- Private Capital Insider

- Posts

- 📈 Are the fees in private markets worth it?

📈 Are the fees in private markets worth it?

An Insider's Guide on Adding Alts to Your Portfolio

Jake @ Equifund

March 13, 2024

If you’re looking for one of the easiest ways to make more money without doing more work, here it is…

Do whatever it takes to reduce (or eliminate) fee drag from your portfolio – whether it’s fees charged by your government, financial advisor, investment manager, broker, or bank.

Why? Because in the Game of Money, every percentage point matters.

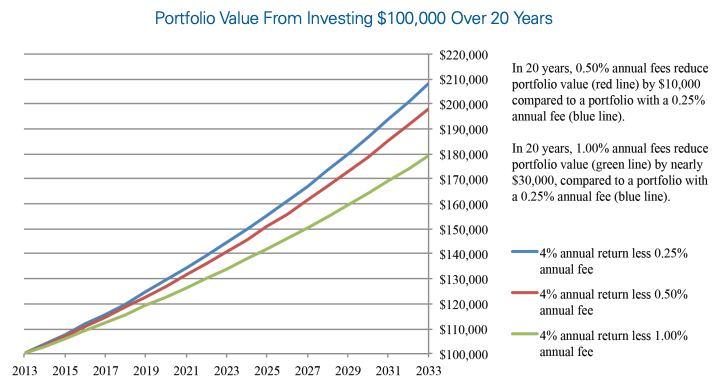

Source: SEC

And the better you become at managing your finances – and directing your investments – the less you have to spend on the endless army of consultants and advisors, who will charge you to do it on your behalf.

To be clear, I’m not saying that you shouldn’t hire advisors to help you achieve your financial goals…

But if you’re going to pay fees for something, you should only be paying for the value they deliver.

So how do you figure out what is worth paying advisors for and what isn’t?

That’s the topic of today's issue of Private Capital Insider.

-Jake Hoffberg

P.S Looking for back issues of Private Capital Insider?

Finding Alpha in a World of Beta

According to economists, in order to generate market-beating returns (called “Alpha”), you must take more risk and more volatility (called “Beta”).

Why? According to the Efficient Markets Theory (EMT), all share prices in the stock market reflect all publicly available information.

This essentially means any ability to “beat the market” over the long term is purely a function of dumb luck and risk tolerance.

Armed with this theory, millions of investors have been sold the benefits of low-cost index funds; if you can’t beat the market, you might as well join it.

Even Warren Buffet says that for most small investors who don't have time to research individual companies, cheap index funds are the best way to invest in the stock market.

But here’s what the Oracle of Omaha wrote in a 1988 letter to Berkshire Hathaway shareholders:

EMT, moreover, continues to be an integral part of the investment curriculum at major business schools.

Apparently, a reluctance to recant, and thereby to demystify the priesthood, is not limited to theologians.

Naturally, the disservice done to students and gullible investment professionals who have swallowed EMT has been an extraordinary service to us.

In any sort of a contest – financial, mental, or physical – it's an enormous advantage to have opponents who have been taught that it's useless to even try.

From a selfish point of view, [we] should probably endow chairs to ensure the perpetual teaching of EMT.

I know you’ve been taught to believe that markets can’t be beaten. But if that were true…

How is it possible that of every single person I know who has more than a $10m net worth, not a single one of them achieved that wealth by dollar cost averaging into low-cost index funds?

Assuming they didn’t inherit it, the vast majority who built such a fortune in a single generation did it by using “Cheat Codes” – wealth-building “hacks” and “super formulas” that I’ll admit are hard to find.

Everyone wants to find Alpha in a world full of Beta - but few do:

Warren Buffet used something called “float” from his insurance companies to generate piles of low-cost capital, giving him a massive advantage over other investors.

Jeff Bezos was able to sell products online without charging sales tax (for a while at least), giving him a massive advantage over his brick-and-mortar competitors who did.

Jimmy “Mr. Beast” Donaldson – a 23-year-old who made $54m in 2021 on YouTube – spent nearly a decade trying to crack the code on the YouTube algorithm, and in the process, discovered his Cheat Code (and has 10 billion views and counting).

So the real question we now have to ask ourselves is this…

In the public markets – which are dominated by institutional investors – is there any Alpha to be found?

Or are we – the average retail investor – part of the Alpha for institutional investors?

Sure, you might get lucky in the short term. But are you willing to put in the time, money, and effort to win long term?

For me, the answer was an easy “no way!” That’s why I rarely do anything other than invest in low-cost index funds.

So where do I turn for Alpha?

It should be pretty obvious that the Private Capital Insider is biased towards private markets.

And the reason for it is simple – it’s the only segment of the market where I feel I can gain any sort of long-term advantage, specifically because of its inefficiencies.

There is a common saying that there are “riches in niches” – and I knew that it was going to be easier to attempt to be a big fish in a small pond than the other way around.

I think Denis Shapiro, author of The Alternative Investment Almanac: Expert Insights on Building Personal Wealth in Non-Traditional Ways, has a great take on this:

I traded options, bitcoins, growth stocks, value stocks, closed-end funds, master limited partnerships (MLPs), utilities, real estate investment trusts (REITs), and dividend-paying stocks.

But every time I thought I was on to something promising, my ego was humbled shortly afterward.

I came to the realization that the stock market was a great tool for asset appreciation, but unfortunately, the benefit of its almost universal liquidity comes with unlimited volatility which, in turn, creates income uncertainty.

Luckily, what also began to emerge during my research for better ways to pick stocks and become a better landlord was a specialty in a certain skill set: networking.

My network started to serve as the foundation for everything I did as an investor.

It was not uncommon for me to talk to an expert in one space (such as mobile home parks), then ask a question about another instrument (like self-storage), and three emails later, I would have a referral to one of the best operators in the self-storage industry.

I soon realized I had stumbled onto exactly what I had been missing in my portfolio.

I knew after all of my failed attempts at creating cash flow from the stock market that I needed to retrain my mindset.

I needed to stop trying to fit a square in a round hole—which is what I was doing every time I tried a new yield strategy using volatile equities.

Instead, I came up with a new investment philosophy that changed how I now look at my portfolio.

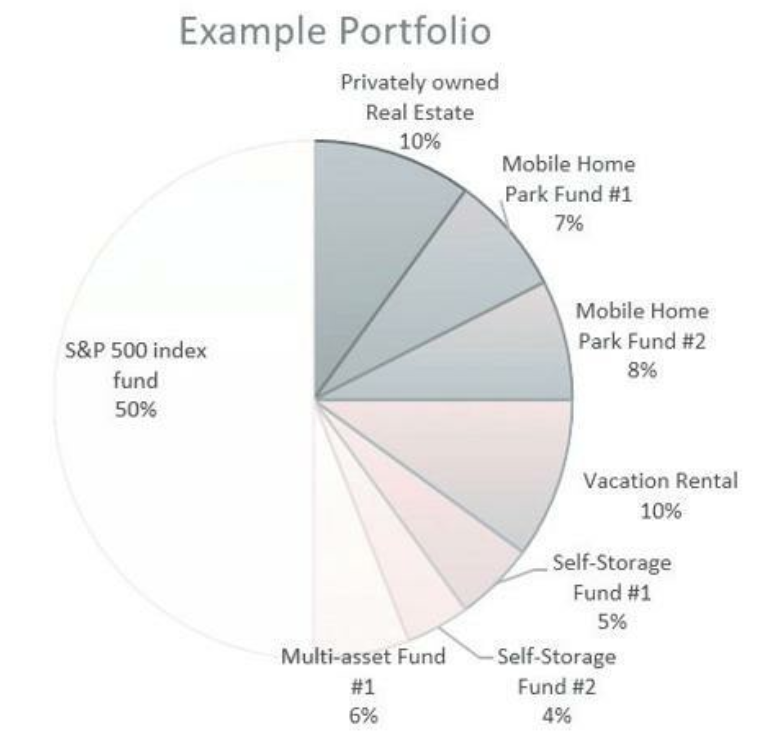

For Shapiro, the solution he came up with was a 50/50 split between public and private assets.

Source: Denis Shapiro

In this model, the PUBLIC side of the portfolio is built for growth, while the PRIVATE side is built for cash flow.

By running this split portfolio, it frees Shaprio to let each side of the portfolio do what it does best, and not fault it for what it doesn’t do.

However, the tradeoff with this portfolio is this: while the left side is very simple and consumes little time, the right requires a LOT of work.

But the time saved by having 50% of his portfolio on autopilot frees up his time to spend on networking and researching private market investments.

According to Shapiro,

To illustrate the effectiveness of my chart, let’s say an investor has a million-dollar portfolio. If they put all of their money into a total stock index fund, their current yield would amount to $15,500 in annual income. [Note: assumes $1m * 1.55% dividend yield]

By going with my model, the annual income increases to $57,750. [Note: assumes $500,000 @ 1.55% yield ($7,750) + $500,000 @ 10% yield ($50,000).]

In the first scenario, they would likely have to sell a portion of their shares every year to supplement their income if they are retired.

In the second scenario, they may never have to sell again depending on their financial needs.

By having so many slices on the right side of the pie, they would also limit significant risk if one deal went south.

Naturally, Shapiro now runs a small fund where he seeks to be a slice of his investors “right side of the pie”...

But does that mean you should give half your money to some private equity manager?

Again, we come back to the issue of fees.

When you invest, you aren’t buying a hypothetical return with no costs. You are buying a financial product that has various fees, which are the killers of returns.

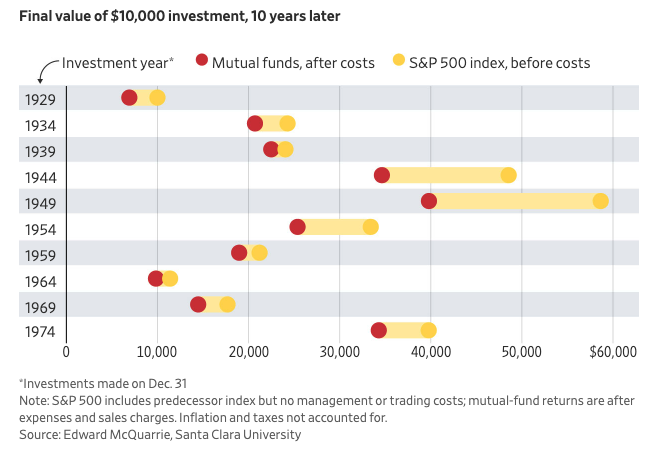

Source: Wall Street Journal

In the real world, where mutual funds charged sales loads of up to 8.5% plus annual expenses, a $10,000 investment in 1926 would have grown to less than $99,000 over three decades.

In the real world, costs ate up half the wealth you could have achieved in theory.

Over the next 30-year period, through 1986, fund investors captured only 71% of the cumulative wealth that the S&P 500 hypothetically generated.

(None of these results account for the toll of taxes and inflation.)

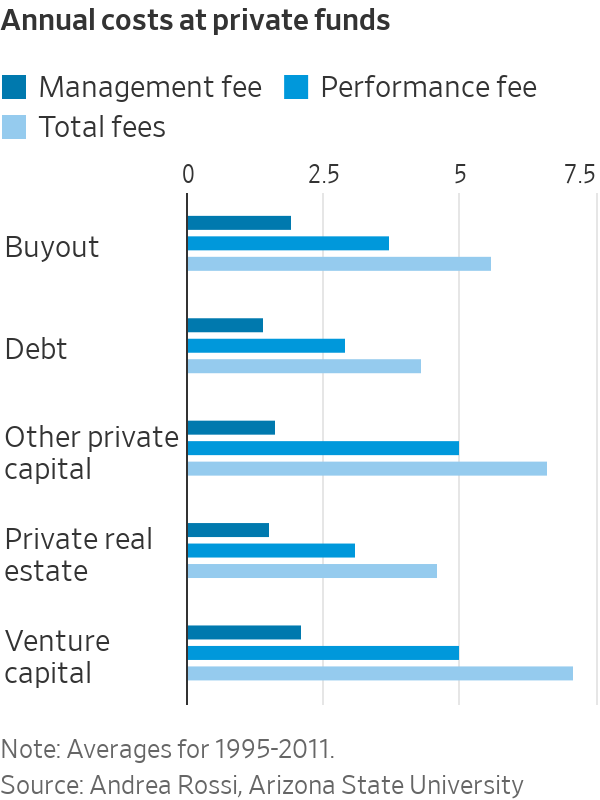

And if you’re interested in the increasing number of alternative-asset-oriented funds hitting the market…

Their past returns might sound great—but only net returns, after subtracting all costs, count.

Source: WSJ

Today, as the fees on index funds and ETFs collapse to zero, Wall Street is looking for new products they can make their margins on.

That’s why it's no surprise to see this major market shift towards offering private assets to retail investors…

And it is for this reason in which we find the opportunity to invest directly into private companies – with no management or performance fees – a compelling value proposition for retail investors searching for passive investment opportunities.

[Note: the only fee Equifund charges its investors is a $24 transaction fee, which is designed to cover the technology and compliance costs we incur per transaction.]

Final Thoughts: Don’t Hire Beta Managers if You're Looking For Alpha

For nearly 10 years, I’ve had one simple thesis about financial advice and wealth management:

As advisors continue to struggle to justify their fees – especially in the assets under management model – they will look to provide value added services (like tax and estate planning), as well as seek to charge additional fees and commissions on private investment opportunities.

But in my opinion, the fee you pay needs to reflect the work that was performed, or the value created.

Unfortunately, the vast majority of investment managers simply cannot outperform their benchmarks – which means there is no reason to pay them to manage investments on your behalf, if you can beat their performance by dollar-cost averaging into a low-cost index fund.

Because if they aren’t generating Alpha (for you, at least), what they are really doing is managing Beta.

However, if you’ve got the right team who understands how to create the proper structures and strategies that provide downside protection, regular cash flow, and upside potential…

And by outsourcing that complexity to an outside advisor, it frees up your time (and emotional energy) to focus on other things…

That is one of the best forms of Alpha you can buy.

Remember: the goal isn’t to “beat the market.” The goal is to live a great life.

Your life shouldn’t revolve around generating financial returns in your portfolio. Your portfolio should revolve around the life you want to live.

Yes, having more money in the bank certainly does help.

But in my experience, it is financial education that shows you the path towards freedom – not a number in your bank account.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |