- Private Capital Insider

- Posts

- 📈 How to get rich WITHOUT gambling on 100x returns

📈 How to get rich WITHOUT gambling on 100x returns

An Insider’s guide to bigger (and faster) gains with proper risk management

Jake @ Equifund

December 21, 2023

Personally, I know I can’t help myself when I hear about some new way to make big, fast gains in whatever is the hot trend of the moment.

But here’s the truth about the vast majority of fast money strategies – there’s no such thing as “getting rich quick” (outside of pure luck or something unethical/illegal).

And I’m not the only one who thinks so. According to my favorite entrepreneur/investor/philosopher, Naval Ravikant: “There are no get rich quick schemes. That’s just someone else getting rich off you.”

Now to be clear, I am fully aware that there are certain wealth-building strategies that generate significant returns in a short period of time, and are objectively “better” or “faster” or “lower risk” than other equally valid strategies.

However, in my experience, the vast majority of these require active investing strategies, which is when you make money through some sort of work.

While I’m all for building (or buying) private companies and real estate as the core strategy for accumulating wealth in the first place…

If you’re looking to build generational wealth through passive investing strategies, which is when your money makes you more money…

You likely have two realistic options when it comes to investing for passive income.

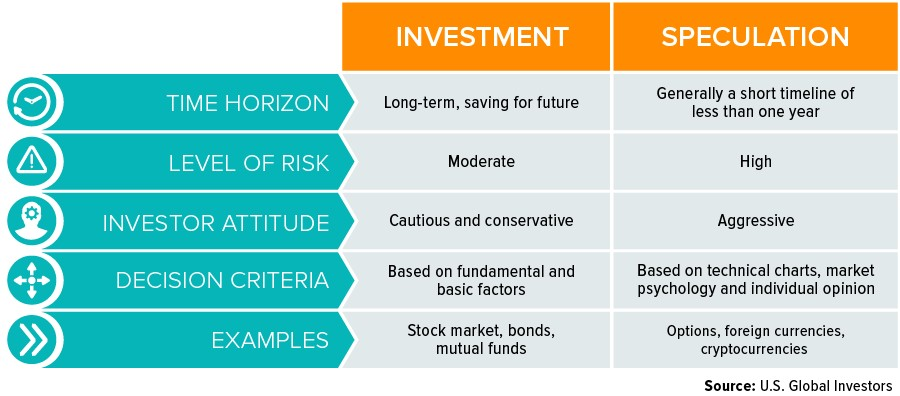

Investing (Get Rich Slow): Accept the 7-12% annual return in public equities, dollar cost average into low-cost index funds, but have relatively low risk and low volatility.

Usually, you need a lot of money already in order to live off these types of returns, or else a few decades left on the clock in which to compound.Speculating (Get Rich Crazy): Move WAY up the risk/volatility curve, and invest in highly speculative investments, with the potential for 10-100x+ returns. While you could get overnight rich, these tend to be “all or nothing” type investments, which usually end up with a 0x.

We can include startups, options, FOREX, and crypto in this category.

In essence, you are required to pick between “investing” and “speculation.”

But if you’re an INSIDER in the financial markets, you have access to a third option that’s somewhere in between investing and speculating.

This “missing middle” on the risk/reward equation seeks to target attractive returns – like 3x - 5x returns in five years or less (or ~25% - 35% annual returns) – with well understood risks that can be reasonably reduced by experienced management teams.

That’s not to say these are “no risk / high return” investment opportunities.

Simply to say that risk is a widely misunderstood concept…

Retail investors – by and large – take on WAY too much risk because they have no concept of risk management…

And they likely do so because they lack any sort of framework for building, managing, and protecting wealth.

That’s why today, we’re going to be zooming out and taking a look at the “big picture” of wealth creation.

-Jake Hoffberg

P.S Looking for back issues of Private Capital Insider?

The Science of Wealth Creation: A brief introduction to building wealth through better risk management

In case you missed it, I recently signed up for a membership to the Corporate Finance Institute, to get some “professional” training in finance.

Although I’ve learned a lot about money, finance, and investing through my 7+ years as a financial copywriter… and I certainly know my way around a spreadsheet…

I knew that I lacked a certain mathematical rigor to build proper financial models, or otherwise do advanced financial planning and forecasting.

That’s why I’m currently working through the Financial Planning & Wealth Management certification program.

And if I had to summarize the biggest breakthrough moment I’ve had in the program so far, it’s this…

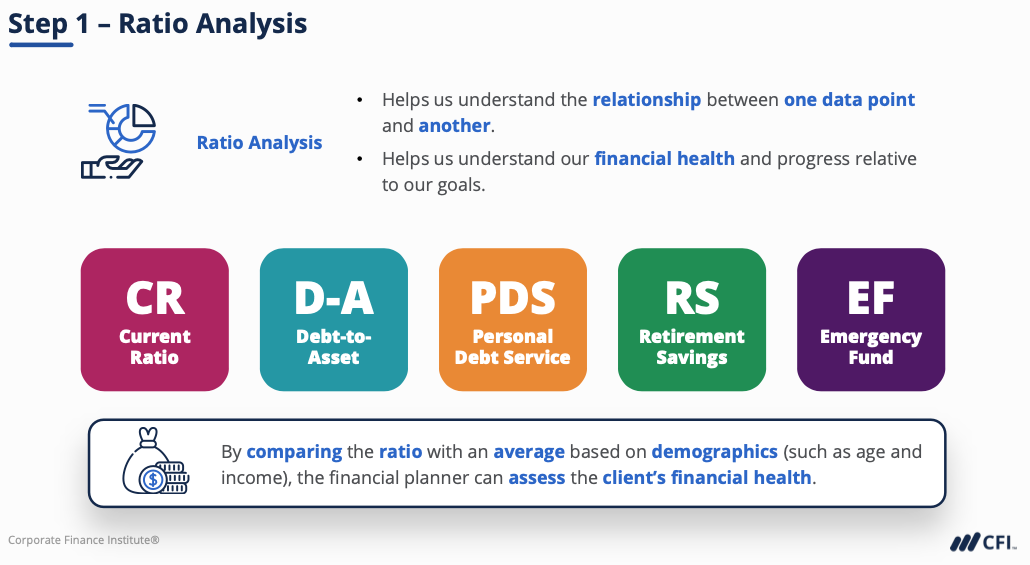

Wealthy people manage their wealth using ratios.

Current Ratio is a measure of liquidity

Debt-to-Asset Ratio shows the percentage of assets that are financed with debt

Personal Debt Service Ratio gives insight into how much cash flow is available after making monthly debt payments

Retirement Savings Ratio tells us if the current savings rate is adequate.

Emergency Fund Ratio tells us how many days we can afford to live, in the event of a financial emergency (like a loss of income)

In other issues of Private Capital Insider, I’ve mentioned that I think most people would benefit from utilizing corporate finance principles to manage their personal finances.

Public finance includes tax systems, government expenditures, budget procedures, stabilization policy and instruments, debt issues, and other government concerns.

Corporate finance involves managing assets, liabilities, revenues, and debts for a business. It also involves raising capital to meet a company's needs and objectives.

Personal finance defines all financial decisions and activities of an individual or household, including budgeting, insurance, mortgage planning, savings, and retirement planning.

In my opinion, the single biggest difference between the two styles is the manager’s relationship with debt and liquidity.

More specifically, in corporate finance, the CEO/CFO is relentlessly focused on raising and deploying capital into projects that exceed their cost of capital, in an effort to deliver positive returns for shareholders.

And I’m not the only one who thinks so. According to NZS Capital:

Investors and corporate management are in the same fundamental business: capital allocation – applying scarce resources toward the best long-term outcomes.

Decentralization is essential to a company’s ability to adapt and evolve. Interestingly, decentralization is NOT a characteristic we find in most companies.

Instead, the most typical structure we find is one of tight central control over day-to-day operations from a hands-on management team (in particular, a hands-on CEO).

Often, centralized/decentralized structure boils down to how the management team understands their role.

To oversimplify, CEOs need to do two things well: manage the business operations efficiently and successfully deploy the cash generated by the business.

Few CEOs understand their primary responsibility is capital allocation, while business operations are given over to business unit managers.

This has the effect of decentralizing operational control while centralizing cash and thereby capital allocation.

This fundamental understanding of a CEO, allocator versus operator, represents a key variable to understanding a great long-term investment.

You’ve heard me say time and time again that the very best business in the world is the money business (i.e., The Family Bank / Family Office concept).

So, if you are serious about building significant wealth in record time, it’s time for you to officially become CEO of Your Money.

Because if you want to learn how to stop working for your money and get your money to work for you…

Then you need to start thinking of your money as one of your employees that you need to give a job to.

“Sounds great Jake! Just one problem. If I already had a financial plan and knew exactly what to do with all my money, I wouldn’t be here trying to figure this thing out.”

Again, if you’re like me, not having “the best possible plan there ever was and ever could be,” became a perpetual source of procrastination.

For a long time, I figured I’d just work hard and the money stuff would sort itself out… or one of my highly speculative hairbrained business ideas would work, and make me rich.

The end result? I worked hard for a long time, earning rather decent money… proactively didn’t put the money into what I thought was a “low yielding” investment… and proceeded to burn all of it inside a startup that I was running.

All of that changed in 2021 thanks to both COVID-19 and me joining the Equifund team.

In the span of about six months, I went from a six-figure income in 2019… to quitting that job to pursue a startup opportunity that failed in early 2020, and picking up $50k in credit card debt for all my troubles.

It took about a year to dig myself out of that hole… but once I did, I decided once and for all I was NEVER going to put myself in a position where I rationalized taking huge risks to chase huge returns without first establishing a proper foundation to support myself.

That is when I got religious about managing debt and liquidity through my Wealth Ratios.

More importantly, I decided I was going to break what was actually a gambling addiction, masquerading as “exciting investment opportunities.”

And once I did that, I started to prioritize capital preservation and risk management, so I could stop constantly going “back to zero,” because I was too emotional with my finances (but too stubborn to hire a financial advisor or ask for help).

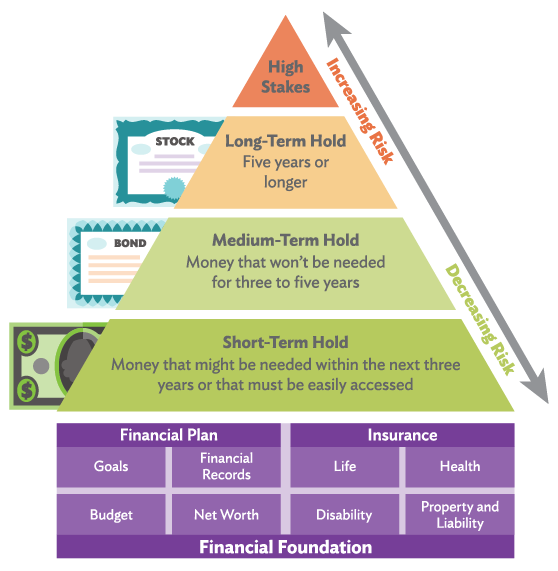

That was when I discovered something called The Investment Pyramid.

SOURCES: Adapted from National Institute for Consumer Education, Eastern Michigan University; AIG VALIC.

The chart is pretty self explanatory, but here is the gist of it…

Step 1) Set meaningful goals.

Remember that money, itself, has no value. It is a medium of exchange and a unit of account. The most important thing I ever did was to stop focusing on MONEY as a goal in itself and instead started focusing on how I can FINANCE the activities I want to do.

Secondarily, I stopped setting goals that other people advertised that I should want (the Keeping Up with the Joneses trap).

And as a result of this, you start to quickly see how the single biggest thing holding you back in life is the lifetime of conditioning you’ve received to borrow money you don’t have to buy things you don’t need to impress people you don’t like.

When you stop playing the game for Status and start playing it for Fun, Freedom, and Family… in my opinion, this is how you wind up achieving the best results, the fastest.

Step 2) Build sufficient emergency savings.

It is my personal and professional experience, most people (and companies) do not put enough value on downside protection and liquidity…

And this is how they put themselves in positions where they have to sell quality assets at a discount to cover short term cashflow issues.

This is why it’s crucial for you to have a cash cushion at all times (Most experts suggest 3-6 months of living expenses) to weather the inevitable storms.

Putting cash into a checking account that got almost no yield was NOT fun. But thankfully I didn’t get my savings into some DeFi yield farming scam, thinking I could get it out any time I want.

I focused all of 2021-2023 getting out of debt and rebuilding my cash position (~$80k-$100k).

Step 3) Get the appropriate insurance coverage!

For a long time, I thought insurance was a complete waste of money. Then, the thing you didn’t get insurance for happen, and you feel like a dummy.

It wasn’t until I started to investigate the whole Overfunded Whole Life Insurance policy thing (often called Infinite Banking) did I begin to understand what an incredible “foundational asset” this can be.

If you’re interested in what I would consider the Holy Grail of investing – Tax Free Passive Income – it doesn’t get much better than this. When set up correctly, money…

Goes in tax free(ish) – Premiums may be tax-deductible if the policy is purchased as part of a business, and the premium payments represent a business expense; most notably, Section 162 Executive Bonus Plan (also called “Key Man” Insurance). However, this will almost certainly be reported as income for the employee, as it would represent compensation.

Be sure to check out our guide on Cash Balance Pension Plans for more on this strategy.

Source: Connor & Gallagher

Grows tax free by a guaranteed rate per year,

Can be borrowed against (also tax free) and then repaid at an interest rate of your choosing. Check out the Buy, Borrow, Die strategy for more on how this works.

Dividend accumulations can also be withdrawn tax free up to the policy basis (i.e., the sum of premiums paid to date). Roth IRA’s also have this pseudo savings account function, where you can also withdraw your principal at any time, penalty free.

The death benefit is paid out tax free (with some exceptions) – Life insurance policy payouts can be pretty hefty and avoiding a major tax bite can be consequential. By contrast, the government will typically tax most retirement plan proceeds when taken by beneficiaries.

When built correctly, Whole Life Insurance winds up not only providing you with a very useful layer of asset protection – the cash value and death benefits of life insurance policies are usually exempt from “attachment” to satisfy debts and creditor claims…

It can also serve as a mechanism to reduce or replace the cash position inside the Emergency Fund, as you can get access to capital via borrowing against the insurance policy.

I promise having just this foundation in place – and knowing your family will be taken care of if anything happens to you – will reduce your anxiety tremendously.

Step 4) Build your balance sheet from low risk to high risk, short term to long term.

I can’t repeat this enough, but as a retail investor, you must prioritize downside protection and liquidity.

The biggest losses in your life will almost certainly happen because you were forced to sell out of a good investment at a discounted rate, and earlier than you would have liked, because you couldn’t cover short-term expenses.

That’s why you need to “ladder” investments that have different time horizons – ideally, we would prefer a regular and “smooth” return of capital, over irregular and “lumpy” events.

Here at Equifund, this is why we DO NOT like venture capital-style deals that require extraordinary risks and 7-10 year hold periods.

If you’re already rich – as in $100m+ under management – you can afford to chase after “Get Rich Crazy” 100x returns, betting on visionary founders looking to “change the world.”

But here’s the thing you figure out once you start building a financial model…

When you plug in the amount of money you have today… then account for all the fees and costs associated with doing anything fancy… you’re probably better off with “Get Rich Slow” index funds, as this would be less work for comparably similar (or better) returns.

But once you’ve got at least $100k of capital to play with, this is when you can start taking advantage of what I like to call…

The Private Capital Accelerator

If I was starting my wealth building journey from $0 (of which I’ve done a few times now), here is what I would do:

Phase 0) Fix your credit score and restructure your debt:

Without knowing anything about you, I would say the single easiest “free lunch” in the Game of Money is to lower your debt servicing costs.

I spent a solid 2 years learning how banks do credit card underwriting, how to “hack” my credit profile based on the information I know they look up (800 credit score now), and how to leverage that score to get lots of cheap money.

Remember – a dollar saved in interest is a dollar earned in gains. If your credit card is charging you 29% APY, mathematically, paying that bill down is the exact same as a 29% return on that money.

But be careful with the 0% credit cards! These things are like fire – used properly it can heat your house and cook your food. If not, it can burn it down with everyone inside.

Phase 1) $0 → $100k Net Worth (Saving):

Just like any business, the goal should be to improve profitability over time. As fast as possible, you need to increase your monthly savings rate, and get to $50k - $100k in liquid capital.

[Note: I am going to start moving this capital into an overfunded whole life policy in 2024, as this will serve as the replacement layer for this.]

Phase 2) $100k → $1m Net Worth (Active Investing):

At this point, I would likely take that capital, go get an SBA loan (up to $5m) and do the whole acquisition entrepreneur thing.

While there is certainly risk to this strategy, I am a big advocate for learning how to buy and sell small businesses. There aren’t many opportunities to realistically generate a seven-figure net worth from nothing in 3-5 years, aside from this.

PLUS! This asset should serve as your core source of active income (wages), the beginning of your passive income (profits), and another asset you can borrow against (leverage).

Phase 3) $1m → $5m Net Worth (Active/Passive Investing):

In my opinion, single digit millionaires are in a bad position – I call it being “Rich (but not rich enough).”

You’ve got enough to live a comfortable lifestyle today, but not enough for the whole family (much less multiple generations).

You’ve got enough to be the target of a lawsuit (or lose it in a crash), but not enough to lose that money and still be okay.

This is when asset protection becomes more important, and you start to transition your income from Active to Passive.

Phase 4) $5m → $25m Net Worth (Passive Investing):

Next (but not last), this is when you fully exit the day-to-day operations of the business and “graduate” to Chairman of the Board and head of the family business…

Or, you make a full exit, take all that capital, make a new plan, and begin again.

Final Thoughts: If you want to win in the Game of Money, look for a good “Banker”

Despite what you hear from the financial media about risk-taking entrepreneurs…

The financial Insiders and Elites, who produce the most consistent returns, HATE taking risks.

And if you want to get into high-quality investment opportunities that have real generational wealth building potential…

You either need to go out into the market, find your own deals, organize your own capital, and otherwise act as the “banker”...

Or, you need to know the “bankers” whom do all that work, and get into their deals.

With this idea in mind, we built Equifund as a mechanism to engineer Alpha for our members.

Note: Equifund Crowd Funding Portal, Inc receives performance based compensation for all Regulation Crowdfunding offerings – 7% of the capital raised + in matching 7% stock awards. This means for every $1m raised in Reg-CF, we would earn $70k in cash and $70k in shares of the offering. While we are the most “expensive” portal in our industry, we believe the incentive structure is key as it is a better alignment with our members interest.

According to Eric Falksteins book “Finding Alpha: The Search for Alpha When Risk and Return Break Down”:

While some alpha seeking is based on understanding portfolio theory, most of it is not.

Alpha is basically private information about straightforward but detailed situations, which implies that people have a good reason to present it strategically.

The theory that risk underlies any returns not due to chance is fundamental to modern finance, and because it is also wrong, presents both current confusion and considerable opportunities to those seeking alpha.

A good risky investment is tied to one's human capital, meaning it is highly idiosyncratic, not so much dependent on covariances with the business cycle as with one's talents.

No matter what your position, it helps to understand how the archetypal alpha is created, because a manager who knows the source of his organization's alpha is much more effective than one who merely knows everyone's name.

Entrepreneurs, inventors, alpha seekers and others like them are trying to create value by doing something differently from how others would do it.

The goal in the search for alpha is to find what you are good at, become better at it, and do it a lot.

Thus, it is more of a self-discovery process in a quest to find an edge that can become a vocation or firm value, rather than a specific trading strategy.

This idea of figuring out what we’re good at, in order to find our source of Alpha, has been a key lesson for us here at Equifund.

We know we can’t play the 100x game in venture capital.

And we know that we’re not going to compete against AI-powered hedge funds in the public markets.

But because our team is uniquely skilled at raising capital from retail investors…

It means we have a far larger universe of investors to work with.

And if all goes well, this also means we can protect our deal position by avoiding a situation where the company can ONLY raise money from a handful of investors who will ask for the “VIP status,” and wreck it for everyone else.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |