- Private Capital Insider

- Posts

- 📈 Is oil and gas a good investment?

📈 Is oil and gas a good investment?

An Insider's Guide to Investing in Oil and Gas

Jake @ Equifund

March 28, 2024

Before the Industrial Revolution, agricultural staples like corn and wheat ruled the commodities markets.

Today, crude oil – and it’s derivatives – reign supreme.

While most people think of oil as primarily a source of energy to power cars, trains, jets, and ships…

Oil is the most actively traded commodity in the world, touching almost every aspect of the global economy.

Refined oil (aka “petroleum products”) is used to make thousands of products we use on a daily basis.

Even though it’s hard to argue the importance of renewable energy sources, crude oil isn’t going anywhere for the foreseeable future.

In fact, based on some of the growing anti-ESG sentiment, backpedaling on things like fully-electric vehicles in favor of gas hybrids, and what could be a looming supply shortage in 2024/2025…

We could be entering a new era of elevated oil prices (and oil profits).

But most investors have little to no experience investing in commodity-based businesses – much less one as volatile as oil.

So if you’re seeing a potential opportunity in the oil and gas industry like we do… and you’d like to get yourself oriented as to how this major industry segment works…

Today is Part 1 of a multi-part series we’re publishing on Investing in American Oil and Gas.

-Jake Hoffberg

P.S. Interested in investing in oil and gas? Pytheas Energy – an AI powered, early-stage oil and gas producer operating in Texas – is raising capital on the Equifund Crowd Funding Portal.

P.P.S. It seems like our latest issue of the Weekend Edition – Texas, BlackRock, and American Oil – hit a nerve with our readers.

At the end of this issue, I’ll be posting some of the poll responses we received.

The consolidation of the $604bn U.S. Oil and Gas industry

With an estimated $3 trillion up for grabs each year, the global oil and gas (O&G) industry has been one of the most important – and potentially lucrative – markets over the past 160 years ($604.8 billion in U.S. drilling and extraction alone in 2023).

Not only does this commodity serve as the backbone of energy infrastructure everywhere, for decades, O&G stocks have offered investors a much-needed source of diversification – and potential growth & income – for their portfolios.

In fact, companies like Exxon Mobil Corp (NYSE: XOM) and Chevron (NYSE: CVX) have increased their dividend payouts every year, for over 35 years… CVX for 36 years and XOM for 40, and counting. There’s no guarantee they’ll keep raising them, but that’s a pretty good track record.

However, despite the consistent payouts to investors, there's been no shortage of volatility since the 1970’s.

Here’s why…

At the core of the O&G industry lies two things: Economic interests (i.e., “energy security”) and national security interests (i.e., “energy independence”).

But traditionally, nations have had to make a choice between one or the other.

For energy independence, the goal is to remove our dependence on foreign oil – or at the very least, remove our dependence on the Middle East, and only buy from North American suppliers.

However, the trade-off with this model is the acceptance of higher prices.

For energy security, the goal is to have a reliable source of oil at stable prices. This typically means participating in the global oil market, and accepting supply from wherever it’s most efficient to do so.

Big Oil historically opposed energy independence, which often works to the advantage of their smaller, domestic Craft Oil competitors.

However, because of America’s unique position of having oil priced in dollars – along with its vast, and still untapped oil reserves – it’s the only country in the world that could potentially achieve both interests at the same time.

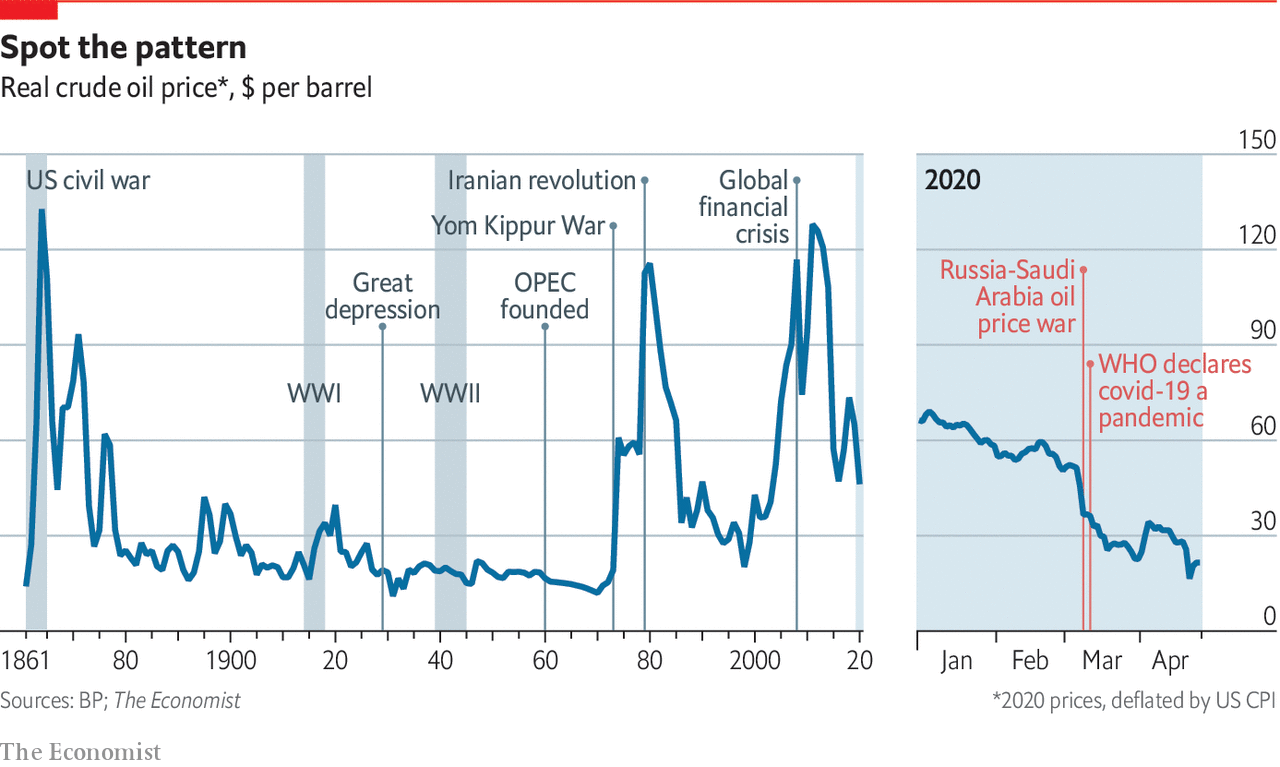

That’s why it’s important for any investor seeking to participate in O&G-related investments to understand that oil tends to operate in a cyclical manner – The Boom Bust Cycle

Source: The Economist

Oil’s Boom Bust Cycle Explained

During boom times, we hear greed-fueled stories in the mainstream media like this one from the Wall Street Journal:

But eventually, the proverbial music stops playing, and it all comes crashing down.

Why does it happen?

It has to do with the capital intensive nature of the business.

Unlike software startups that can be launched quickly and cheaply… producing, transporting, and refining O&G products requires considerable infrastructure and upfront capital expenditures to bring new projects online.

However, because the price of O&G is determined by supply and demand, changes in price can have significant impacts on investment activity in the sector.

Because of this, we see five predictable stages that drive the Boom Bust Cycle:

Stage 1: At the bottom of the cycle, there’s too much supply. This creates low oil prices and a period of under-investment by the oil industry. Generally speaking, low prices stimulate higher demand.

Stage 2: As demand increases relative to stable or easing supply, this causes prices to rise.

Stage 3: As prices rise, marginal projects become economically viable, and companies begin to deploy capital into expansion. The higher prices climb, and the longer they stay elevated, financiers and investors become more attracted to the opportunity.

Stage 4: As speculators begin to enter the market, price action begins to separate from underlying fundamentals. This inevitably leads to inflation, as high energy prices drive up the cost for everything else.

Stage 5: Eventually, a market shock causes a crash, leading to bankruptcies and consolidation, and the cycle begins again.

Throughout history, we can see one irrefutable fact about the oil industry: We oscillate between eras of relatively stable prices and eras of volatility.

The “Eras of Stability” depend on one major factor: a monopolistic entity (or “cartel”) to act as the “swing producer,” in order to regulate supply.

“Eras of Volatility” happen when the swing producer loses control – or is absent altogether – and new powers emerge.

Source: The Quest: Energy, Security, and the Remaking of the Modern World by Daniel Yergin

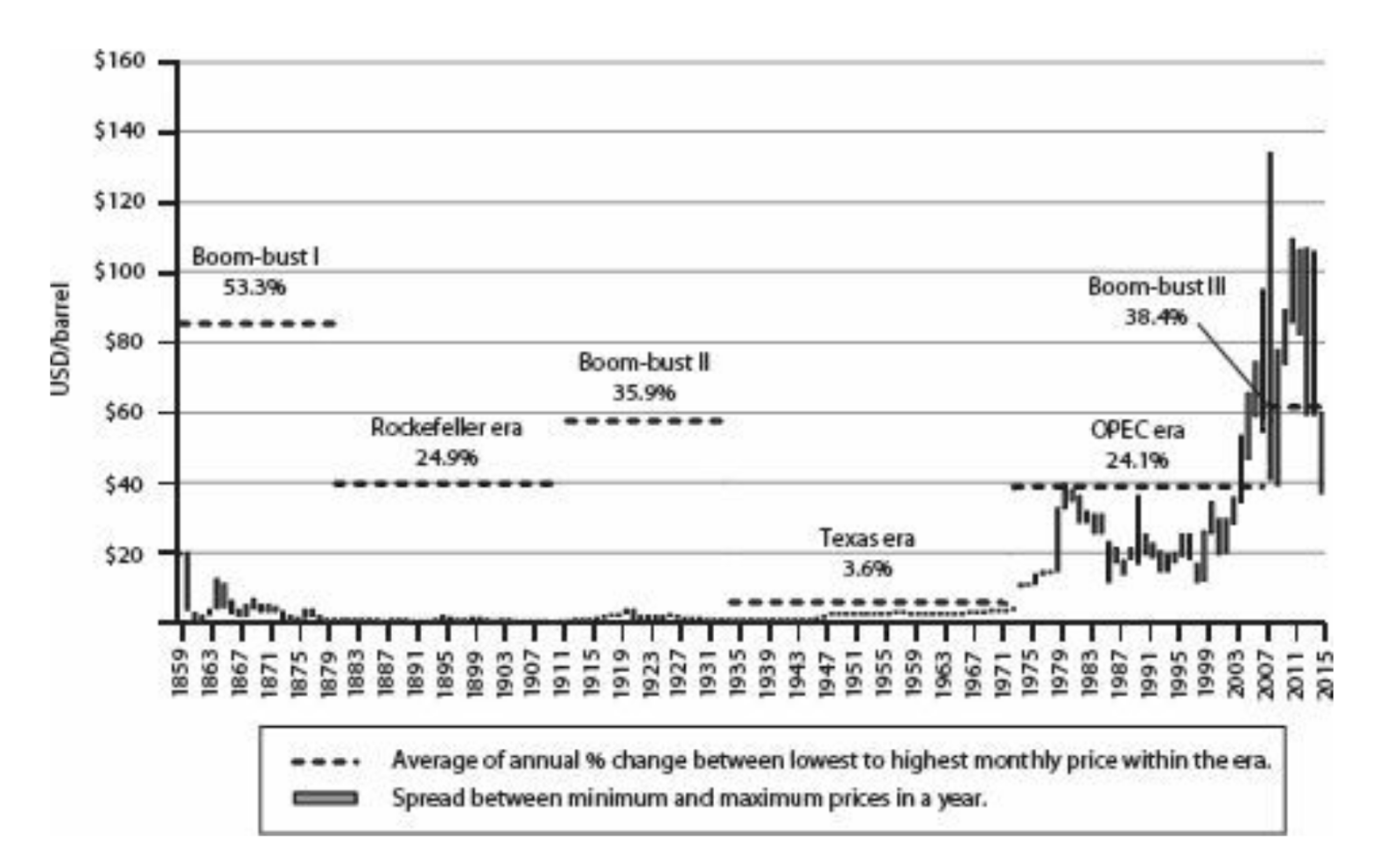

Between 1855 and 1879 (Boom Bust I) – when oil was first discovered in America – it was an all out “free market” war.

Then, John D. Rockefeller began to dominate the oil markets, and from 1880 to 1911 (The Rockefeller Era), the markets were brought under control and prices stabilized.

That all changed once the empire was broken up in 1911 via the Sherman Antitrust Act. From 1911 to 1931 (Boom Bust II), volatility returned in full force, with the price of oil being driven by the will of the “free market.”

In an effort to stabilize the markets, U.S. officials – most notably, the Texas Railroad Commission – imposed quotas.

Abroad, a new cartel of seven international oil majors – collectively known as the “Seven Sisters” – rose to control the newly discovered deposits in the Middle East.

Thanks to these controlling powers, between 1932 and 1972 (The Texas Era), the world enjoyed a level of stability never before seen.

Then, between 1973 and 2004 (The OPEC Era), the balance of power shifted firmly into OPEC’s hands, and more specifically, Saudi Arabia. With the largest proven oil reserves - that were also cheap and easy to recover - the Kingdom gained massive power over the global oil markets.

However, that all began to change, thanks to a new technology that unlocks “unconventional” oil reserves: horizontal drilling and hydraulic fracturing.

These two technologies led to the U.S. Shale Revolution, and marked the beginning of a new era of all-out oil wars between America and OPEC nations.

From 2004 to 2020 (Boom Bust III), monthly crude price changed an average of 38%, on par with the volatility from 1911 and 1931.

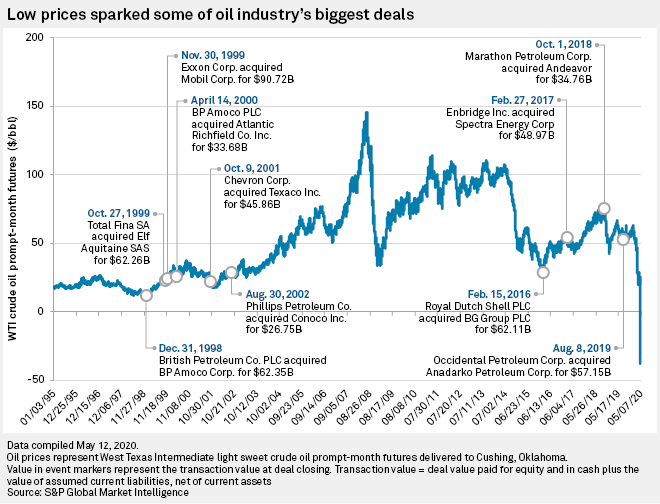

The biggest oil deals follow oil price crashes. Since 1995, more than 50 deals have been completed in the sector valued over $10 billion.

The priciest deals, excluding pipeline partnership reorganizations, all came after the market collapse in the late 1990s or the price fall that began in the second half of 2014.

Source: S&P Global

Fast and loose spending from the 2004 to 2014 exploration and production (E&P) rush saw 27 major oil producers triple capital spending. Over-leveraged oil companies that took on too much debt in 2016 were unable to refinance, causing a wave of bankruptcies that decimated U.S. oil producers.

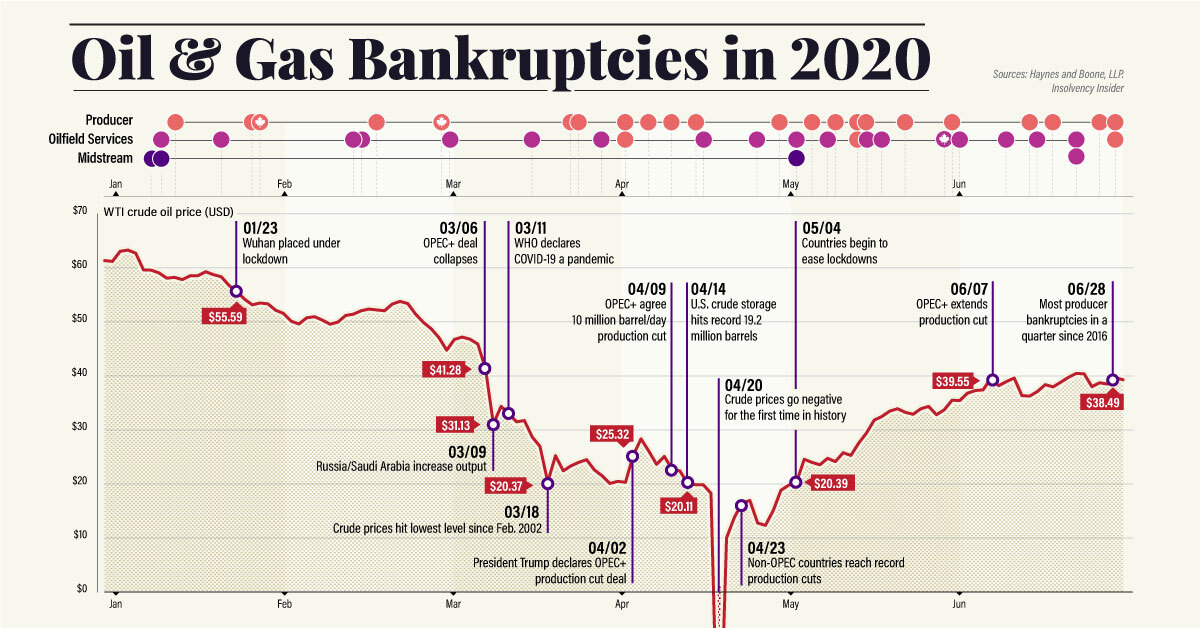

Over 100 small to mid-sized oil and gas companies went bankrupt between 2015 and 2020, including not only E&P operations, but also oilfield services, and even refineries.

Then, the famous COVID Crash of 2020 happened amidst shutdowns, a temporary supply glut, and a new wave of bankruptcies…

Source: Visual Capitalist

Yet, when demand returned following the COVID shutdowns, there weren’t plentiful new wells readily available to fill calls for more production.

Addressing the situation, Raymond James analyst Pavel Molcanov noted,

Oil and gas companies do not want to drill more.

They are under pressure from the financial community to pay more dividends, to do more share buybacks instead of the proverbial ‘drill baby drill,’ which is the way they would have done things 10 years ago.

This pressure, in turn, drives consolidation as companies seek to improve profits by achieving economies of scale…

Especially as supply uncertainty from OPEC+ led to lower, more volatile commodity prices.

Source: PeakOilBarrel.com

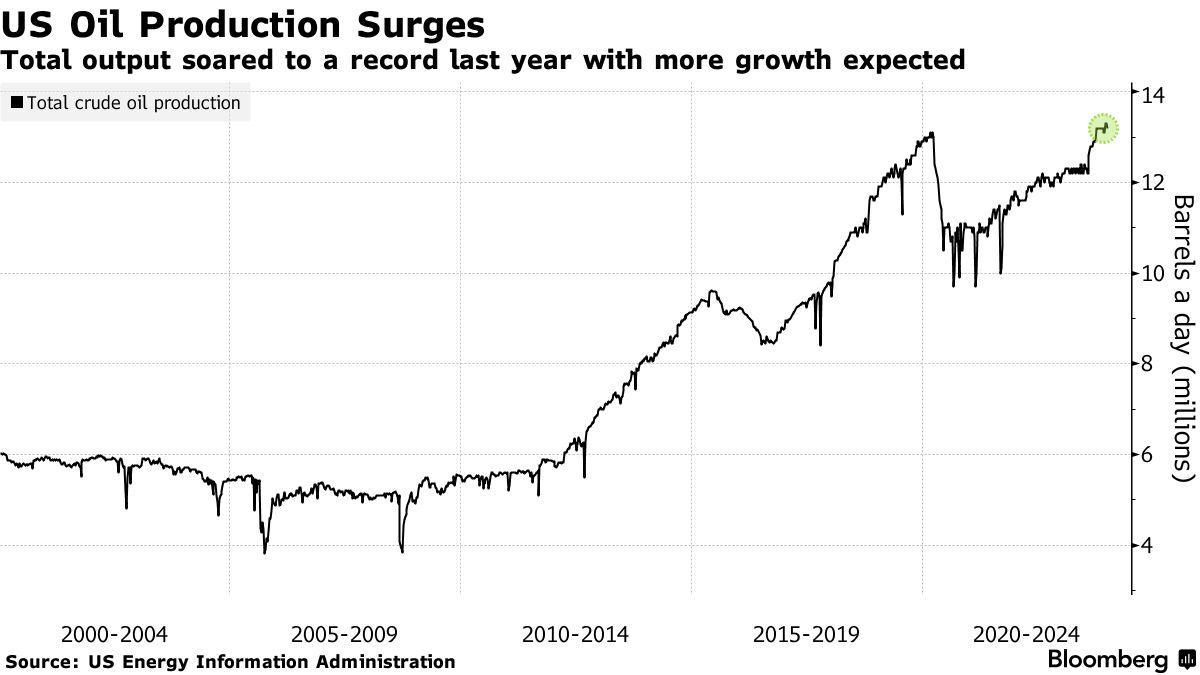

Thanks in part to sustained geopolitical tensions and supply chain issues, the American O&G industry quickly recovered and achieved record production levels in 2023 of 13.4 million average barrels per day (BPD), surpassing only 2019’s previous record highs, of 13.3 million BPD, according to the EIA, with some estimates reaching 13.5 million BPD.

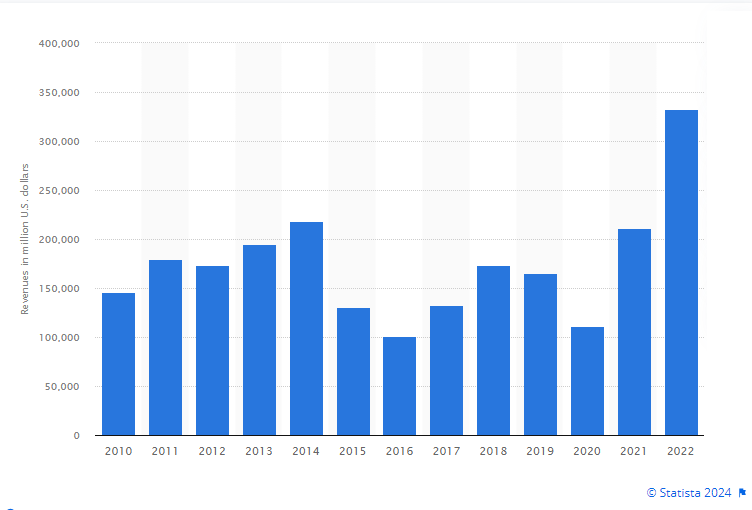

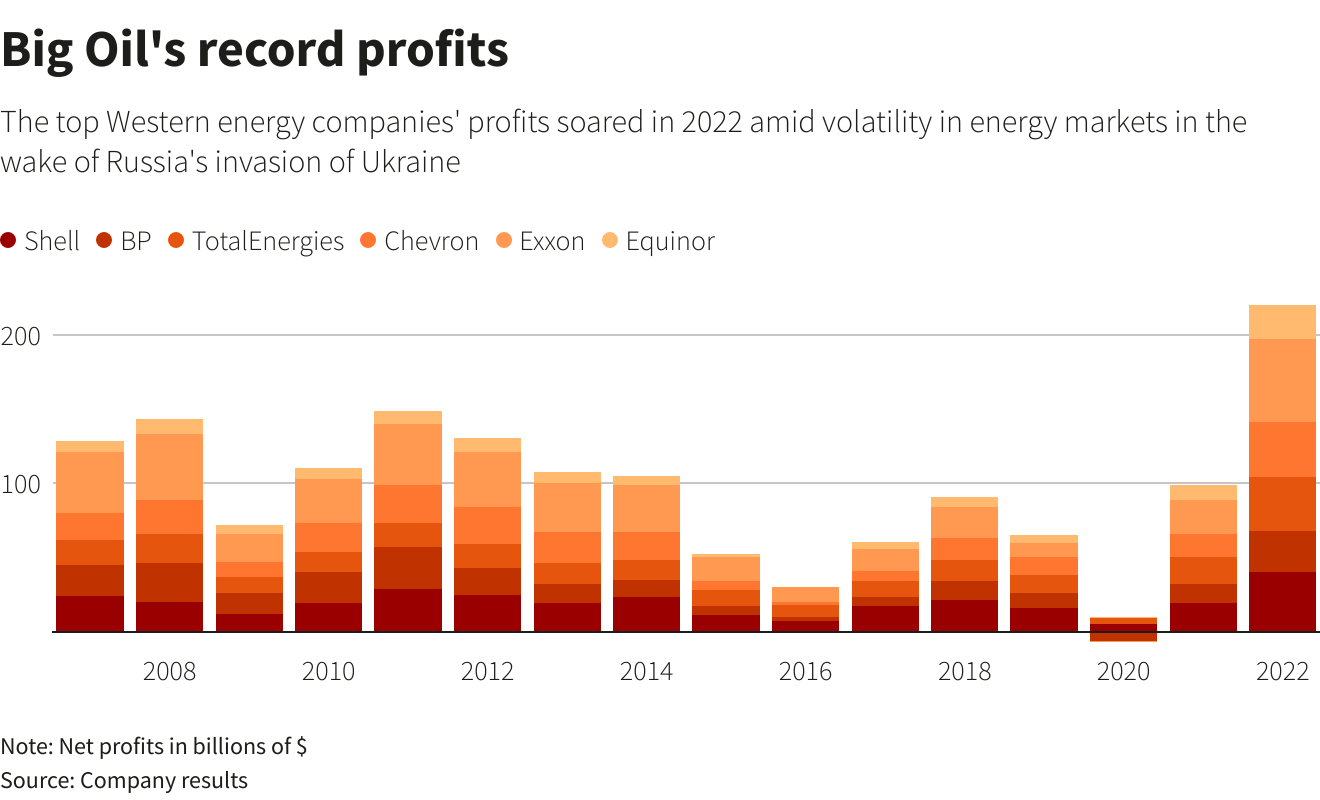

The industry also rocketed to record profits in 2022 of nearly $333 billion, up 63.4% from 2021.

We saw record high stock prices as 2022 drew to close, with the proxy S&P 500 Energy Sector Index reaching an all-time high.

However, despite President Biden’s climate agenda – which includes the bipartisan 2021 Infrastructure Law, and 2022 Inflation Reduction Act – American Oil has continued to pump record crude.

The industry has also produced record cash flows in 2021-2022…

Source: Reuters

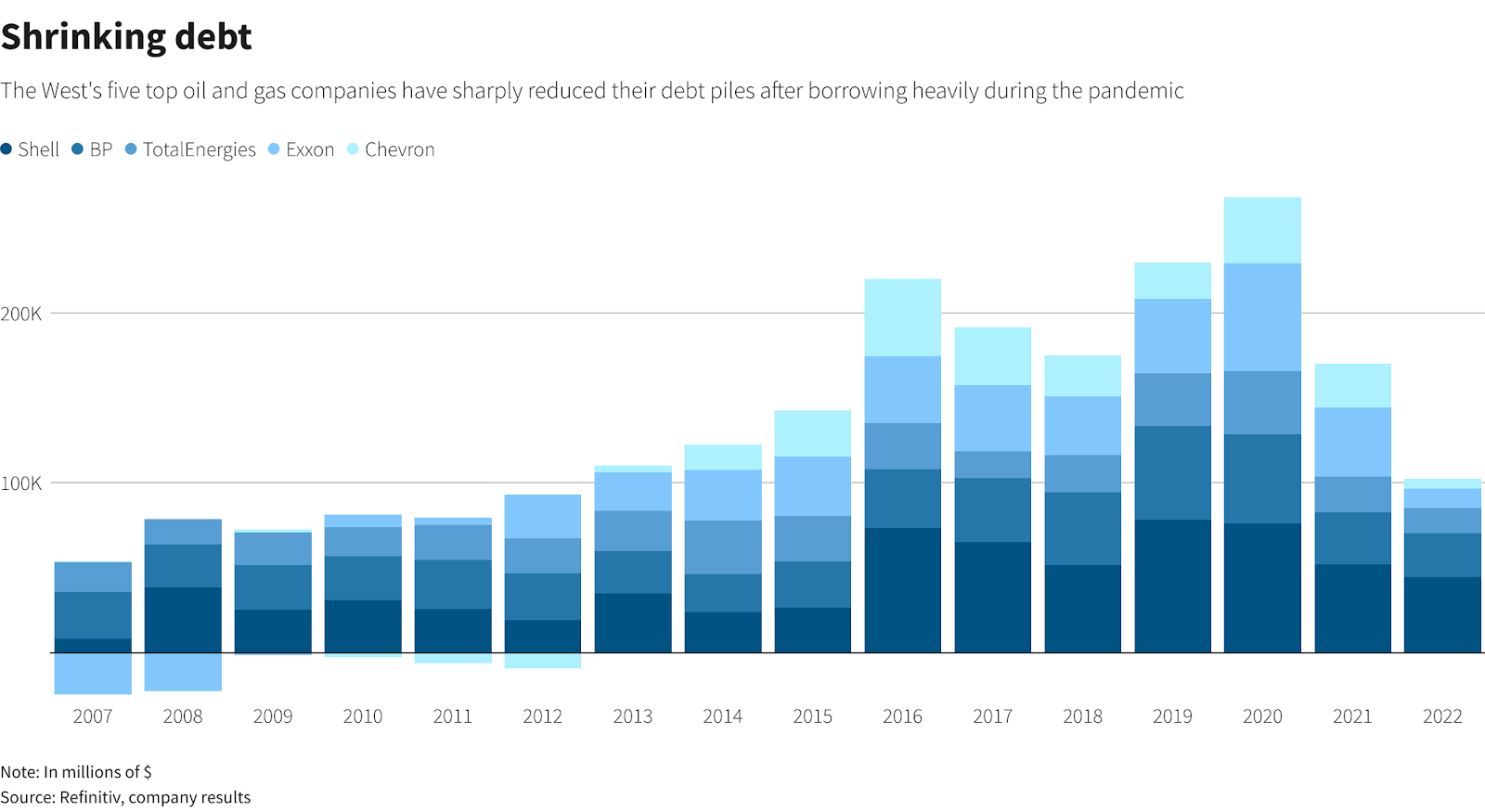

Significantly reduced debt…

Source: Reuters

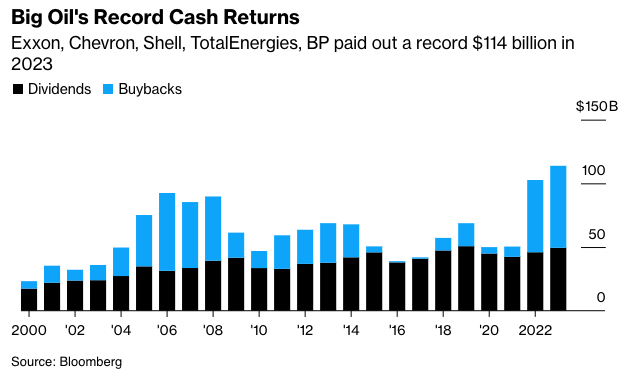

Not to mention, massive dividends and share buybacks for investors.

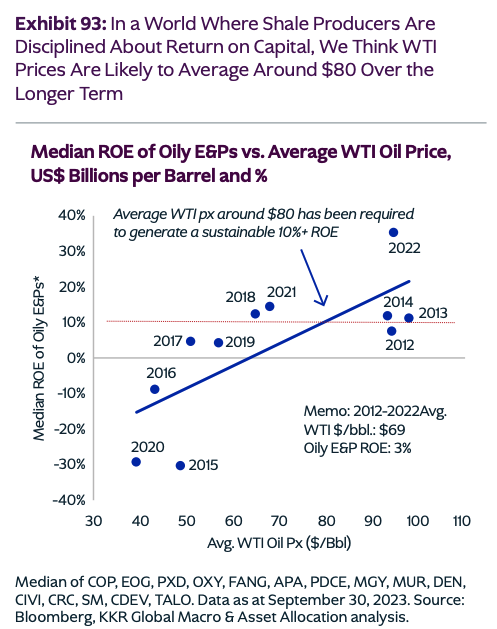

And if KKR’s forecast of ~$80-$100 per barrel in 2024 comes true, that will likely only continue to drive profitability for oil majors.

Source: KKR

All of which puts Biden (and the Democrats) in a weird position – According to the Washington Post,

The soaring domestic oil output has already begun to reshape geopolitical dynamics.

The United States is producing so much oil that it has undermined the influence of OPEC, which failed when it tried to make production cuts recently to drive prices up globally.

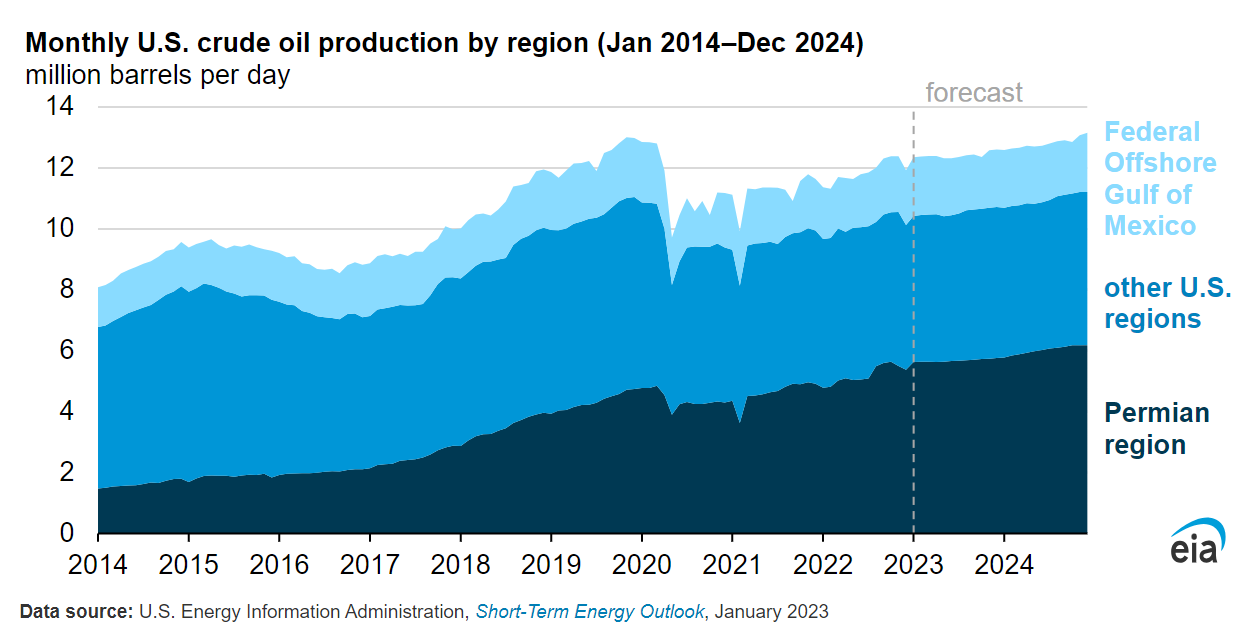

Even crazier? Permian oil production is projected to hit new all-time highs in 2024 – 6.4 million barrels per day (MMbpd) at the end of this year, up from 6.1 MMbpd at the end of 2023.

Thanks to the hostile posture coming from the Biden administration – as well as growing pressure to deal with environmental issues, the continued shift towards renewable energy, along with higher interest rates, and tighter credit conditions – the consolidation cycle has only continued to accelerate.

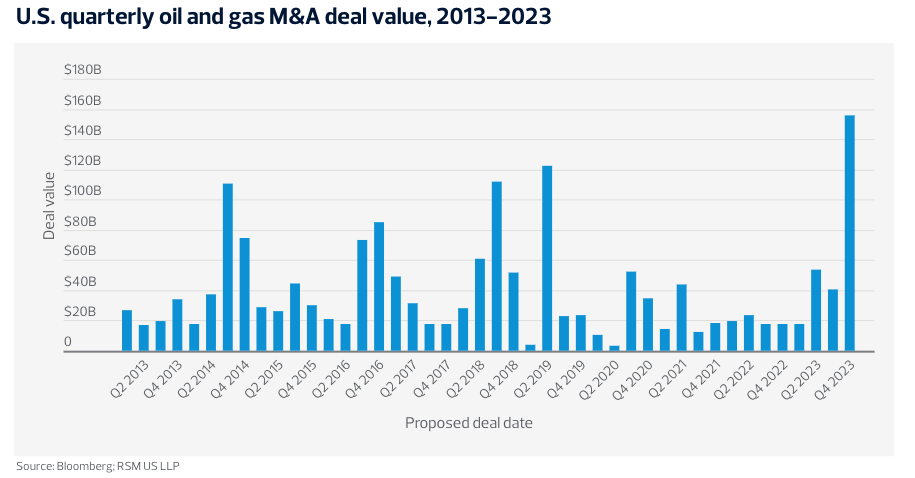

In recent months, the oil and gas sector has experienced a remarkable surge in merger and acquisition (M&A) activity, with over $155 billion in deals in the fourth quarter of 2023– more than the prior five quarters combined.

Similar to what we’ve seen in the gold mining industry, O&G companies started to grow through mergers and acquisitions, in order to achieve economies of scale, increase reserve depth, and gain/maintain market relevance.

This is especially the case in the most productive formation in America, the Permian Basin (i.e., West Texas and New Mexico)...

Source: EIA

All of which is becoming increasingly concentrated in the hands of Chevron, Occidental, ConocoPhillips, and ExxonMobil.

In 2023 alone, the industry had seen more than $250 billion in mergers and acquisitions by mid-December, according to Investors Business Daily. This was the highest annual year-to-date total since 2014.

Analysts are projecting that this M&A activity will steadily continue in the coming years, led by investments in the Permian. CFRA analyst Stewart Glickman said, "If you are going to grow in the U.S., it makes sense to try to either expand or find a foothold in the Permian. I think the wave of consolidation [will] continue.”

Drillers have been warning for a while that untapped acreage is running out, so acquisitions have essentially become the only option for producers that want to grow in the area—and many big players do want to grow in the area.

Earlier this year, the Energy Information Administration predicted that oil output in the Permian was declining for several months in a row.

For each of these months the EIA had to revise its figures after getting actual production data that showed output in the Permian was actually increasing.

There is still plenty of oil in the Permian that can be extracted relatively cheaply. That is why everyone with money to spend is rushing there to buy smaller rivals and expand.

And that is why some believe that by 2030, the U.S. oil industry could be a very different place than it is now.

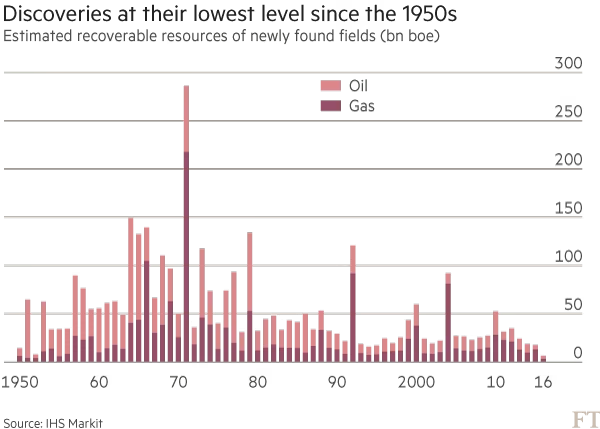

Also similar to the gold mining industry, there has been a severe lack of major oil discoveries in recent years, which only continues to put pressure on supply.

Which leads us to an uncomfortable question…

Is America Running Out of Oil?

Although the United States is currently the top producing country, every year of record production that isn’t replaced by new supply means our reserves are shrinking.

Discoveries of new oil and gas fields have dropped to a fresh 60-year low, as companies put a brake on exploration and large fields have become harder to find.

According to Occidental Petroleum's CEO, Vicki Hollub, over the past 10 years, the world has replaced less than half of the oil that was produced.

All the big fields have been found. So, if you take the 20 largest fields in the world, 97% of the volume from those was discovered before 2000.

So we're in a situation now where in a couple years' time, we're going to be very short on supply, so the situation is going to flip.

The slowdown in exploration success shows that the world is likely to become increasingly reliant on “unconventional” resources, such as U.S. shale oil and gas, to meet demand for energy in future decades.

The slowdown also reflects both the cyclical cuts in exploration made by companies struggling to stay afloat after the drop in oil and gas prices since 2014…

As well as the structural shift in the industry towards onshore shale and similar reserves – especially in North America.

These looming shortages, often called “Peak Oil,” could one day threaten the security of the United States and its allies.

How did this happen?

It all has to do with what we call the Big Oil vs Craft Oil dynamic – which we’ll cover in next week’s issue of Private Capital Insider.

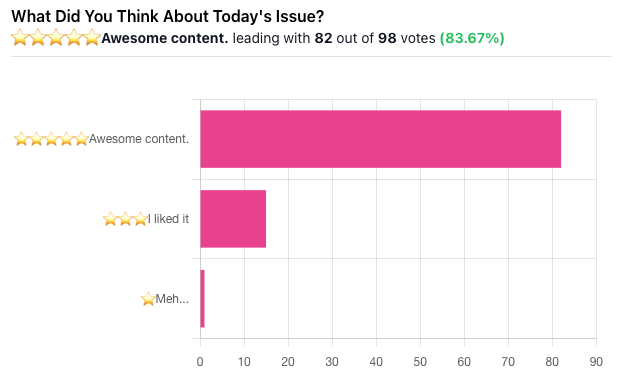

Mailbag: Texas, BlackRock, and American Oil

As always, I want to give a big thank you to everyone who regularly reads Private Capital Insider, rates the issue using the poll feature, and leaves a comment.

Everytime a new issue goes to “print,” I’m hitting that refresh button like crazy during the first 24 hours to see the poll data.

Not only was this the most voted, but it had the highest number of comments on any issue we’ve published so far.

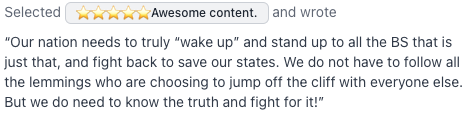

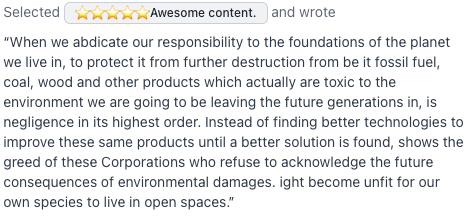

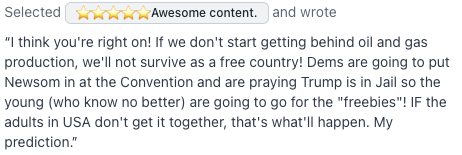

Here are some of my favorites:

Here’s the good news for everyone who is enjoying our coverage on precious metals and now oil: Much of the conversations about the future of currencies rests on top of both the re-monetization of gold/silver, and access to oil and gas.

Here’s the bad news: Investing in asset-heavy commodity businesses is a different beast than investing in asset-light technology companies (often characterized by “high flying” and “fast scaling”).

That’s why we’re going to focus our next several issues on investing in oil and gas.

If you read this far, please be sure to rate the issue and leave me any comments or feedback.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |