Biden administration has canceled two planned oil purchases aimed at replenishing the Strategic Petroleum Reserve, the Department of Energy confirmed Wednesday, saying it was “keeping the taxpayer’s interest at the forefront” of its decision not to purchase as many as three million barrels of oil for a Strategic Petroleum Reserve site in Louisiana.

Probably nothing, right?

Oil Advances Near $90 as OPEC Sticks With Its Production Cuts: Brent crude rose to within one cent of the $90-a-barrel psychological level on Wednesday, after OPEC and its allies didn’t recommend any changes to their existing output cuts at an online ministerial review meeting. The move means roughly two million barrels a day of curbs will be in place until the end of June.

Natural Gas Prices Go Negative in Texas: Everyone is talking about oil prices, but nobody is talking about natural gas prices. Despite surging industrial capacity, natural gas prices in Texas are negative because there’s simply not enough pipeline to carry all the production.

What does this all mean for Oil, Inflation, and the Biden administration?

That’s the topic of today’s issue of the Weekend Edition.

-Equifund Publishing

P.S. Interested in investing in oil and gas? Pytheas Energy – an AI-powered, early-stage oil and gas producer operating in Texas – is raising capital on the Equifund Crowd Funding Portal.

P.P.S. In case you’re looking for the weekly update on the biggest story no one in the mainstream media seems to care about…

Gold AGAIN hits new highs in basically every single currency…

And now, it looks like we’re building momentum into the much fabled “silver squeeze”.

We’re going to stay focused on energy for today’s issue. But if you’d like to read our previous coverage on the gold markets, check out some of our back issues.

When History Repeats Itself

Generally speaking, people love to pull out sage-sounding advice in the form of quotes from “famous” people – especially when it comes to investing.

For example, Mark Twain (allegedly) said, “History doesn’t repeat, but it often rhymes.”

Winston Churchil famously said, “Those that fail to learn from history are doomed to repeat it.”

And today, we are going to say, “Maybe people did learn from history, and maybe it’s not an accident that it’s repeating.”

Why? Because over and over again, we’ve heard that today’s global economy is eerily similar to the 1970’s “stagflation” episode – a mixture of slowing economic growth with rising inflation.

Don’t take my word for it. Here’s some of the headlines in 2024 from the mainstream financial media.

Source: Business Insider

Source: Fortune

Source: Bloomberg

And just in case your 2024 outlook wasn’t going to be spicy enough…

There’s now growing speculation the Federal Reserve WILL NOT cut rates this year as many expected (or even counted on).

In fact, we could see the Fed be forced to continue to raise rates to tamp down inflation…

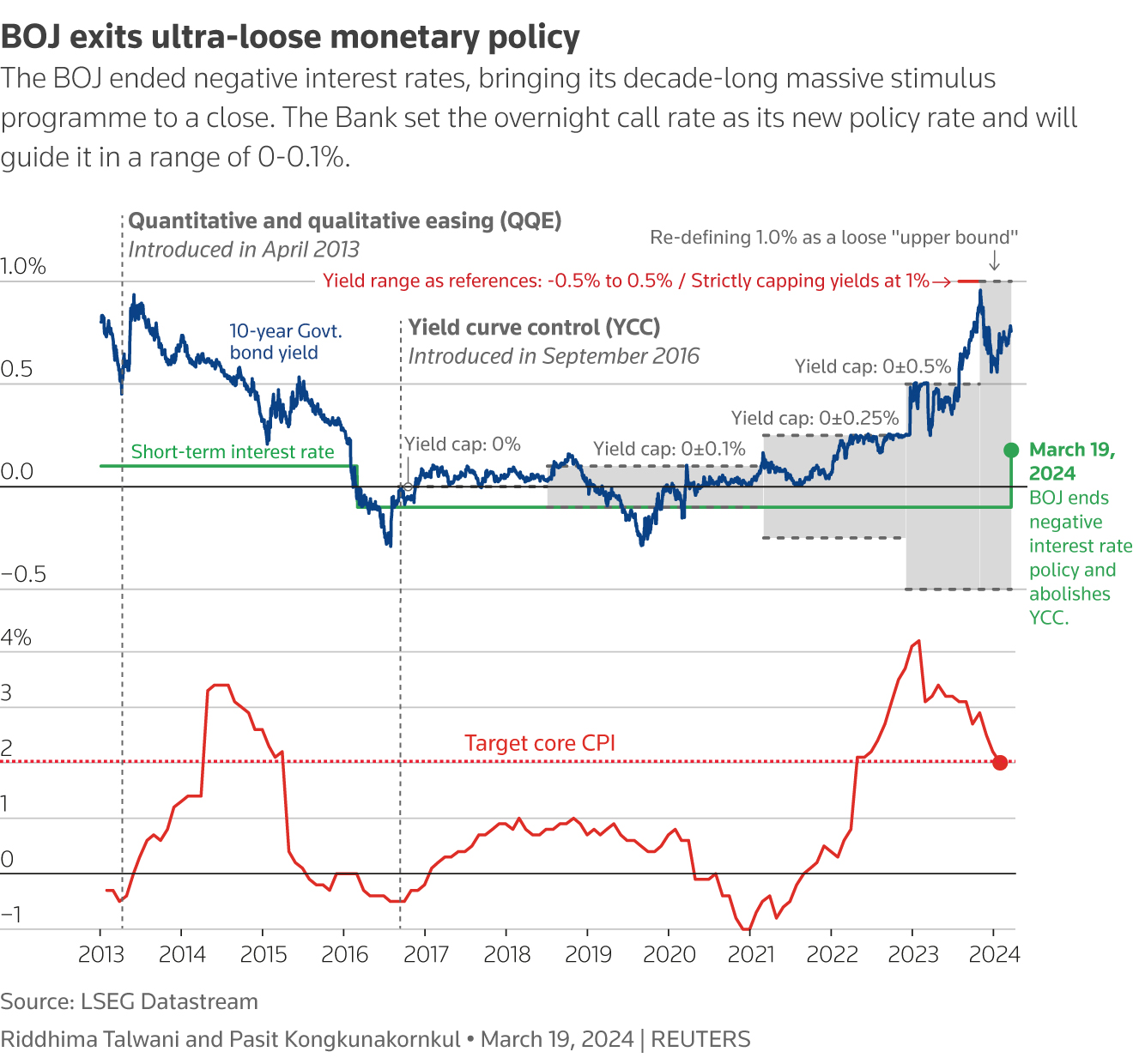

Especially as Japan officially ends the Era of Negative Interest Rates with its first rate hike in 17 years.

And if there’s anything we’ve learned about inflation since 2020, the rise in energy prices is probably the single biggest driver.

So how does our current situation compare to the 1970s? Let’s take a look.

On October 19, 1973, immediately following President Nixon’s request for Congress to make available $2.2 billion in emergency aid to Israel for the conflict known as the Yom Kippur War, the Organization of Arab Petroleum Exporting Countries (OAPEC) instituted an oil embargo on the United States.

The embargo ceased U.S. oil imports from participating OAPEC nations, and began a series of production cuts that altered the world price of oil.

These cuts nearly quadrupled the price of oil from $2.90 a barrel before the embargo to $11.65 a barrel in January 1974.

As Arthur Burns, the chairman of the Federal Reserve at the time, explained in 1974, the “manipulation of oil prices and supplies by the oil-exporting countries came at a most inopportune time for the United States.

In the middle of 1973, wholesale prices of industrial commodities were already rising at an annual rate of more than 10 per cent;

our industrial plant was operating at virtually full capacity;

and many major industrial materials were in extremely short supply”

In addition to these cost pressures, the U.S. oil industry had a lack of excess production capacity, which meant it was difficult for the industry to bring more oil to market if needed.

Thus, when OAPEC cut oil production, prices had to rise because the American oil industry could not respond by increasing supply.

Fed Chairman Burns argued in 1979 that the inflation appeared to be the result of a plethora of forces: “the loose financing of the war in Vietnam … the devaluations of the dollar in 1971 and 1973, the worldwide economic boom of 1972-73, the crop failures and resulting surge in world food prices in 1974-75, and the extraordinary increases in oil prices and the sharp deceleration of productivity”

Economists have since come to understand that a central bank can influence the extent to which supply shocks affect inflation, but they face a trade-off.

Higher oil prices, because of the widespread effect they have on commodities throughout the economy, will tend to generate both inflationary pressures and slower growth.

To find out what rhymes with this piece of history, let’s take a look at how we’re doing across these various indicators.

Industrial Capacity: Even though we are seeing a prolific boom in the reindustrialization of America, we are absolutely lacking in terms of industrial capacity – especially relative to Russia and China.

U.S. Treasury Secretary Janet Yellen recently slammed China’s use of subsidies to give its manufacturers in key new industries a competitive advantage, at the cost of distorting the global economy, and said she plans to press China on the issue in an upcoming visit.

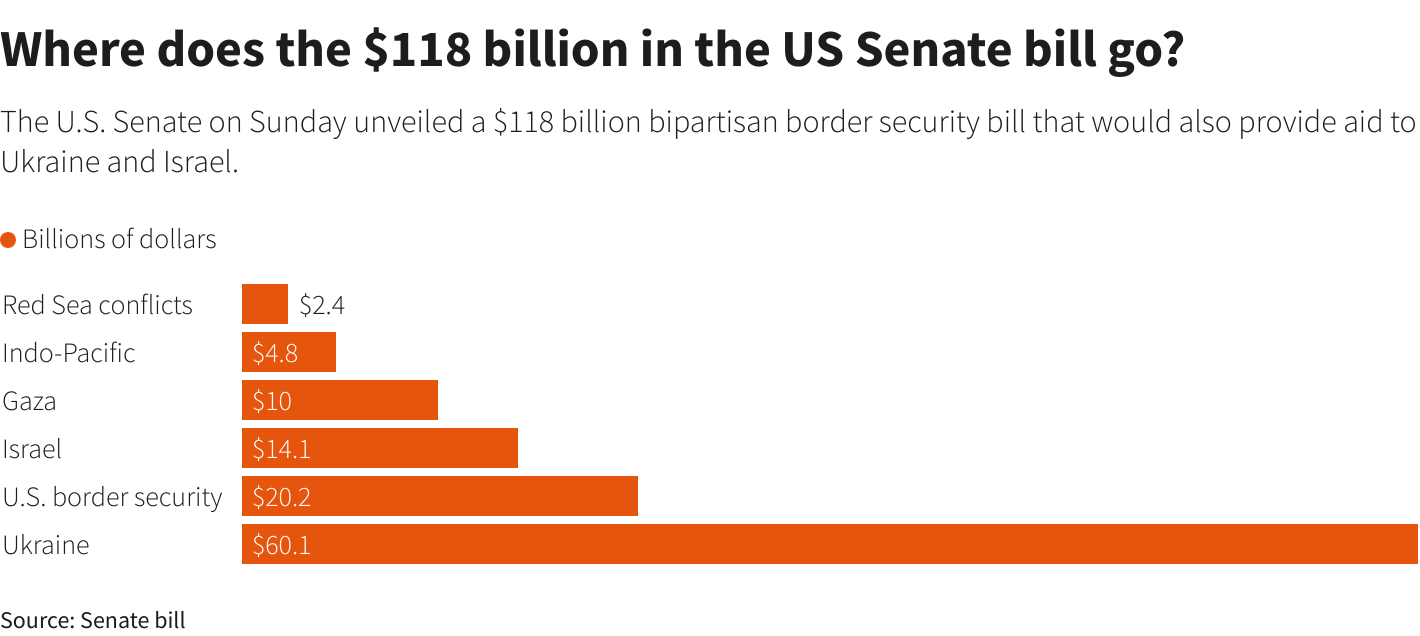

Loose War Financing: Since the Israel-Hamas war started, the U.S. has given Israel about $3.8 billion. Since the war in Ukraine started, the U.S. has given Ukraine $115 billion.

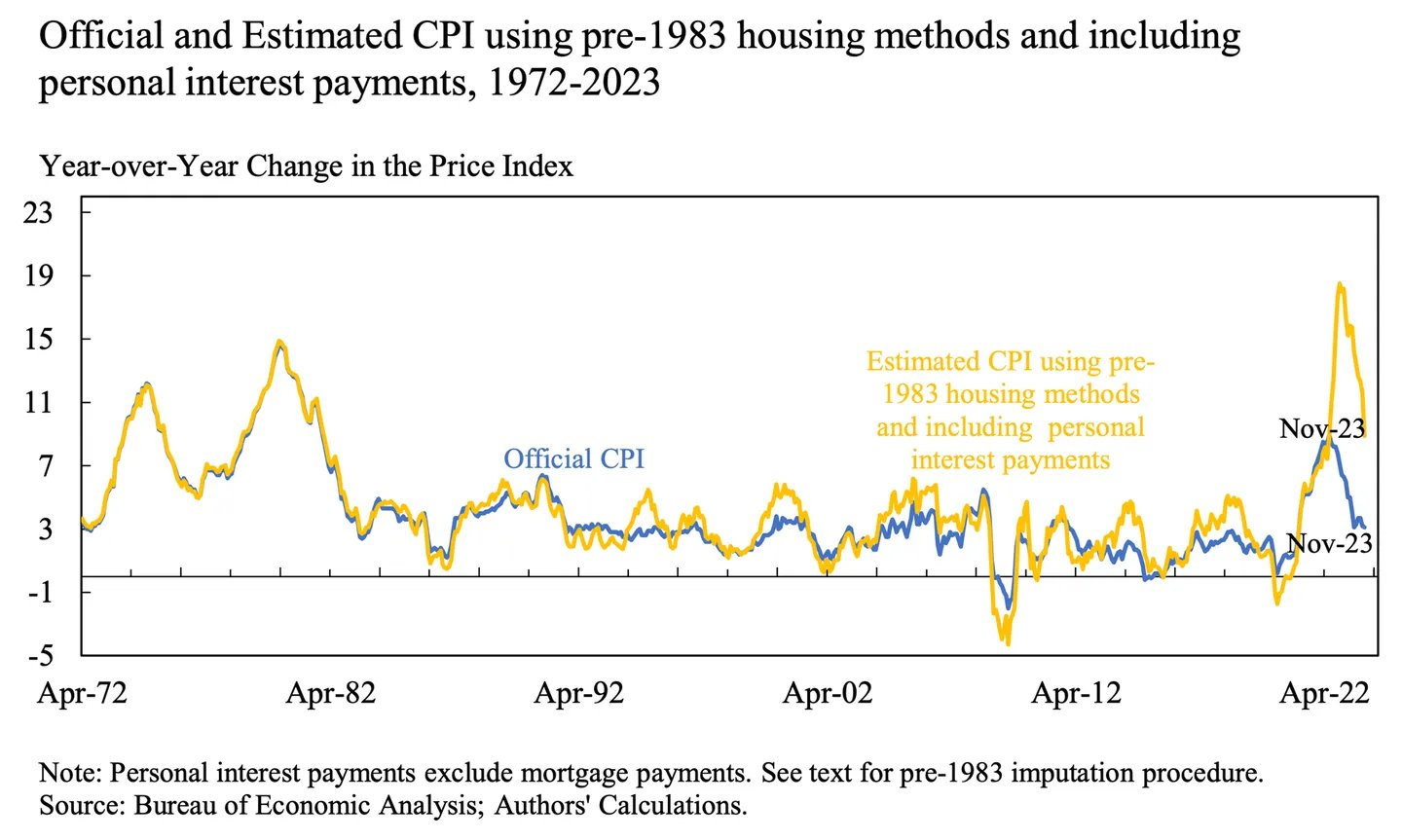

Home Prices: if we use pre-1983 housing methods, homes are four times more expensive than official inflation numbers.

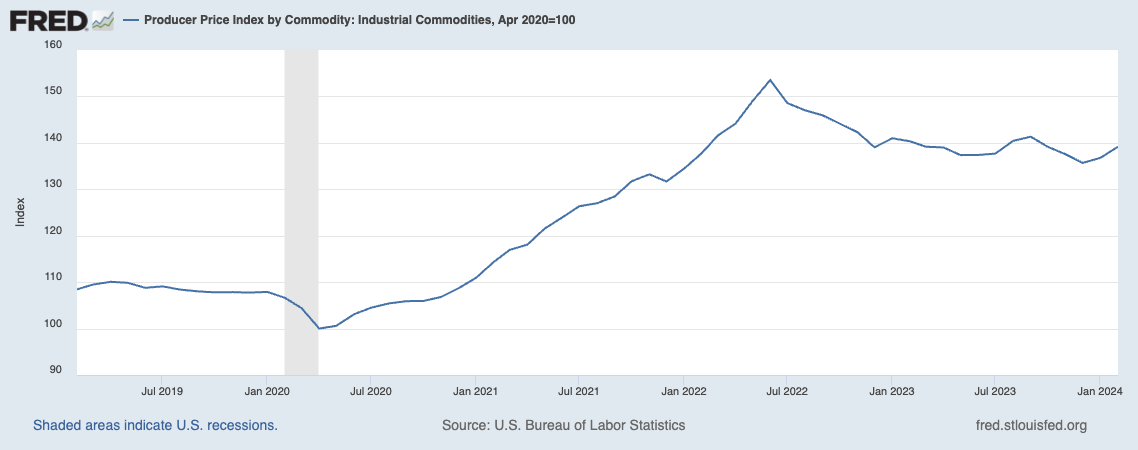

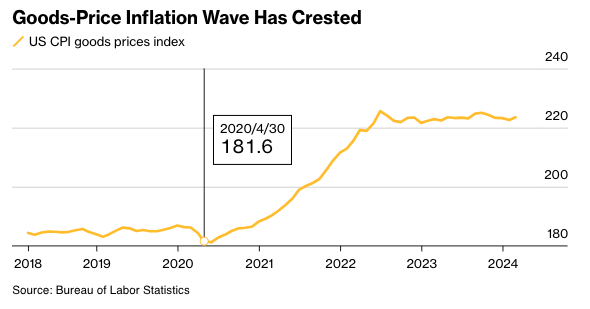

Producer Price Index by Commodity: Industrial Commodities: Since April 2020, we’re up ~40%.

Consumer goods: up ~18% since April 2020.

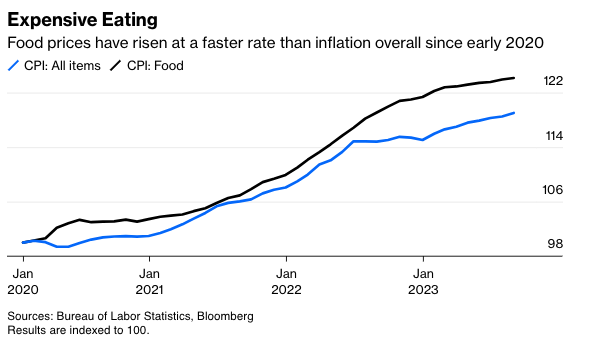

Food prices: up ~24% since 2020, and account for one-sixth of the increase in consumer prices overall.

What’s to blame? The official narrative is a combination of “shrinkflation” and “disruption in the supply chain.”

Let’s start with the Shrinkflation theory.

According to the United States Senate Committee on Agriculture, Nutrition, & Forestry:

In his latest effort to avoid responsibility for the historic inflation in food and grocery prices, President Biden tried to lay the blame at the feet of food companies-- accusing them of a practice called “shrinkflation” -- during his State of the Union Address.

This follows a similar effort in 2021 to blame inflation on food processors.

However, he will need to keep searching for a scapegoat as data from the Bureau of Labor Statistics (BLS) reveals that product downsizing played only a minor role in the rapid increase in food prices that occurred under this administration.

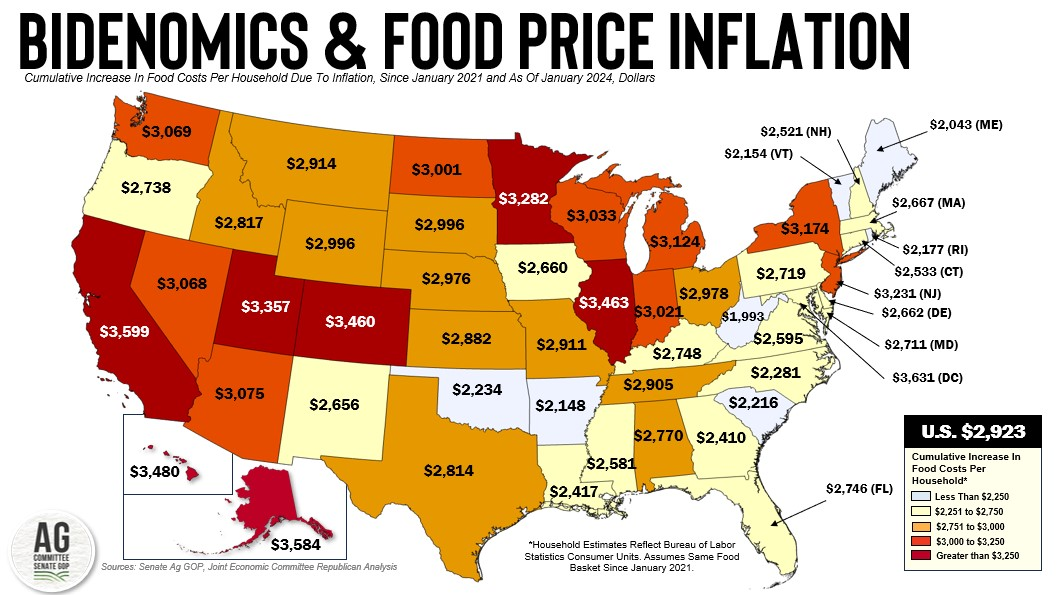

Across the U.S., the cumulative increase in food costs paid by households under this administration ranges from a low of nearly $2,000 in West Virginia to more than $3,000 in Alaska, California, Colorado, the District of Columbia, Hawaii, Illinois, Minnesota, and Utah. Source: US Senate

Don’t get me wrong. I’m also upset that candy bars and Girl Scout cookies have been a little bit smaller these past few years…

But, maybe it’s just higher oil prices?

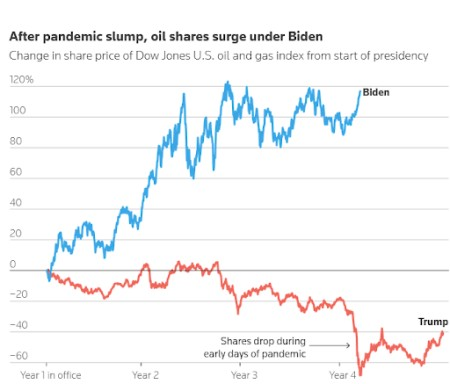

In other news, oil stocks are up ~120% since Biden took office vs a ~50% slump under Trump.

To be fair, COVID heavily distorted these numbers in both directions by creating what could be considered an artificial depression/recovery.

Under Trump, we could suggest oil stocks were down 20% prior to COVID, down 50% during COVID, and Biden got to step in to benefit from the recovery (it takes a 100% gain to overcome a 50% loss).

We saw a similar dynamic play out during the 2008 housing crisis with Bush/Obama.

Now let’s take a look at supply chain issues

The major supply chain story of the week is the Baltimore Bridge Collapse – the second largest business infrastructure coordinator in the United States.

The collapse of Baltimore’s Francis Scott Key Bridge, which severed ocean links to the city’s port, adds a fresh headache to global supply chains already struggling with the effects of war, climate change and higher interest rates.

Tuesday’s mishap means a significant disruption for East Coast shipping, with trade in autos, coal, and machinery likely to be the hardest hit, according to government officials and industry executives.

It comes as global shippers are grappling with a historic drought that has left the Panama Canal without enough water for routine operations, as well as two wars in Europe and the Middle East that have turned routine commercial voyages into daring adventures.

But for those of you who find many of the issues surrounding this “accident” rather suspicious…

Three ships have hit bridges in three different countries – in just three months.

Speaking of ships…

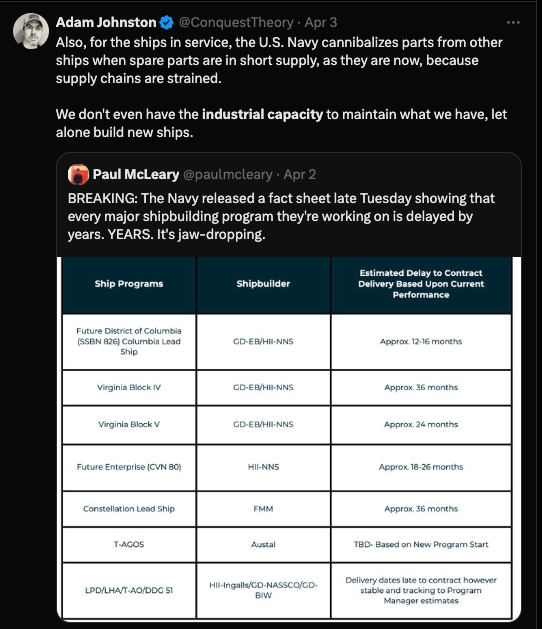

Despite the fact that the U.S. once was a prolific ship builder in WWII and beyond, today, the U.S. commercial ship industry has basically vanished.

At the beginning of 2023, China had 1,749 large oceangoing commercial vessels under construction in its domestic shipyards. America had five.

At the beginning of 2022, China had 1,708 vessels under construction. America had three.

While China consolidates its role as the world’s leading commercial shipbuilder with 40% of global output, the United States produces about one-fifth of one percent of global output.

Even worse, not only does America lack the industrial capacity to maintain the ships we do have…

We have basically no ability to build new ones to replace our aging fleet.

Are you hearing the rhymes yet?

With all that said, there is one noticeable difference between the 1970s and the 2020s…

America is currently the world's largest producer of crude oil, and U.S. suppliers are muscling into OPEC+ territory all across the world.

According to Gary Ross, an oil consultant turned hedge fund manager at Black Gold Investors, “US production is going up and OPEC and Russian production is going down — so the US, by definition, is going to have more market share.”

So, I guess the only real question we have left to ask ourselves is this:

Are we on the cusp of a 1970’s style “oil squeeze” that sends prices soaring?

As usual, we’re not going to make predictions about what the markets will do next.

But we’re most certainly paying attention to the setlist the “band” is playing.

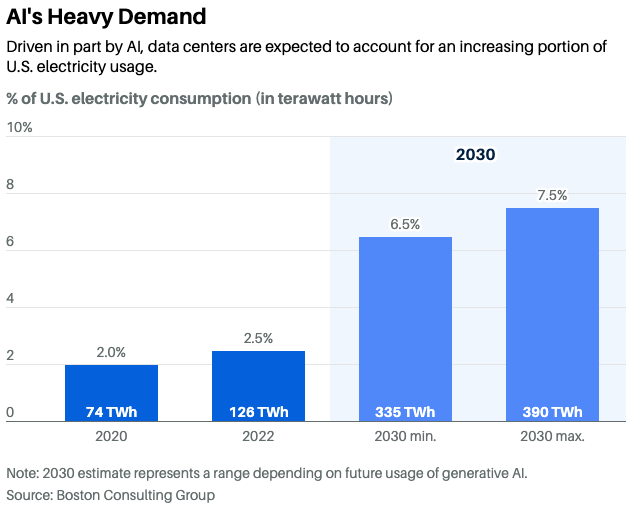

And to us, it sure sounds like energy demand is only set to increase in the coming years ahead – especially with the power-hungry loads required by AI data centers, which require 5-10x as much power per server rack.

According to Elon Musk, “Next year, you will see that they just can’t find enough electricity to run all the chips.”

So if you’re looking for a way to get exposure to the “Just Add AI!” hype cycle – and the prospect of higher energy prices…

Maybe now is the time to consider investing in oil and gas.

Or if you’re feeling a little bit adventurous, maybe you’re considering an investment in an AI-powered oil and gas company.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |