- Private Capital Insider

- Posts

- 📈 3 Money Myths that Keep You Trapped

📈 3 Money Myths that Keep You Trapped

You won’t believe what #3 is...

Jake @ Equifund

December 08, 2023

There’s a saying I’ve seen floating around the internet that goes something like this – “Money can only solve money problems.”

And even though having more money will almost certainly make many problems easier to solve…

Once you’ve solved all the problems money can solve, now you’re left with the problems money doesn’t solve.

Generally speaking, the vast majority of these problems – whether it’s your health and fitness, your relationship with yourself and other people, or a sense of mission and purpose – inevitably come down to the choices you make and the habits you form.

If you want more money, there are things you can start doing today that can immediately improve your financial situation.

But only if you are willing to “unlearn” many of the Money Myths you’ve been indoctrinated to believe.

Today, we’re going to discuss seven of the biggest lies people believe about money that keep you trapped…

And the so-called “truth” that will put you on a path towards freedom.

Without further ado, let’s get into it.

-Jake Hoffberg

P.S. Looking for back issues of Private Capital Insider?

Three Money Myths that Keep You Trapped

(and the truths that will set you free)

I started my career as a financial ghostwriter in 2016.

At the time, I didn’t know anything about how money, finance, and investing worked…

But I did have one thing that has served me well throughout my life: Curiosity.

I’ve always been interested in ideas. I’ve always been intrigued to learn the secrets behind how things work. And I’ve always valued being “smarter” than other people (or at least “right”).

These are all great qualities when you’re dealing with hard sciences that have “correct” answers.

But when I started to search for the “truth” about money and finance…

Here's the first Money Myth I quickly discovered.

Money Myth #1) Economics is science, and Economists are credible.

Fact: Economics is a social science that is not based on empirical evidence, but opinions that become dogmatic beliefs.

In many areas of our life, there is an “expert” out there who probably knows how that thing works way better than we do…

And we should probably listen to what they have to say before making important life decisions.

Then, there are economists. And even though they have fancy sounding degrees, and may be intelligent people…

Technically speaking, economics falls into the category called “Social Sciences” – which is the relationship between individuals and societies.

Unlike “Real Sciences” – like biology, chemistry, and physics – where the laws of the world are “discovered” by practitioners ...

In Social Sciences – like psychology, sociology, and economics – the social world does not consist of facts, but rather of actions performed in the context of purposes, intentions, and meanings.

And while I’m not suggesting the mathematics and statistical analysis used in economics aren’t “real”...

The stories economists tell about those numbers aren’t the “truth,” but rather, opinions supported by charts, graphs, and numbers.

This is best described by the lie that is Modern Portfolio Theory (MPT) and the Efficient Markets Hypothesis (EMH) – which, after more than seven decades of real world testing, there is no empirical evidence suggesting this Nobel Prize winning theory is correct.

For those who aren’t familiar, EMH and MPT are based on a simple assumption that risk is defined by volatility.

According to the theory, investors are risk averse: they are willing to accept more risk (volatility) for higher payoffs, and will accept lower returns for a less volatile investment.

While this theory sounds simple and elegant, and can be supported by legitimate-looking mathematical proofs and equations…

As H.L. Mencken once said, “For every complex problem there is an answer that is clear, simple, and wrong.”

You don’t need to have a PhD in mathematics to know that humans do not behave rationally… so any economist who tells you they are, is simply delusional.

But if you have the ability to look through this obvious lie and see the truth, you can benefit tremendously.

Here’s what the Warren Buffet wrote in a 1988 letter to Berkshire Hathaway shareholders:

EMT, moreover, continues to be an integral part of the investment curriculum at major business schools. Apparently, a reluctance to recant, and thereby to demystify the priesthood, is not limited to theologians.

Naturally, the disservice done to students and gullible investment professionals who have swallowed EMT has been an extraordinary service to us.

In any sort of a contest – financial, mental, or physical – it's an enormous advantage to have opponents who have been taught that it's useless to even try.

From a selfish point of view, [we] should probably endow chairs to ensure the perpetual teaching of EMT.

I know you’ve been taught to believe that markets can’t be beaten…

But all you need to do is look around, to know that isn’t true.

People beat the market all the time.

And even though you might not be able to outperform the public stock market…

Chances are, there is something you can do that may generate better risk-adjusted returns (called Alpha) than you could achieve in the stock market...

Or at the very least, a strategy that provides you with a return on capital that’s better suited to your financial needs and liquidity preferences.

Money Myth #2) Banks take deposits and loan money, and the money in my bank account is mine.

Fact: By law, banks cannot accept deposits or loan out their reserves. They can only buy and sell securities.

There’s an interesting thing that happens in the educational system that you’re probably not aware of…

Because some concepts are too complex for a student’s education level, the teacher sometimes has to resort to using a dumbed down, “not-actually-true teaching aid” (NATTA) to explain how a concept KIND OF works.

In chemistry, this happens when teaching first year students about the behavior of electrons around the atomic nuclei.

The Bohr-Rutherford model – which is still taught in schools – described electrons that orbit an atomic nucleus like planets around a star…

But we’ve since replaced the Bohr model with the hydrogenic wavefunction, derived from the Schrödinger equation.

While the Bohr Atomic Model (left) is still very useful, the Electron Cloud Model (right) captures reality better.

In this solution, the electron exists as a distributed probability field, it has no “presence,” and indeed, no time dependence (in an energy eigenstate).

Since the Schrödinger solution, we've had several better models - Dirac’s equation, and then QFT, and so on - but the result is the same:

Electrons aren’t solid little balls, and it often makes no sense to talk about them as if they were.

A similar NATTA is used to teach people how the banking system works, and by extension, how money creation works.

The fractional reserve theory of banking is proposed in many textbooks, especially for undergraduate students.

The financial intermediation theory of banking is taught to postgraduate students.

But there is a third theory – the credit creation theory of banking – that was once widely accepted as true, and is no longer even talked about.

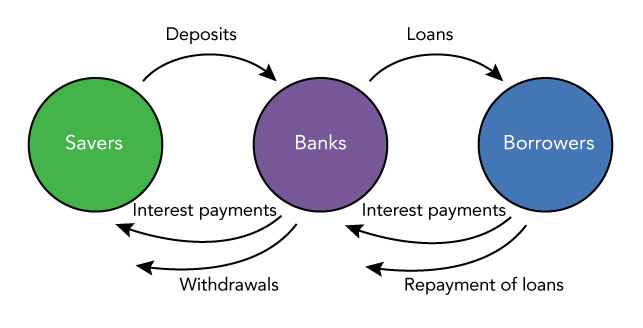

Most people imagine that money is simply a system of government-created tokens (physical or electronic) that get passed from person-to-person as trade is carried out…

And that banks act as financial intermediaries that work kind of like this: Savers deposit money into the Bank, and then Banks then lend that money to Borrowers (called the Money Multiplier Effect).

However, this is completely false. The legal reality is banks don’t take deposits and banks don’t lend money. They buy and sell regulated financial products called “securities.”

In the same way economists come up with incorrect theories of how the economy works…

They also come up with incorrect theories about how banks work, as well.

Source: Richard Werner

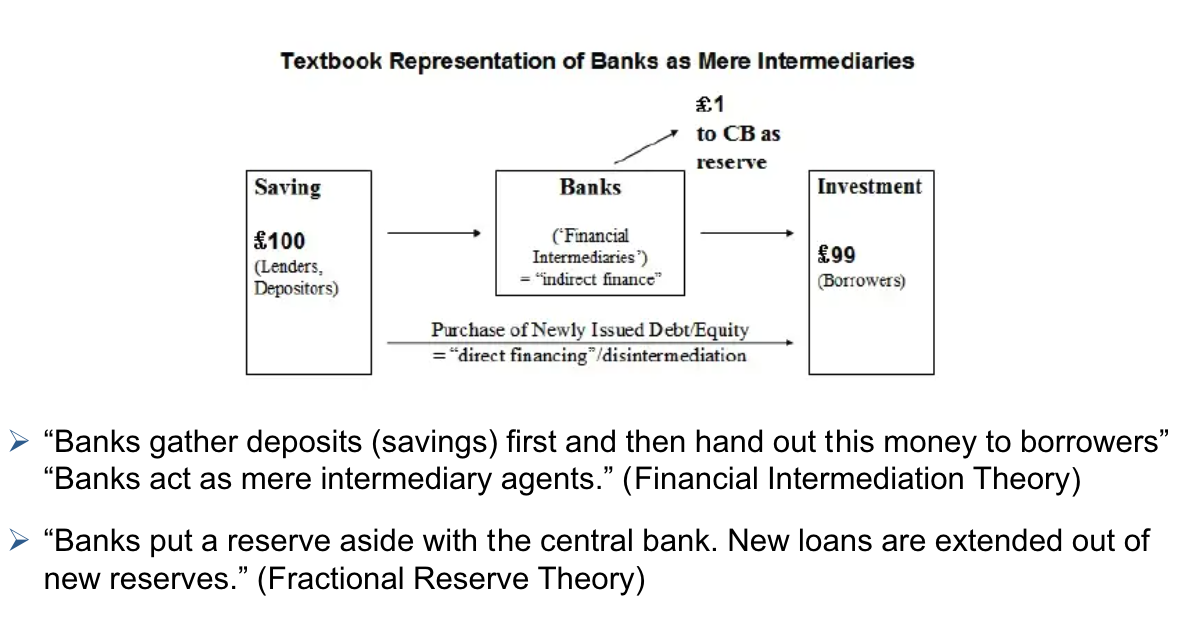

According to Richard Werner, who published the first empirical evidence in the history of banking on the question of whether banks can create money out of nothing…

In modern neoclassical intermediation of loanable funds theories, banks are seen as intermediating real savings.

Lending, in this narrative, starts with banks collecting deposits of previously saved real resources (perishable consumer goods, consumer durables, machines and equipment, etc.) from savers and ends with the lending of those same real resources to borrowers.

But such institutions simply do not exist in the real world. There are no loanable funds of real resources that bankers can collect and then lend out.

Banks do of course collect checks or similar financial instruments, but because such instruments—to have any value—must be drawn on funds from elsewhere in the financial system, they cannot be deposits of new funds from outside the financial system.

New funds are produced only with new bank loans (or when banks purchase additional financial or real assets), through book entries made by keystrokes on the banker’s keyboard at the time of disbursement.

This means that the funds do not exist before the loan and that they are in the form of electronic entries—or, historically, paper ledger entries—rather than real resources.

Here’s how it actually works. The Saver is the Lender, and the Bank is the Borrower.

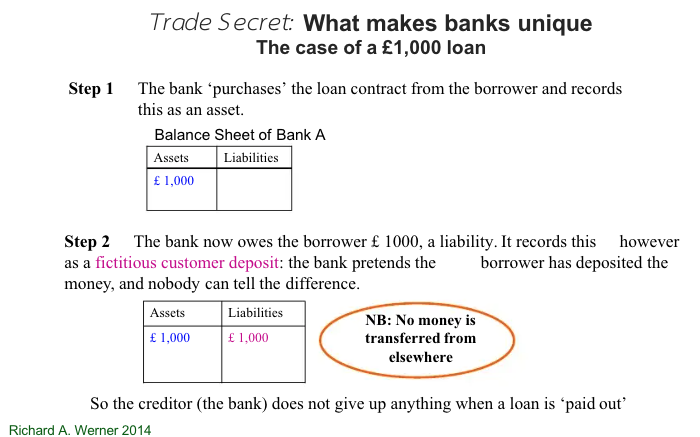

Legally speaking, when you “deposit” money into a bank, what you are actually doing is issuing a loan to the bank (hence the interest).

But it’s actually not a loan.

Instead, the loan contract is actually a promissory note – unlike a loan that must be signed by both parties, a note is a regulated financial product (called a Security) that is only signed by the borrower (the Bank), and secured only by the borrower’s word.

Savers “lend” money to the Banks by selling a promissory note, which then becomes an asset for the Bank, and turns the depositor into a general creditor of the Bank (which is why a “bail in” – where deposits are confiscated – is even legally possible).

Then, the bank creates an account payable, where a CREDIT is recorded on behalf of the customer.

Basically, what you see in your bank account is actually an IOU from the Bank… not a representation of how much of your money is there.

And what you are trading with people are just a bunch of IOUs.

The same is true with money the Bank “loans” to borrowers. It does not give the borrower any “money” it has in reserves. Instead, Banks also record a CREDIT in the borrower's account.

But here’s where it gets really weird… the Bank does not pay out the money referred to in the loan contract turned promissory note.

So where did “your money” actually go? And more to the point, where did “your money” actually come from?

Which brings us to…

Money Myth #3) Money is real and has intrinsic value.

Fact: Money is an accounting fiction developed by humans. It is simply a tool for recording debits and credits.

What is Money? You’ll often hear about two types of money in textbooks:

Narrow Money (M0/M1) – which includes all physical currency held by the central bank…

Broad Money (M2/M3/M4) – basically a “spendable bank IOU” (called commercial bank deposits) and what we spend on a daily basis in our economy .

But the truth about modern Fiat Money is that it is simply credit… nothing more, nothing less.

According to Werner, 97% of all “money” is created by Banks when they extend credit (or “lend”). The money supply (“deposits”) is created via credit creation, which defines effective purchasing power.

The most authoritative writer supporting this theory is Henry D. Macleod (1856), who was a Scottish banking expert and barrister at law.

His influential work – published in many editions well into the 20th century – emphasizes the importance of considering accounting, legal, and financial aspects of banking together.

Based on an analysis of the legal nature of Bank activity he concluded:

Nothing can be more unfortunate or misleading than the expression which is so frequently used that banking is only the “Economy of Capital,” and that the business of a banker is to borrow money from one set of persons and lend it to another set.

Bankers, no doubt, do collect sums from a vast number of persons, but the peculiar essence of their business is, not to lend that money to other persons, but on the basis of this bullion to create a vast superstructure of Credit; to multiply their promises to pay many times: these Credits being payable on demand and performing all the functions of an equal amount of cash.

Thus banking is not an Economy of Capital, but an increase of Capital; the business of banking is not to lend money, but to create Credit: and by means of the Clearing House these Credits are now transferred from one bank to another, just as easily as a Credit is transferred from one account to another in the same bank by means of a cheque.

And all these Credits are in the ordinary language and practice of commerce exactly equal to so much cash or Currency

These banking Credits are, for all practical purposes, the same as Money. They cannot, of course, be exported like money: but for all internal purposes they produce the same effects as an equal amount of money.

They are, in fact, Capital created out of Nothing

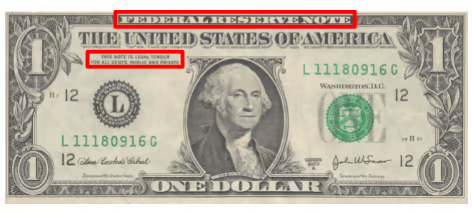

Pull out any denomination of USD, if you don’t believe me.

At the top, it says “Federal Reserve Note” (FRNs) with the notice that “this note is legal tender for all debts; public and private.”

The money supply is created as ‘fairy dust’ produced by the Banks individually, "out of thin air."

U.S. supporters of this theory include Herbert J. Davenport:

…banks do not lend their deposits, but rather, by their own extensions of credit, create the deposits.

As well as Robert Harrison Howe:

The introduction of bank notes was useful in weaning the public from the use of gold and silver coins, and prepared the way for the introduction of Bank Credit as the means of payment for commodities.

This means when you “deposit” money into a Bank, you are selling them a promissory note (which implies they are accepting your private credit)...

And in exchange, the Banks “lend” you FRNs, of which they created out of thin air, by the virtue of their “character,” and then charge you interest for the privilege of using.

The 5 C’s of Credit

The five Cs of credit are character, capacity, capital, collateral, and conditions. They are used by lenders to evaluate a borrower’s creditworthiness and include factors such as the borrower’s reputation, income, assets, collateral, and the economic conditions impacting repayment.

So where does the promissory note – which is recorded as an asset on the Bank’s balance sheet – go?

It goes to the Federal Reserve; as per the bank’s license from the Federal Reserve, agreeing to have such reserves means they can never lend money, but instead exchange one currency into another with their internal capital.

It’s every bank, credit card company and lender’s policy to send your contract via overnight mail to the Federal Reserve once 72 hours has passed (called Truth in Lending, Regulation Z in the Uniform Commercial Code).

This means that the promissory note – which is treated as a cash equivalent – is exchanged for FRNs.

But to make things weirder, according to multiple supreme court cases – as well as The National Bank Act of 1864 and National Banking Act of 1933 – banks cannot lend money from their assets or their depositors' assets, nor can they lend its credit either.

A national bank has no power to lend its credit to any person or corporation…

In the federal courts, it is well established that a national bank has not power to lend its credit to another by becoming surety, indorser, or guarantor for him.

It has been settled beyond controversy that a national bank, under federal law being limited in its powers and capacity, cannot lend its credit by guaranteeing the debts of another. All such contracts entered into by its officers are ultra vires.

Banking Associations from the very nature of their business are prohibited from lending credit.

So what are they actually “lending?”

By many accounts, it appears they are actually “lending” you your own “money” back to you, and charging you interest for the privilege of “borrowing” it.

Final Thoughts: The Importance of Building Credit in a Debt Based Monetary System

When I first started learning the “truths” of the banking system, and how some of the things Banks do are basically legalized fraud and racketeering, I’ll admit I got angry.

But after I calmed down, I felt empowered for one simple reason…

If money isn’t “real,” but simply private credit issued out of thin air by your Bank, logically speaking, this means your “debts” aren’t “real” either.

And more to the point, if you understand how the CREDIT based monetary system works, you can use it the way financial Insiders and Elites do - to their extraordinary advantage.

To that end, if you aren’t regularly checking your credit scores and credit reports… and proactively taking steps to improve your credit score and obtain more credit… and otherwise educating yourself on the actual laws and regulations surrounding banking, lending, credit, and debt collection…

Doing so might represent the most impactful money move you can make in 2024.

What Did You Think About Today's Issue?Select an option below and send us any feedback you have. We're always looking for input from our readers on how we can improve our editorial. |